Part of our Capital Budgeting guide

Examples of Capital Budgeting Techniques

With the help of capital budgeting, we can understand that some methods make decisions easy; however, some methods do not arrive at a decision; it makes it difficult for an organization to make decisions. The below example of the capital budgeting technique shows us how an organization can decide by comparing future cash inflows and outflows of the individual projects. The point to be remembered on capital budgeting is that it considers only financial factors in investment, as explained in the below examples, and not a qualitative factor.

Capital Budgeting Formula Excel Template

Download Excel Template- Capital budgeting is making long-term investment decisions, such as replacing existing machinery with a new one. It involves analyzing a project’s future cash inflows and outflows and determining whether it is financially viable.

- While capital budgeting considers only financial factors and not qualitative factors in investment decisions, it is a critical process for companies that require substantial funds for capital expenditures.

- Capital budgeting techniques include the payback period, accounting rate of return, net present value, and discounted payback period, which provides a quantitative analysis for choosing the most profitable investment.

Top 5 Examples of Capital Budgeting

Let’s see some simple to advanced examples of capital budgeting to understand it better.

Example #1 (Pay Back Period)

Pay Back Period Definition and how to understand that. Let’s discuss this by considering the below example?

An XYZ limited company looking to invest in one of the new projects and the cost of that project is $10,000 before the company wants to analyze how long it will take a company to recover invested money in a project?

Solution:

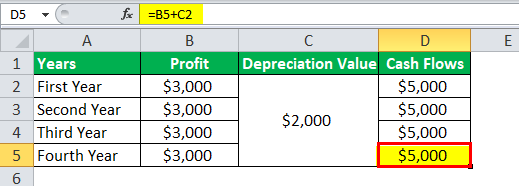

Let’s say in a year one, and so on, the company recovers a profit as listed in the table below.

So how long will it take the company to recover invested money from the above table it shows three years and some months. But this is not the right way to find out a payback period of initial investment because the company’s base is profit. It is not a cash flow, so profit is not the right criteria, so a company should use it here as cash flow. So profit is arrived after deducting depreciation value, so to know the cash flows, we have to add depreciation in profit. The depreciation value is $2,000, so net cash flows will be as listed in the below table.

So from Cash flow analysis, the company will recover the initial investment within two years. So the payback period is nothing but the time taken by cash inflows to recover the investment amount.

Example #2

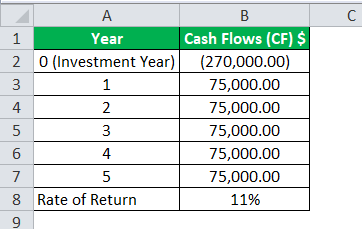

Calculate the Payback Period and Discounted Pay Back Period for the project, which costs $270,000 and projects expected to generate $75,000 per year for the next five years? The company required rate of return is 11 percent. Should the company go ahead and invest in a project? The rate of return is 11%. Do we have to find it here, PB?DPB?Should the project be purchased?

Solution:

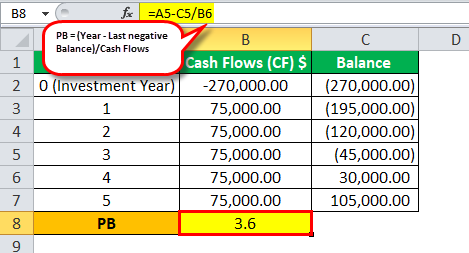

After adding each year’s cash flows, the balance will come, as shown in the below table.

From the above table, positive balance is in between 3 and 4 years, so,

- PB= (Year – Last negative Balance)/Cash Flows

- PB=[3-(-45,000)]/75,000

- PB= 3.6 Years

Or

- PB= Initial Investment/Annual Cash Flows

- PB= 270,000/75,000

- PB= 3.6 Years.

The Discounted rate of return of 11% Present Value of Cash Flows are shown below.

- DPB= (Year – Last negative Balance)/Cash Flows

- DPB= [(4-(37,316.57)/44,508.85)

- DPB= 4.84 Years

So from both capital budgeting methods, it is clear that the company should go ahead and invest in the project as though both methods will cover the initial investment before five years.

Example #3 (Accounting Rate of Return)

The accounting rate of Return technique of capital budgeting measures the annual average rate of return over the assets life. Let’s see through this example below.

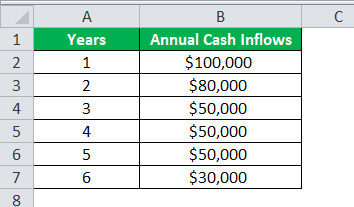

XYZ limited company planning to buy some new production equipment, which costs $240,000, but the company has unequal net cash inflows during its life, as shown in the table, and $30,000 residual value at the end of its life. Calculate the accounting rate of return?

Solution:

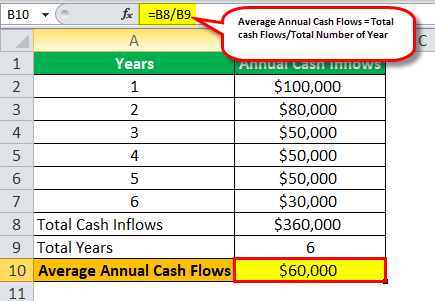

First, calculate the Average Annual Cash Flows

- =Total cash Flows/Total Number of Year

- =360,000/6

Average Annual Cash Flows =$60,000

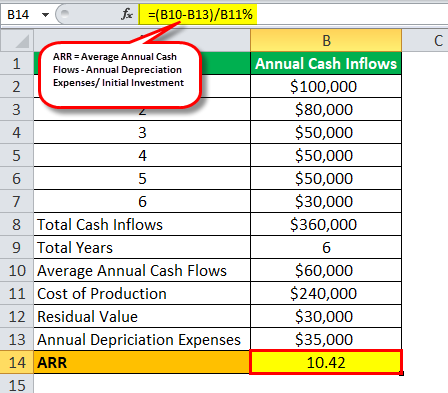

Calculate Annual Depreciation Expenses

=$240,000-$30,000/6

=210,000/6

Annual Depreciation Expenses =$35,000

Calculate ARR

- ARR=Average Annual net cash flows – Annual Depreciation Expenses/ Initial Investment

- ARR=$60,000- $35,000/$240,000

- ARR=$25,000/$240,000 × 100

- ARR=10.42%

Conclusion – If ARR is higher than the hurdle rate established by company management, it will be considered, and vice versa, it will be rejected.

Example #4 (Net Present Value)

Met Life Hospital is planning to buy an attachment for its X-ray machine, The cost of the attachment is $3,170, and life of 4 years, Salvage value is zero, and an increase in cash inflows every year is $1,000. No investment is to be made unless having an annual of 10%. Will MetLife Hospital invest in the attachment?

Solution:

Total investment Recovered (NPV)= 3170

The above table shows that cash inflows of $1,000 for four years are sufficient to recover the initial investment of $3,170 and provide exactly a 10% return on investment. So MetLife Hospital can invest in X-ray attachment.

Example #5

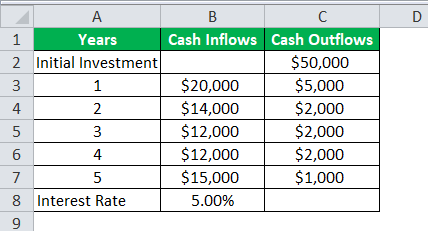

ABC limited company is looking to invest in one of the project costs of $50,000 and cash inflows and outflows of a project for five years, as shown in the below table. Calculate Net Present Value and Internal Rate of Return of the Project. The interest rate is 5%.

Solution:

First, calculate net cash flows during that period by Cash inflows – Cash outflows, as shown in the table below.

NPV= -50,000+15,000/(1+0.05)+12,000/(1+0.05)²+10,000/(1+0.05)³+ 10,000/(1+0.05)⁴+

14,000/1+0.05)5

NPV= -50,000+14,285.71+10,884.35+8,638.56+8,227.07+10,969.21

NPV= $3,004.84 (Fractional Rounding of)

Calculate IRR

Internal Rate of Return = 7.21%

If you take IRR 7.21% the net present value will be zero.

Points to Remember

- If IRR is > than Discount (interest) rate, than NPV is > 0

- If IRR is < than Discount (interest) rate, than NPV is < 0

- If IRR is = to Discount (interest) rate, than NPV is = 0

Frequently Asked Questions (FAQs)

1. What are some examples of capital budgeting projects for a manufacturing company?

A manufacturing company may invest in a new production line, purchase new machinery, or construct a new factory building. These capital budgeting projects require significant capital expenditure, and the company needs to evaluate the potential returns on investment before making a final decision.

2. What is an example of a capital budgeting project for a service-based company?

A service-based company may invest in a new software system or upgrade its IT infrastructure. These projects are important for improving the efficiency and effectiveness of the company’s operations and can generate significant cost savings or revenue growth.

3. What is an example of a capital budgeting project for a real estate company?

A real estate company may invest in a new development project, such as constructing a new office building or shopping center. These projects require significant capital expenditure and can generate long-term returns through rental income and property appreciation.

Recommended Articles

This has been a guide to Capital Budgeting Examples. Here we provide the top 5 examples of Capital budgeting techniques and explanations. You may learn more about accounting from the following articles –