What Is Owner Financing?

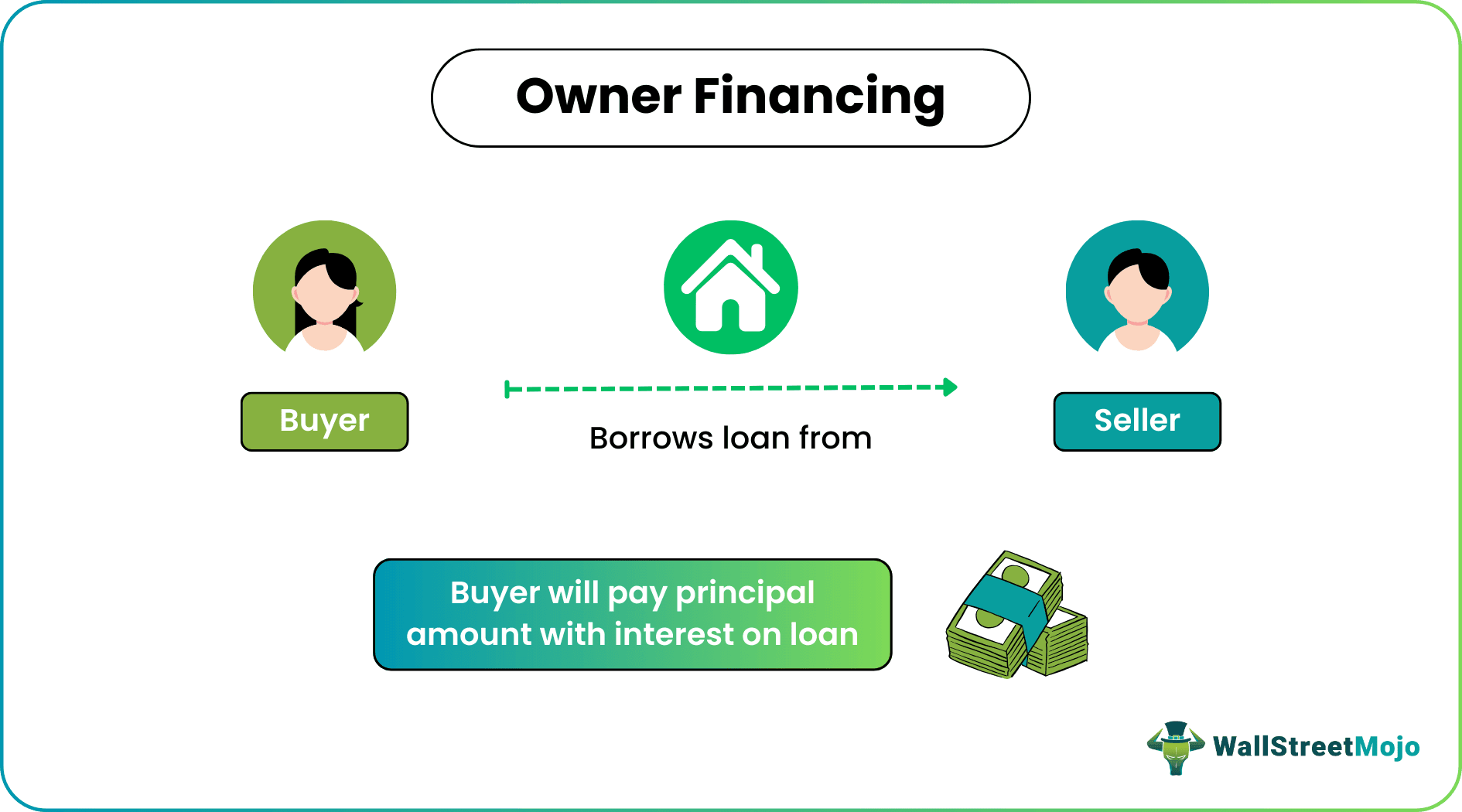

Owner financing is an option where buyers of a property, instead of applying and taking a loan from a banking institution, takes the loan from the owner. The owners fund the transaction under considerationand the buyers repay them the principal amount along with the interest amount over a predetermined period.

It is merely a financing mechanism between a buyer and the seller of a property where the seller of a particular property takes charge of financing the transaction on behalf of the buyer of the property in question. The latter, on the other hand, takes the loan from the seller of the property at a particular interest rate instead of a bank or other financial institution.

Key Takeaways

- Owner financing can be characterized as a situation where the owner finances the proposed transaction, i.e., the buyer borrows money from the owner rather than applying for and receiving a loan from a financial institution.

- A down payment is required from the prospective buyer of the subject property. The transaction is then frequently carried out and documented using a promissory note.

- Owner financing is beneficial as it helps establish advantageous and agreeable conditions for both parties. However, the fact that it may be more expensive than other options available to property buyers may be one of its biggest drawbacks

How Does Owner Financing Work?

Owner financing in real estate, also better known as seller financing, owner carryback, or seller carryback, allows sellers to finance the property on behalf of the buyers, making the buyers pay back the principal amount and the interest money to the supplier over a certain period. However, the buyer must make a down payment, which is usually calculated as a specific percentage of the selling price of that property.

The transaction is often executed and recorded utilizing a promissory note. This note is often referred to as an owner-financing contract that carries all the terms and conditions of the purchase transaction, including amortizations, interest rates, etc. The process is carried out under legal guidance.

So far as the tax implications are concerned, buyers pay property taxes and insurance payments to the concerned authorities separately. In the case of mortgages, these charges are already included in their monthly payments.

Example

The following are the two options available to Mike for purchasing a particular property. Evaluate the two options and determine which one yields less of all totals and turns out to be a better profitable option for Mike.

Solution

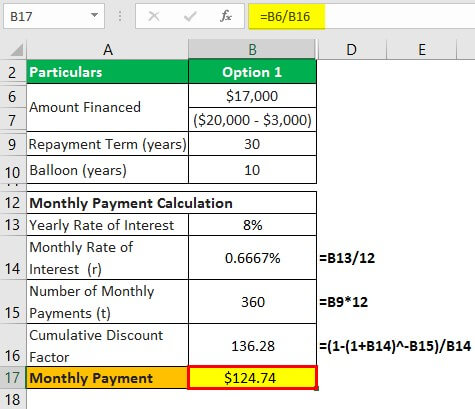

Option 1

The monthly payment, balloon payment due, and total payments due to the seller in the case of option one are calculated as follows:

Monthly Payment Calculation

- The monthly rate of interest (r)= 8/12 = 0.67%

Number of monthly payments = Number of years * number of months in a year

- = 30 * 12

- Number of monthly payments (t) = 360

Cumulative discount factor = (1 – (1 + r)-t ) / r

- = (1 – (1 + 0.0067) -360) / 0.0067

- Cumulative discount factor = 136.28

Monthly payment = Amount financed / Cumulative discount factor

- = $17,000 / 136.2834

- Monthly payment = $124.74

Balloon Payment Calculation

- Number of month in 10 years = 10* 12 = 120

Balloon Balance of a Loan = PV (1+r)n – P [((1+r) n -1)/r]

- = $17,000 (1+0.0067)120 – $124.74 [((1+0.0067) 120 -1)/ 0.0067]

- Balloon Balance of a Loan = $14,913.196

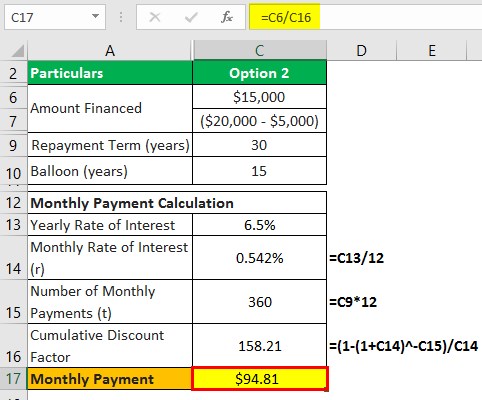

Option #2

The calculation for monthly payment, balloon payment due, and total payments due is as follows:

Monthly Payment Calculation

- Monthly rate of interest (r)= 6.5/12 = 0.542%

Number of monthly payments = Number of years * number of months in a year

- = 30 * 12

- Number of monthly payments (t) = 360

Cumulative discount factor = (1 – (1 + r)-t ) / r

- = (1 – (1 + 0.00542) -360) / 0.00542

- Cumulative discount factor = 158.21

Monthly payment = Amount financed / Cumulative discount factor

- = $15,000 / 158.21

- Monthly payment = $94.81

Balloon Payment Calculation

- Number of month = 15* 12 = 180

Balloon Balance of a Loan = PV (1+r)n – P [((1+r) n -1)/r]

- = $15,000 (1+0.00542)180 – $94.81 [((1+0.00542) n -1)/0.00542]

- Balloon Balance of a Loan = $10,883.87

The above-determined values for both options show that Mike might save more on the loan’s monthly payment if he chooses the second option. But as he is extending the repayment period for another five years in the second option, the interest rises, and he might end up spending higher than the first option. Therefore, Mike should go with the first option.

Pros & Cons

Though owner financing on a home or land or any real estate property gives buyers a huge relief so far as wandering about places in search of loans or finances is concerned, the option comes with a few flaws for both parties. Let us have a look at the benefits and limitations of owner financing.

Advantages

- The first and foremost benefit of the owner financing mechanism could be the elimination of third-party interference, which ultimately allows the participants to save a lot of time, money, and harassment.

- It allows the participants to create terms that they find mutually acceptable and advantageous.

- A seller can choose to collect monthly payments from the buyer and the balloon payment or even sell the owner financing contract to the investors and earn a lump-sum amount on the same.

Disadvantages

- It can be more expensive than other options available to property buyers.

- If a seller of the property happens to take his property back from the owner, he might have to pay for repairs and maintenance costs, too, if the buyer did not take good care of the property in question.

- The buyer might not repay the loan amount as promised while executing the transaction. There is no foolproof way to fully confirm the buyer’s intentions and ability to pay back the loan and interest amount in the future.

- The process of record-keeping is different for each seller. Some record it themselves, while some hire a third party for the same. The buyers must ensure that they are also maintaining the record of each payment made to the seller so that the same can be verified in case of any discrepancy.

Owner Financing Vs Contract For Deed

While owner financing on land or a home is a broader term, a contract for deed is one of its types.

- Though both terms are similar, the contract for deed does not offer buyers the entitlement to the property in question while the installments are going on.

- In the contract for deed or bond for deed mechanism, sellers retain the rights over the property and have the liberty to make improvements and stay there despite buyers paying the installments.

- In owner financing, the clauses and conditions are per the favorability of sellers. On the other hand, a contract for deed becomes the middle path for both buyers and sellers, protecting their interests.

Frequently Asked Questions (FAQs)

What tax effects might owner financing have?

The seller of owner financing pays a significantly smaller tax on the capital gains when the income is received rather than all at once in the first year.

Can you deduct the interest on a home that you personally owner financed?

Whether your first or second property is used as collateral for a loan from a bank or an owner-financed mortgage, the IRS permits you to deduct any interest paid on that loan as a mortgage interest deduction.

Does owner financing report to credit bureaus?

Owner-financed mortgages are frequently not reported to credit agencies; thus, the information won’t appear on your credit report.

Is owner financing legal in Texas?

In a situation where standard lender financing may be challenging to get, owner financing is a legal and efficient approach to selling real estate. The owner-financing procedure is now more challenging than it was in the past, however, due to recent state and federal legislation.

Recommended Articles

This has been a guide to what is Owner Financing. Here we explain how it works along with its disadvantages, advantages, an example & vs contract for deed. You can learn more about from the following articles –