Part of our Shareholder Equity guide

What Is Contributed Capital?

Contributed Capital is the amount the shareholders have given to the company to buy their stake. It is recorded in the books of accounts as the common stock and additional paid-in capital under the equity section of the company’s balance sheet. It is also known as the paid-in capital and the organizations record this capital from investors only in case the shares are sold to the investors directly (in the primary market).

Contributed Capital Formula

It is reported under the equity section of the company’s balance sheet and generally split into two different accounts which are as follows:

Contributed Capital Formula = Common Stock + Additional Paid-in Capital

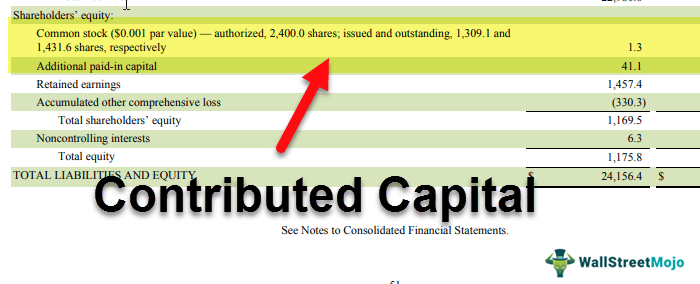

- Common Stock – The common stock is the par value of issued shares. The common stock of the company appears on its balance sheet below as common stock and preferred stock.

- Additional Paid-in Capital – The additional paid-in capital of the company represents money paid, which is paid by the shareholders of the company above the par value to the company.

Examples

Company X ltd issued 1,000 common stocks to the investors at the par value of $ 10 each. However, as per the requirement and terms and conditions of the issue of shares, the investors have to pay $ 100,000 for these shares. The shares were fully subscribed, and the investors paid $ 100,000 for these shares having the par value of $ 10,000 (1,000 shares * $ 10). Now, for this issue, $ 10,000 (being par value) will be recorded by the company in common stock accounts, and the additional $ 90,000 ($ 100,000 – $ 10,000) will be recorded to paid-in capital as this amount is in excess of the par value of shares. Total contributed capital will be the sum of both of these accounts, i.e., a sum of common stock accounts and the paid-in capital accounts, which will be equal to $ 100,000 ($ 90,000 + $ 10,000).

Advantages

#1 – No Fixed Payment Burden

The amount received in the form of contributed capital does not increase the fixed cost or the fixed payment burden of the company. It is so as it has no fixed compulsory payment requirements, which are there in case the capital is borrowed by the company in the form of regular interest payments. For this, the company pays dividends to the shareholders in case of profits. However, in the case of profits as well, it is not compulsory to pay a dividend as it deferred and diverted to other business opportunities or requirements if needed for the betterment of the company.

#2 – No Collateral

For the equity shares issued, the investors do not ask for a pledge of collateral, which can be there if the company raises funds by borrowing the money. Also, the existing assets of the business remain free, which are then available in case required as security for loans in the future. Apart from existing assets in case, the company purchases new assets with the funds raised through the issue of equity capital, then it can also be used by the company for securing its long-term debt in the future.

#3 – No Restrictions on Use of Funds

The main motive of the lender of funds if the company borrows the fund is on the repayment of debt and interest portion on time. So, a lender wants to make sure that the proceeds of the loan are used in areas where they can generate the cash for the repayment of the loans on time. Thus the lender establishes the financial covenants, which put restrictions on how one can use proceeds of loans. However, this restriction is not there in case of equity investors who rely on governance rights so that their interest remains protected.

Disadvantages

#1 – No Guarantee of Return

From the perspective of the investors, contributed capital does not guarantee any profits, growth, or dividends to them, and their returns are more uncertain when compared with the returns received by the debt holders. Due to this risk, equity investors expect a higher rate of return out of their investment.

#2 – Dilution of Ownership

Equity investors have governance rights with respect to the election of a board of directors and the approval of many major business decisions of the company. This right leads to the dilution of ownership and control and increases in the oversight of the management decisions.

Important Points

The organizations record only those paid in the capital, which is sold directly to the investors of the company, i.e., the contributed capital is recorded only in case of initial public offeringsor the other stock issuances which are there directly to the public. So, any capital which is traded (bought and sold) in the market directly among the investors is not recorded by the company in paid-in capital as in that case the company is neither receiving anything nor giving anything and the paid-in capital will remain unchanged.

Retained earnings are the company’s net profits which remain undistributed to the shareholders of the company as dividend and do not form as the part of the contributed capital of the company as it is restricted to the amounts which the investors pay for buying equity stock of the company. In the case of retained earnings, there is no capital contribution by the investors and hence do not form as the part of the contributed capital of the company.

Conclusion

Contributed capital is the accounting entry on the balance sheet of the company in the form of common stock and additional paid-in capital showing the amount raised by the company by issuing the stock that has been bought by the shareholders of the company. It is the equity investment made by shareholders in a company. Stock can be bought by the shareholders by paying the cash or in exchange for the fixed assets in the company. Also, it is possible to acquire the stock of the company in exchange for the reduction in the company’s debt. Each of the mentioned aspects will result in an increase in the equity of stockholder. Only those capital are recorded, which are sold directly to the company’s investors.

Recommended Articles

This has been a guide to what is Contributed capital and its definition. Here we discuss components of contributed capital in accounting, examples, advantages, and disadvantages. You can learn more about accounting from following articles –