What Is Conventional Cash Flow?

Conventional Cash Flows (CCFs) are defined as a series of inflows and outflows, with an initial outlay at the beginning followed by only cash inflows afterward. In the process, the cash flow pattern changes its direction only once and keeps proceeding in that direction.

CCFs are significant in evaluating the net present value (NPV) of future cash flows. Further, the internal rate of return (IRR) from a particular project’s CCFs should be more than the company’s hurdle rate. It helps the company choose the best and most profitable investment among the given alternatives.

Key Takeaways

- A conventional cash flow refers to a series of inflows and outflows with a single change in the direction of the flow.

- The series starts with an initial outlay a cash outflow, and then progresses with only cash inflows from operations, financing, investing, etc. Therefore, the pattern is represented as -, +, +, +, +, and so on.

- CCFs facilitate decision-making by evaluating the net present value of future cash flows from an investment and estimating its profitability based on the internal rate of return.

Conventional Cash Flow Explained

Conventional cash flows (CCFs) mirror the traditional investment pattern where businesses make an initial investment and subsequently generate income. This CCF concept is driven by the desire for a single initial cash outflow followed by consistent inflows.

The cash flow pattern can be defined as follows:

- Outflow: This represents the initial investment that businesses make when embarking on a new project, expanding their operations, or acquiring assets. It typically encompasses substantial expenses, including capital expenditures and working capital requirements. Outflows are denoted by a negative (-) sign, indicating cash leaving the company.

- Inflow: Inflows consist of the revenue generated from a business’s operations. This represents the income they continue to earn as long as the investment remains operational. Inflows are denoted by a positive (+) sign, signifying cash entering the company. The conventional cash flow pattern is thus represented as -, +, +, +, and so on. However, if a company experiences an outflow at some point, its cash flows are no longer considered conventional.

For a practical example, consider Nina, who invested $100,000 in a private firm in 2017, acquiring a 10% equity stake. She receives dividends each month as income from her investments. The initial $100,000 investment represents her cash outflow, and the dividends she receives constitute her cash inflow. Since there are no other significant outflows, her cash flows are conventional.

In practice, most investments deviate from the CCF model as they involve ongoing expenses such as raw materials, maintenance, and additional capital outlays. CCFs play a pivotal role in decision-making for companies facing choices between diverse projects. Moreover, the IRR for CCFs should surpass the hurdle rate, representing the minimum acceptable return, making them indispensable for businesses seeking the most profitable investments.

Examples

Study the examples given below to understand the concept better.

Example #1

Tyler sold his ancestral house for $500,000. He invested this amount in a safe asset that gave him decent returns for his children’s tuition in 10 years. Tyler’s friend advised him to invest in no-load mutual funds, which wouldn’t take up a considerable chunk of his investment amount as fees.

Ten years later, Tyler took a part of the money for his first child’s tuition and left the remaining amount in the fund. Five years later, he withdrew another portion of the fund when his second child went to college. The remaining amount was still invested in the mutual fund for his retirement. It follows a CCF pattern, as Tyler only invests once and does not lose any money in commission or charges.

Example #2

Here is an example of an annuity and CCFs. An annuity is a standard investment option in the United States, with investors mostly looking to ensure an income source after retirement. Since it is an investment, they estimate the present value of future cash flows from annuities offered by different companies to choose the best option that works for them.

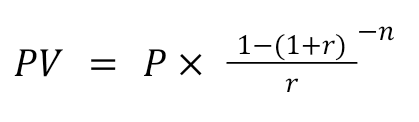

Annuity buyers can invest in a bulk payment or a series of payments over a period. When buyers invest in bulk and receive payments from the issuer after retirement, the annuity works like a CCF. The present value of an annuity can be calculated as follows:

Where,

PV is the present value.

P is the amount of each payment

r is the interest rate per period

n is the number of periods

For bulk payments, there is only one value of P and r. Therefore, the calculation is also more straightforward, a feature of CCFs.

Differences Between Conventional And Non-Conventional Cash Flow

This table summarizes the key differences between conventional and non-conventional cash flows based on various characteristics.

| Basis | Conventional Cash Flows | Non-Conventional Cash Flows |

|---|---|---|

| Cash Flow Direction | It changes direction once | It can change multiple times |

| Initial Cash Flow | Initial outlay (always outflow) | First, cash flow can be inflow or outflow |

| Cash Flow Pattern | Follows pattern of -, +, +, +, +, etc. | Various patterns, e.g., +, -, -, +, – |

| Internal Rate of Return (IRR) Calculation | One IRR, making computation easier | Complex IRR with different discount rates |

Frequently Asked Questions (FAQs)

1. What is IRR with Non-Conventional Cash Flows?

Non-conventional cash flows IRR, or internal rate of return, is a complex concept used to assess the present value of future cash flows for projects with non-CCFs. In such cases, the challenge lies in the existence of multiple IRRs, some of which may exceed the company’s hurdle rate, while others may not. This discrepancy introduces uncertainty and may undermine confidence in the investment, potentially leading the company to reconsider or reject the project.

2. What is the Difference Between Incremental Cash Flow and Conventional Cash Flow?

Incremental cash flow represents the total income or expenses incurred by a firm as a result of undertaking a project or investment. While both incremental cash flows and CCFs are estimated before making investment decisions, they are fundamentally distinct. For example, incremental cash flows can take the form of non-CCFs involving multiple outlays and inflows.

3. When Does a Conventional Cash Flow Have a Payback Period Less Than Its Life?

When a project’s payback period is shorter than its expected life, it implies that the project generates positive cash flows in the earlier stages of its existence. This condition typically results in a positive net present value (NPV), and the internal rate of return (IRR) is likely to be zero, assuming the project follows a CCF pattern. In such cases, the project is considered financially viable.

Recommended Articles

This article has been a guide to what is Conventional Cash Flow. Here, we compare it with non-conventional cash flow & explain its examples. You may also find some useful articles here –