Part of our Cost of Capital guide

Risk Premium Formula Explained

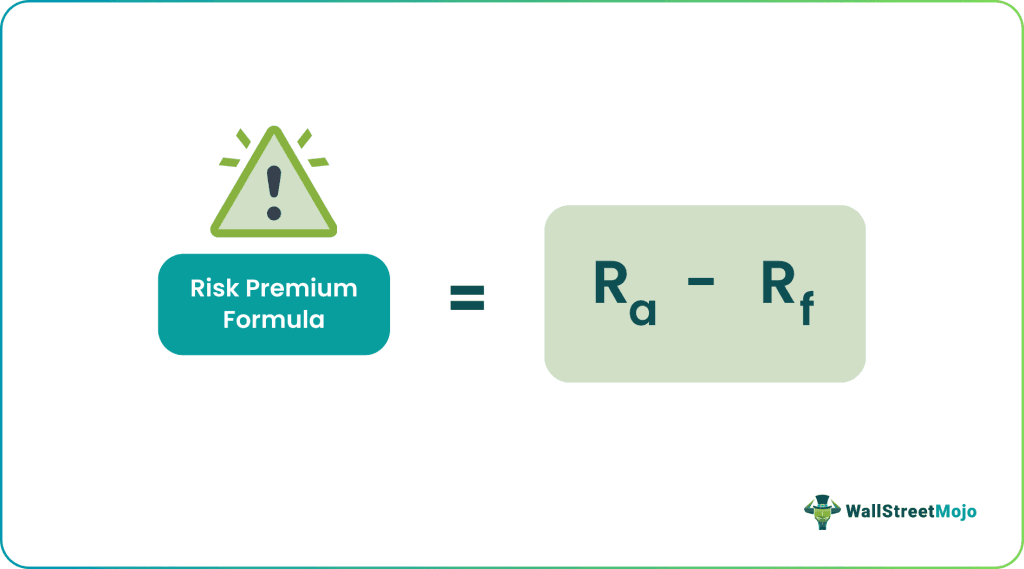

The expected risk premium formula uses the concept of risk premium which is the additional or extra compensation that the investor will expect to get from the investment. This return depends on the risk level that the investment is associated with. The formula which can be used for the calculation depends on the type of asset and the risk level.

Different approaches or models exist in the financial market regarding market risk premium formula, which the traders, investors and analysts commonly use for premium estimation. The premium is the amount that compensates the investor for the risk. This risk can arise due to various reasons like lack of proper management, financial performance is not up to the mark, or due to fluctuation in economic or political conditions.

It is to be noted that no asset is totally free of risk, even though analysts consider the debt securities that are issued by the government of the US to be risk-free virtually. This is because it is a rare possibility that the government is not able to honor the payment of treasury bills or bonds.

Likewise, even many corporates which fall under the blue chip company category, issue bonds. They are often considered free of any risk because of strong balance sheets that they have. However, these companies may also default on their payment.

Thus, stock are considered have very high risk and thus, the premium is also very high.

How To Calculate?

Let us look at some of the formulas used to calculate risk premiums in the financial market.

Specific premium forms can also be calculated separately, known as the market risk premium formula and Risk Premium formula on a Stock using CAPM. The former calculation aims to calculate the premium on the market, which is generally taken as a market index like the S&P 500 or Dow Jones. It is achieved by subtracting returns on a risk-free investment from a probable return on a similar investment in a specific market index.

Market Risk Premium = Rm – Rf

The expected risk premium formula on a stock using CAPM is intended to help understand what other returns can be had with investment in a specific stock using the Capital Asset Pricing Model (CAPM). The risk premium for a specific investment using CAPM is beta times the difference between the returns on a market investment and a risk-free investment.

Expected Return = rf + Beta (rm – rf)

Example

Given below is a suitable example that will help us to understand the concept better.

Person ABC wants to invest 100,000 US$ for the best returns possible. ABC has the option to invest in risk-free investments like the US treasury bond, which offers a low rate of return of only 3%. On the other hand, ABC is considering an investment in a stock that can give returns up to 18%. To calculate the risk premium example for taking on the extra amount of risk involved with this stock investment, ABC would carry out this mathematical operation:

Risk Premium = ra (100,000 x 18 / 100) – rf (100,000 x 3 / 100) = 18,000 – 3000 = 15,000 US$

Hence, in this case, ABC enjoys a 15,000 US$ risk premium example with this stock investment compared to the risk-free investment. However, it entirely depends on the stock’s performance and if the investment outcome turns out to be positive. For this, ABC would need to understand the risk factor involved by studying the fundamentals of the stock at length and assess if this investment is worth it and whether he would be able to realize the risk premium or not.

Thus, the above example clearly explains the process of making the calculation using the market or equity risk premium formula. It also tell us what are the factors that we should keep in mind while using the concept so that it is possible to earn maximum return by keeping the risk under control.

Risk Premium Formula For US Market

Here, we have considered a ten-year Treasury Rate as the Risk-free rate. Some analysts also take a 5-year treasury rate as the risk-free rate. Please check with the research analyst before taking a call on this.

source – bankrate.com

Market Risk Premium (RM – RF)

Each country has a different Risk Premium. Equity Risk Premium primarily denotes the premium expected by the Equity Investor. For the United States, Equity Risk Premium is 6.25%.

source – stern.nyu.edu

- Market premium = Rm – Rf = 6.25%

- Rf = 2.90%

- Expected Return from the Equity Market = Rm = Rf + Market Premium = 2.90 + 6.25% = 9.15%

Use And Relevance

The formula has uses in different types of risk premium calculation.

In case of equity, the premium is very high. Thus, here, the risk-free rate is deducted form the expected return to get the premium value using the equity risk premium formula. The expected return is the normal level of compensation that the investor will want an the risk free rate is represented by government bonds.

There is a certain amount of risk in corporate bonds, which can be measured using this formula, where the risk-free rate is again deducted from the yield on corporate bonds. The yield is what the bond issuer needs to pay the bondholders.

It must be carefully understood that market premium seeks to help assess probable returns on investment compared to any investment where the risk level is zero, as in the case of US-government-issued securities. This additional return on a risk-laden investment is in no way promised or guaranteed in this calculation or by any related factor. Should this investment outcome be negative, the premium calculation would have little relevance. The risk that an investor agreed to take upon in return for extra returns should the investment have a positive outcome. The difference between anticipated and actual returns on any investment must be understood clearly.

Risk Premium Formula In Excel (with excel template)

Let us now do the same liquidity risk premium formula example above in Excel. It is very simple. You need to provide the two inputs of investment return and risk-free return.

We can easily calculate this premium in the template provided.

Frequently Asked Questions (FAQs)

What is the equity risk premium formula?

By subtracting the risk-free return from the expected asset return or assuming that current valuation multiples are roughly accurate, the equity risk premium is calculated as the difference between the estimated actual returns on stocks and safe bonds

Does risk premium increase during a recession?

The risk premium is more considerable during a recession since so many companies would fail now. It increases due to the increased chance of corporate bond default.

What happens when the risk premium increases?

The required rate of return rises in proportion to the market risk premium. The only method to boost recovery is to pay less for the security, supposing all other factors, like the PE ratio, stay the same. Raising the required rate of return increases the risk-free rate of return.

Does the risk premium change over time?

Yes, the risk premium can change over time due to fluctuations in economic conditions, market sentiment changes, and investor risk appetite shifts. In times of economic uncertainty, investors may demand a higher risk premium, leading to lower asset prices and higher expected returns.

Recommended Articles

This has been a guide to what is Risk Premium Formula. We explain the formula using excel along with example, how to calculate & premium in US market. Here we also provide you with a Risk premium Calculator with a downloadable excel template.