What Is Fixed Capital?

Fixed capital refers to the investment made by the business for acquiring long-term assets. These long-term assets do not directly produce anything but help the company with long-term benefits. If a firm invests in a building where the production process occurs, the building becomes its fixed capital.

These fixed capital assets are neither consumed in the production process nor do they get destroyed. Plus, they can be used multiple times in manufacturing the items. Some of the types of such assets include Property, Plant, and Equipment (PPE), land, vehicles, machinery, etc.

- Fixed capital refers to a business’s investments to purchase long-term assets that provide long-term benefits to the company.

- Examples of fixed capital include land, buildings, manufacturing machinery, equipment, and other assets.

- The sources of fixed capital include owner’s resources, term loans from banks or financial institutions, the issuance of shares, retained earnings, and debentures.

- Businesses use various approaches to determine whether the potential cash inflows from a fixed capital investment would outweigh the cash outflows. These approaches include Net Present Value, Internal Rate of Return, and Payback Period.

Fixed Capital Explained

Fixed capital meaning signifies the assets that businesses have to be used and reused over time in the production process. It comprises the gross fixed capital formation recorded for an organization or business.

There is no consumption of fixed capital, and it is different from working capital, which is fully utilized to finance daily business activities. In the production process, businesses do not directly consume the building. However, if the company does not have the building, it would not run the production process.

Investing in the building becomes a fixed capital because this building will serve the business for a long period, and the building can be referred to as a long-term asset.

If the company decides to sell out the building in the future, it will get a residual value even if its economic usefulness is exhausted.

Factors

As fixed capital is important for running a business, it is important to know which long-term assets one should invest in.

One should do it by comparing the value of a particular long-term asset with how much cash flow it would generate in the long term. So, for example, let us say that a business has purchased a machine. And it has been found that the device would serve the industry for the next ten years. And using this particular machine would improve the production process and enhance the workers’ productivity. So, as a result, the business knows investing in a device is a good idea.

The businesses use three techniques to determine whether the potential cash inflows would outweigh the cash outflows.

- Net Present Value (NPV): This technique helps a business see its present value of future cash inflow and easily compare whether it is a good idea to invest in the asset.

- Internal Rate of Return (IRR): IRR helps determine the right rate of return with a lot of trial and effort. If the IRR seems good, investing in a long-term asset is wiser.

- Payback Period (PP): If you invest in an asset, it will return the cash outflow within how much time. For example, if a business has to decide between investing in “Building A” and “Building B” and if the payback period of A and B are 5 and 10, respectively, the business should choose to invest in A (depending on the amount invested is similar).

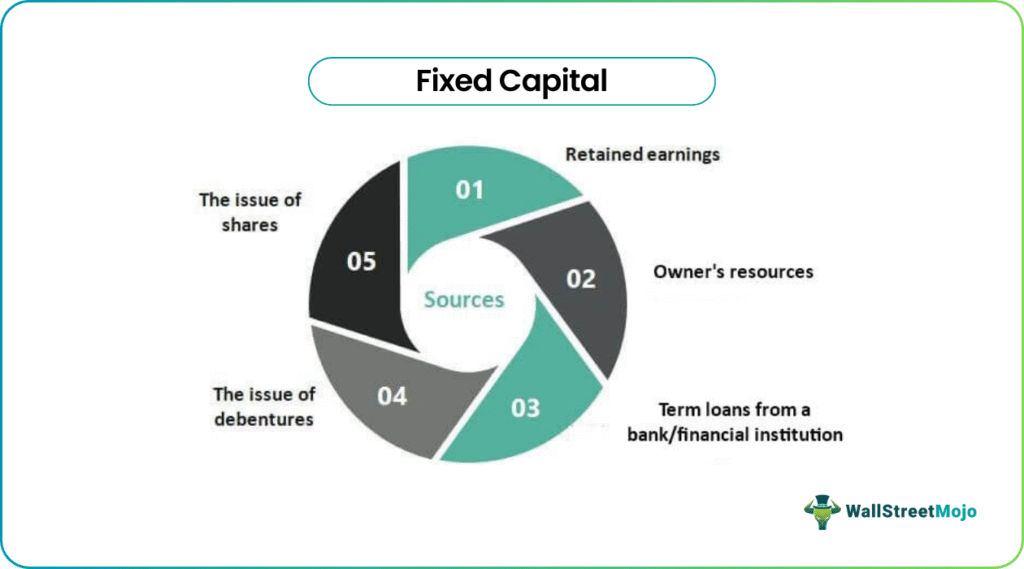

Sources

There are many sources of fixed capital. Let us have a look at them one by one: –

- Owner’s resources: This is fixed capital’s first and foremost source. Since fixed capital is a must-have in starting a business, the owner sources it from his resources.

- Term loans from a bank/financial institution: If the owner does not have enough money to invest in fixed capital, they would take help from the bank or any financial institution and take a loan against the mortgage or the mortgage. If the loan amount is larger, the owner has to arrange a mortgage to take the loan; if the loan amount is smaller, the owner does not need to organize any mortgage to avail of the loan.

- The issue of shares: If a company feels that it has to issue shares to finance the immediate need of buying/acquiring long assets, we can call it fixed capital. A private company can become public by conducting an IPO. A public company can issue new shares to finance fixed capital.

- Retained earnings: When a company needs to invest in fixed capital, it can use internal finance also. Retained earnings are a portion of the profit retained and reinvested into the company. Usually, retained earnings are invested in acquiring new fixed capital.

- The issue of debentures: By issuing debentures, companies source funding for developing long-term assets. Companies issue bonds. People interested in investing in a company buy those bonds and pay the money for them. And the companies then use that money to acquire long-term / non-current assets.

Examples

Let us consider the following fixed capital examples to gain a better understanding of the process:

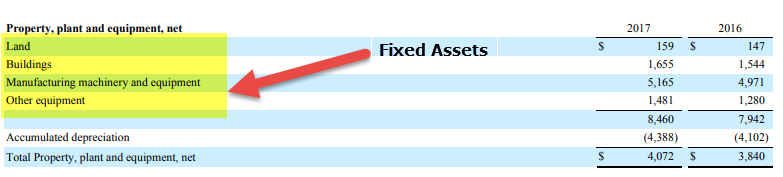

The following is an excerpt from Colgate SEC filings. Here, we can find many fixed capital examples: –

- Land

- Building

- Manufacturing machinery and equipment

- Other equipment.

Also, please note that intangible assets like patents and copyrights are classified as examples of fixed capital investments.

Importance

There are multiple reasons for which fixed capital in a business. Let us take a simple example to illustrate this.

Let us say that Peter wants to start a bookselling business. He has lots of old books lying around in his house. Peter knows that they are valuable, and most are out of print. So, he can charge a premium to sell those books.

The challenge is, where does he start his business? He does not have any place to open a shop. So, he talks to his old friend Sam and tells him he wants to buy a shop in the town. But now the issue is that he needs furniture to stack up books and arrange them so that the shop looks nice.

He asks a local carpenter to build a structure to adorn his books. Within 15 days, everything is completed, and Peter starts his business. But, if Peter had not invested in a shop or furniture, could he start his business?

The answer is “No.” Here the “shop” and the “furniture” are Peter’s fixed capital, without which he could not start his business.

Frequently Asked Questions (FAQs)

1. What is fixed capital vs. working capital?

Fixed capital refers to a business’s long-term, tangible assets that are necessary for its operations, such as land, buildings, and machinery. On the other hand, working capital refers to the short-term assets and liabilities of a business that are used in day-to-day operations, such as inventory and accounts payable.

2. What is the consumption of fixed capital?

Consumption of fixed capital is a non-cash expense that reflects the depreciation of a company’s fixed assets over time. It represents the decline in the value of an asset due to factors such as wear and tear, obsolescence, and physical deterioration. This expense is accounted for in the income statement and is deducted from a company’s revenue to arrive at its net income.

3. What is the capitalization of fixed assets?

Capitalization of fixed assets refers to recording the cost of a fixed asset as an asset on a company’s balance sheet rather than as an expense on its income statement. This is done by depreciating the asset over its useful life and adding the annual depreciation expense to the asset account.

Recommended Articles

This article has been a guide to what is Fixed Capital. We explain it with examples, factors affecting requirements, sources, and importance. You may also have a look at the following articles to learn more about corporate finance: –