What Is Float Management?

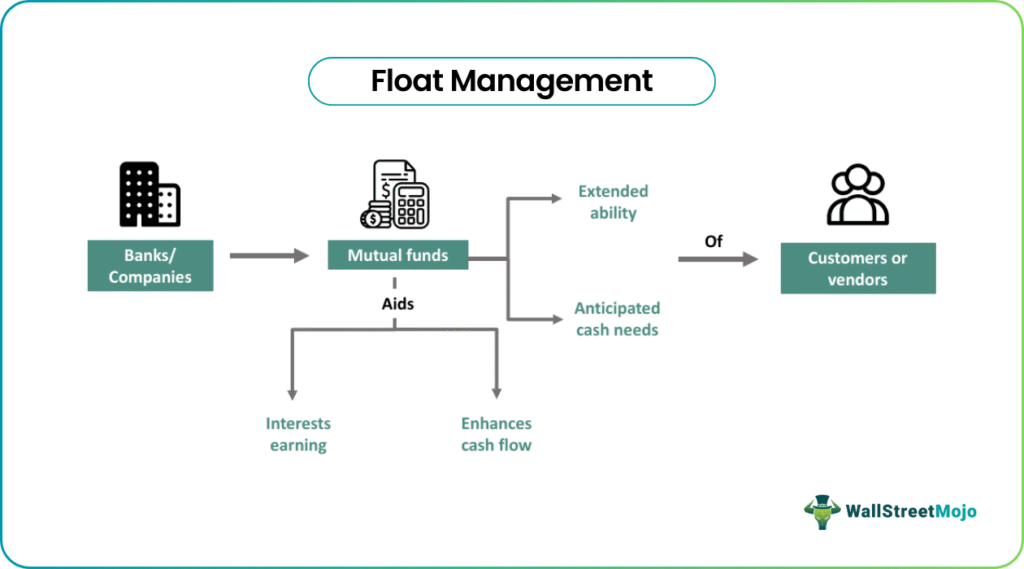

Float Management in finance refers to keeping a watch on the timing of cash flows and implement strategies to maximize the advantages of the time gap between the funds getting deposited and cleared (float). It serves to earn more interest by extending fund availability, increasing liquidity, and managing working capital by optimizing cash flow.

Banks’ time floats in a manner that they can utilize to extend the cash-on-hand utility for the long term. It can lead to a negative float arising out of a discrepancy between customer and bank float. It maximizes liquidity by holding securities for immediate buying and selling in markets.

- Float management in finance involves strategically aligning cash flow timing to capitalize on the time difference between fund deposition and clearance (float).

- It aims to expand fund availability, boost interest earnings, enhance liquidity, and optimize working capital through efficient cash flow management.

- It can be achieved by utilizing cash flow forecasting, technology implementation, real-time management, outsourcing, maximizing collection and minimizing disbursement float, optimizing cash positioning, and leveraging technology.

- Its improvement in cash flows and reduction of overdrafts contrasts with potential ethical dilemmas that could harm customer and vendor relationships.

Float Management Explained

Float management involves manipulating fund availability for a more extended period before the funds are actually needed. As a result, it gives banks and businesses more time to use these funds for investments, business operations, debt reduction, or earning interest. It generally involves the disbursement of floats and the early payment discount technique. By using the disbursement float method, a company can delay payments to retain cash in its account for more extended periods.

On the other hand, by using the early payment discount technique, companies give discounts to customers for faster payments and motivate them to deposit their checks very quickly. Efficient management of floats improves cash flow, reduces overdrafts, and improves holistic financial performance. On the contrary, a lousy float management system results in problematic cash flow, leading to financial instability. In the project, it identifies slack or float time within a project’s schedules, streamlines projects, and works around delays.

An effective float management system efficiently optimizes cash flow and ensures enough liquidity to meet the financial needs of a company. Businesses can accelerate the availability of funds and improve their working capital position. Overall, float management is an essential aspect of financial management that can help companies maintain liquidity and financial stability.

Techniques

Companies may enhance their cash flow and their procedures and provide better financial outcomes by using the techniques below:

- Cash Flow Forecasting: It enables robust cash flow estimation, which is vital for risk mitigation and float optimization.

- Technology Implementation: Using Automated Clearing House (ACH) payments, online banking, float management software, Electronic Bill Payment and Presentment (EBPP), and mobile payments to optimize float.

- Real-Time Float Management: Undertake educated cash flow decision-making, which is becoming more popular.

- Outsourcing Float Management: Deploy proficient businesses to provide cash flow tactics that are maximized.

- Maximizing Collection Float: Use lockbox systems for quicker check receptions, early payment incentives, and remote deposit capture for optimized float.

- Minimizing Disbursement Float: Utilize restricted disbursement accounts and extended periods to manage payments while adhering to vendor agreements strategically.

- Optimizing Cash Positioning: For the best possible cash management, centralize funds through concentration banking and invest excess money in zero-balance accounts.

- Leveraging Technology: Adopt electronic payments to speed up transactions and use cash management software for tracking and forecasting.

- Disbursement Float Management: Increase cash flow by encouraging quicker client payments and purposefully postponing payouts to prolong cash retention times.

Examples

Let us use a few examples to understand the topic.

Example #1

Suppose Cogsworth Bank which has distinguished itself in Verbidian’s busy financial scene as a master of float management. Luminax City’s Mayor Penelopex depends on their knowledge to negotiate the tricky tax scenario successfully. Cogsworth Bank maximizes the amount of time between payments and transfers to the Royal Reserve Bank by carefully timing their deposits of Lumos, the local currency.

This financial aspect is arranged by the expert banker, Mr. Widget, who makes sure that Luminax City’s money is handled correctly. But the setting up of a new rival- Cloverleaf Bank, gives an unpredictable quality to the environment. The Regulatory Guild’s continuous observation guarantees the fairness of the competition. Cogsworth Bank’s financial skill continues to garner confidence as Lumina City thrives despite the hurdles faced by rivals.

Example #2

A March 25, 2016, report states that traditional banks are grappling with a complex challenge of the monetary float. This temporary holding space for funds, needed to bridge the gap between transactions, demands expensive high-liquidity securities and adds to operational burdens. Fintech companies, with their lower costs and potential regulatory advantages, are seen as a threat to this established system. Additionally, the opening up of banking services has paved the way for non-bank players like PayPal and Alipay, who manage their float using pre-paid customer funds.

However, PayPal’s partial shift to banking demonstrates the challenges of navigating float outside the traditional system. Plus, the proposals for alternative solutions like blockchains and virtual currencies are prompting calls to eliminate the float requirement. As a result, central banks have been taking note of it. Therefore, these trends could lead to significant changes in the related policies, even a potential return to full-reserve banking.

Example 3

MPESA float management is a crucial component of the MPESA, a mobile money service agent, float system. It is because it helps MPESA agents optimize their existing cash. Hence, these agents effectively serve customers and maintain liquidity by buying a float of approximately Sh400,000 ($2,605.01) from any branch of Stanbic Bank. Therefore, they contribute to the overall success of the mobile money platform by enhancing cash flows.

One way to achieve optimal cash flow for MPESA agents is through an effective float management system. Although it optimizes the cash flow of a business, it must be used cautiously and ethically so that the relationship with customers and vendors is not harmed. It impacts the liquidity and cash flow of a company significantly. An accurate prediction of cash outflows and inflows aids businesses in handling their float successfully. As a result, it improves the overall financial performance of businesses and banks alike.

Advantages And Disadvantages

Firms and banks must know the below pros and cons before utilizing it to their advantage:

| Advantages | Disadvantages |

|---|---|

| Improves cash flows and reduces overdrafts. | It may become unethical, hampering customer and vendor relationships. |

| Daily managing it helps minimize the borrowing cost, adding to the company’s bottom line. | Exposes companies to public scrutiny, increasing their vulnerability to takeover bids. |

| Strategically optimizes cash flows. | Firms and banks face increased accountability from shareholders, drawing massive criticism during financial turmoil. |

| It aids in increasing the overall financial stability of a business. | Firms may try to exploit float to raise credit and liquidity, leading to increased risks for stakeholders and investors. |

| Identifies float times, optimizes resource use, and optimizes tasks in project management. | It increases substantial costs for public companies due to higher professional fees |

Frequently Asked Questions (FAQs)

1.What is float management related to?

It has to do with managing a company’s financial situation strategically by maximizing the interval between cash inflows (receipts) and outflows (payments). In order to maximize liquidity entails efficiently controlling the interval between the moments that funds are disbursed and when they are available for usage.

2.What are the three types of float in float management?

The three categories of floats are collection, dispersal, and net floats. The collection float represents the total number of checks deposited into an account between available funds and deposit time. Disbursement float measures the time between clearing a cheque and disbursing funds. Net float separates the collecting and disbursement floats.

3.How can technology help in float management?

Technology allows for electronic fund transfers, automates payment procedures, expedites reconciliation work, provides real-time cash position visibility, and supports data analytics for improved decision-making.

Recommended Articles

This article has been a guide to what is Float Management. Here, we explain the concept along with its techniques, examples, advantages, and disadvantages. You may also find some useful articles here –