Part of our Fixed Assets and Depreciation guide

Journal Entry For Depreciation

→ Explore all 30 Journal Entries articles

Depreciation Journal Entry is the journal entry passed to record the reduction in the value of the fixed assets due to normal wear and tear, normal usage or technological changes, etc., where the depreciation account will be debited, and the respective fixed asset account will be credited. The main objective of a journal entry for depreciation expense is to abide by the matching principle.

The journal entry for depreciation refers to a debit entry to the depreciation expense account in the income statement and a credit journal entry to the accumulated depreciation account in the balance sheet. In each accounting period, a predetermined portion of the capitalized cost of existing fixed assets, such as equipment, building, vehicle, etc., is transferred from the fixed assets in the balance sheet to depreciation expense in the income statement so that the cost can be matched with the corresponding revenue generated by utilizing these assets.

- The “Accumulated Depreciation” account is captured under the asset heading of Property Plant and Equipment (PP&E ). This account is also referred to as a contra asset account since it is an asset account with a credit balance. Given that the accumulated depreciation account is a part of the balance sheet, its outstanding balance amount is carried over to the next accounting period. The credit balance of the accumulated depreciation account eventually becomes as large as the cost of the assets that are being depreciated.

- The “Depreciation Expense” account is a part of the income statement, and it is a temporary account. At the end of each accounting period, the balance from the depreciation expense account is moved to the accumulated depreciation account. The depreciation expense account will eventually begin the new accounting period with a zero balance.

Examples of Depreciation Expense Journal Entry

Example #1

Let us consider the example of a company called XYZ Ltd that bought a cake baking oven at the beginning of the year on January 1, 2018, and the oven is worth $15,000. The owner of the company estimates that the useful life of this oven is about ten years, and probably it won’t be worth anything after those ten years. Show how the journal entry for the depreciation expense will be recorded at the end of the accounting period on December 31, 2018.

Let us assume that the depreciation will be charged on the straight-line method; then the annual depreciation charge can be calculated as,

Annual depreciation expense = (Cost of the asset – Salvage value of the asset) / Useful life

= $1,500

Therefore, the journal entry for the depreciation expense is as shown below,

Depreciation Journal Entry

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| December 31, 2018 | Depreciation Expense Account | $1,500 | |

| Accumulated Depreciation Account | $1,500 | ||

| To record depreciation expense on the newly purchased cake baking oven) |

Example #2

Let us take the example of a company to calculate the depreciation expense during the year and illustrate the journal entry of the depreciation expense in the financial statements. The following facts are available:

- On January 1, 2018, the company bought a piece of equipment worth $6,000

- The equipment is estimated to have a useful life of 3 years

- The equipment is not expected to have any salvage value at the end of its useful life

- The company intends to follow the straight-line depreciation method over the three years of life

Since the company will use the equipment for the next three years, the cost can be spread across the next three years. The annual depreciation for the equipment as per the straight-line method can be calculated,

Annual depreciation = $6,000 / 3 = $2,000 a year over the next 3 years.

Therefore, it will be recorded according to the golden rule of accounting-

- Debit depreciation expense account and

- Credit accumulated depreciation account

Let us assume that the company prepares annual financial statements only, and the depreciation journal entries can be prepared for the fiscal years (from 2016 to 2018) as of the last day of each year.

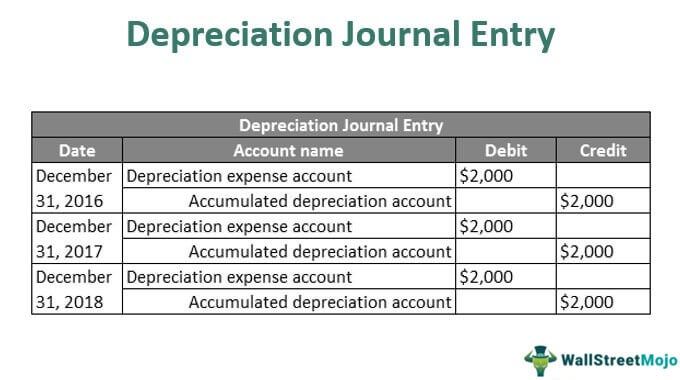

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| December 31, 2016 | Depreciation Expense Account | $2,000 | |

| Accumulated Depreciation Account | $2,000 | ||

| December 31, 2017 | Depreciation Expense Account | $2,000 | |

| Accumulated Depreciation Account | $2,000 | ||

| December 31, 2018 | Depreciation Expense Account | $2,000 | |

| Accumulated Depreciation Account | $2,000 |

Video Explanation of Journal vs Ledger

Relevance and Uses

From the view of accounting, accumulated depreciation is an important aspect as it is relevant for capitalized assets. Therefore, it is very important to understand that when a depreciation expense journal entry is recognized in the financial statements, the net income of the concerned company is decreased by the same amount. However, the company’s cash reserve is not impacted by the recording as depreciation is a non-cash item. Therefore, the cash balance would have been reduced at the time of the acquisition of the asset.

Another important aspect of depreciation is that it is an estimate based on the historical cost of the asset (not the replacement cost), its expected useful life, and its probable salvage value at the time of disposal. There is a common misconception that depreciation is a method of expensing a capitalized asset over a while.

Nevertheless, depreciation is a way of evaluating the capitalized asset over some time due to normal usage, wear and tear of new technology, or unfavorable market conditions. The depreciation expense account and accumulated depreciation account help estimate the current value or the book value of an asset. However, there might be instances when the market value of a one-year-old computer may be less than the outstanding amount recognized in the balance sheet. On the other hand, a rental property located in a growing area may end up having a market value greater than the outstanding amount recognized in the balance sheet. It happens because of the difference in the depreciation method adopted by the market and the company.

Recommended Articles

This article has been a guide to Depreciation Journal Entry. Here we discuss the journal entries on Depreciation expense and the practical example and its uses. You can learn more about from the Accounting following articles –