Part of our Cost of Capital guide

What Is Country Risk Premium?

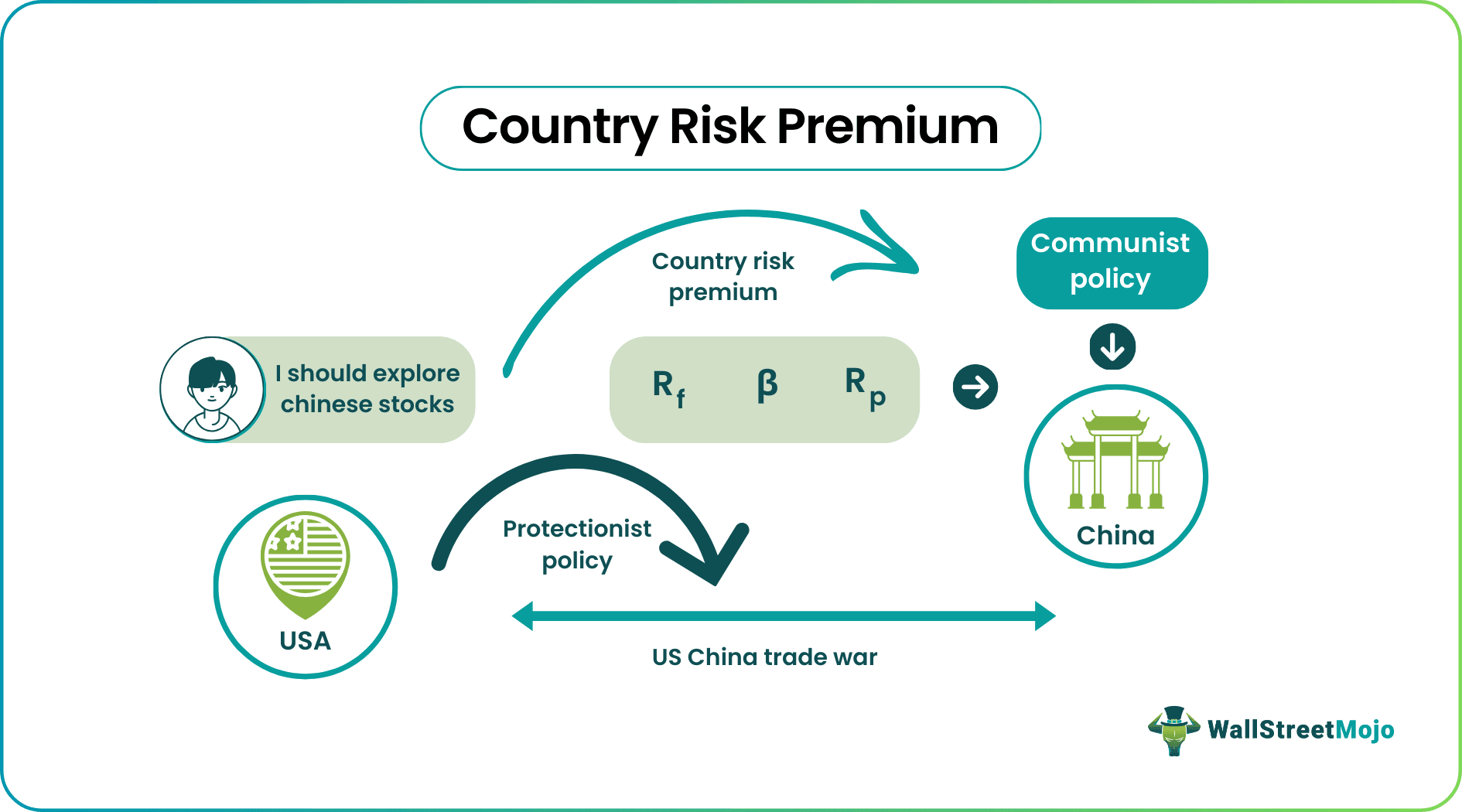

Country Risk Premium (CRP) is the additional returns expected by the investor to assume the risk of investing in foreign markets compared to the domestic country.

Investing in foreign countries has become more common now than it was before. For example, United States investors might like to invest in the securities of Asian markets, e.g., China or India. That is as much alluring as risky as it is. However, the geopolitical scenario is not the same in different world regions. There are risks associated with every economy, and a country’s risk premium measures this risk. Since the certainty of investment returns in foreign markets is generally less than in domestic markets, It becomes vital here.

We have taken a hypothetical example. Here, China faces its own set of macroeconomic risks. These risks make investors skeptical about their investments. For any given asset, market risk premium, as many analysts believe, does not capture the excess threat posed by the economic factors of the country.

Factors to consider while estimating Country risk premium:

- Macroeconomic factors like inflation.

- Currency fluctuations.

- Fiscal deficit and related policies;

Key Takeaways

- Country Risk Premium (CRP) refers to the extra returns the investor anticipates to assume the investment risk in foreign markets compared to the domestic country.

- When determining the Country’s Risk Premium, macroeconomic factors such as inflation, currency fluctuations, fiscal deficit, and concerned policies must be considered.

- The equity risk premium encourages investors to invest in risky assets in domestic markets. Moreover, it offers further force to take uncertainties in foreign markets.

- It is a dynamic statistic. In addition, it must be continuously tracked and updated in financial markets and investment analyses.

Country Risk Premium Calculation

The rates on sovereign bonds can be used to calculate country risk premia because these assets provide a good picture of a country’s macroeconomic situation. Put another way, it combines the equity and bond market indices to improve risk measurement. Both of these markets have large sums of investor money, making them more accurate country risk indicators.

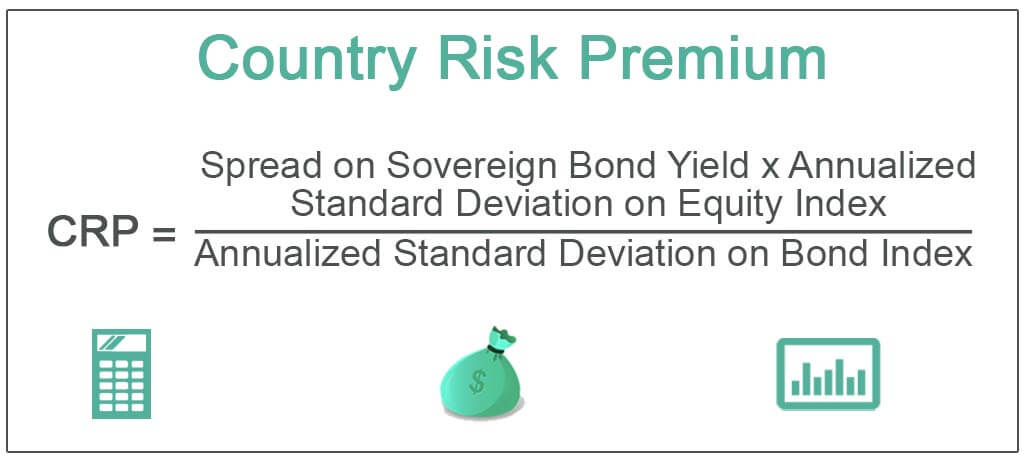

Country Risk Premium Formula

The formula for Country risk premium is:

CRP = Spread on Sovereign Bond Yield * (Risk Estimate on Equity Index Annualized / Risk Estimate on Bond Index Annualized)

Thus, more technically,

CRP = Spread on Sovereign Bond Yield * Annualized Standard Deviation on Equity Index / Annualized Standard Deviation on Bond Index

Examples

Let us see some examples of country risk premium to understand it better.

Example #1

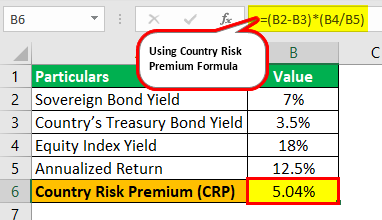

If a country has an annualized return of 18% and 12.5% on equity and bond index, respectively, over 5 years, what is the country’s risk premium? The country’s treasury bond has yielded a 3.5% return. In contrast, the sovereign bond has a 7% yield in a similar period.

Solution:

Simple substitution in the formula above gives us the CRP.

- CRP = (7% – 3.5%) x (18%/12.5%)

- CRP = 3.5% x 1.44%

- CRP = 5.04%

Example #2

Calculate the CRP with similar yields as the example above, other than the equity index yield of 21%.

Solution:

Again, putting the values in the formula, we get:

- CRP = (7% – 3.5%) x (21%/12.5%)

- CRP = 5.88%

Notice that as the equity index yield increases from 18% to 21%, the CRP increases from 5.04% to 5.88%. That can be attributed to the higher volatility in the equity market, which has produced a higher return and raised the CRP with it.

Country Risk Premium Calculation & CAPM

Country risk premium finds most use in the CAPM (Capital Asset Pricing Model) theory. A CAPM model is a measure of return on equity considering the non-systematic risk or firm risk when,

- Re is the return on equity,

- Rf is the risk-free rate,

- Β is the Beta or market risk, and

- Rm is return expected from the market.

We have two approaches to estimating rebased on the inclusion of CRP.

- One way to include Country Risk Premium (CRP) is to add it to the risk-free and risky asset component. Hence,

- Another way to include CRP in the CAPM model is to make it a function of firm risk.

Approach 1 differs from 2 in that country risk is unconditional addition to every firm’s risk-return profile.

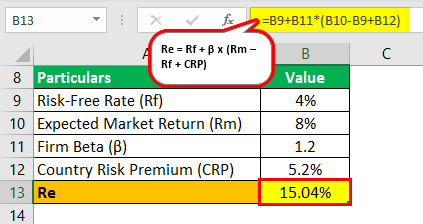

Example #3

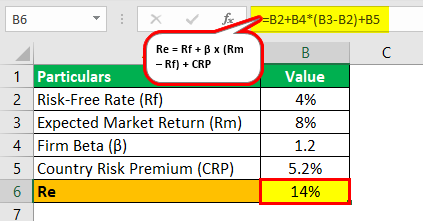

Calculate the return on equity from the following information:

- Risk-Free Rate (Rf): 4%

- Expected Market Return (Rm): 8%

- Firm Beta (β): 1.2

- Country Risk Premium: 5.2%

Solution:

From both approaches, we have the following results:

Approach 1

- Re = Rf + β x (Rm-Rf) + CRP

- Re = 4% + 1.2 x (8% – 4%) + 5.2%

- Re = 14%

Approach 2

- Re = Rf + β x (Rm-Rf + CRP)

- Re = 4% + 1.2 x (8% – 4% + 5.2%)

- Re = 15.04%

Investors’ Perspective

While the equity risk premium incentivizes investors to invest in risky assets in domestic markets, it provides further impetus to accept uncertainties in foreign markets. Some of the advantages of CRP are: –

- To a significant extent, country risk premia clearly distinguish between developed economies’ risk-return profiles against developing economies. Prof. Aswath Damodaran has summarized country risk premia and related components globally. Below is an excerpt:

| Country | Equity Risk Premium | Country Risk Premium |

|---|---|---|

| Iraq | 16.37% | 10.41% |

| India | 8.60% | 2.64% |

| Korea DPR | 22.61% | 16.65% |

| UK | 6.65% | 0.69% |

| USA | 5.96% | 0.00% |

- According to some analysts, beta does not estimate the country risk for firms, thus resulting in a low equity risk premium for the same risk ventures.

- Some scholars also argue that the risks due to a country’s macroeconomics are better captured by the cash flow positions of the firm. That raises the issue of the futility of country risk estimation as an additional level of security.

Conclusion

A country risk premium is a difference between the market interest rates of a benchmark country and that of the subject country. Of course, the less attractive economies have to offer a higher risk premium for foreign investors to attract investments.

It is a dynamic statistic that needs to be continuously tracked and updated in analyses around financial markets and investments. It assumes many factors while ignoring many others. Country risk can be better estimated when every significant aspect is appropriately valued in risk and return. Events such as the Russia-NATO conflict, tensions in the Gulf region, Brexit, etc., will certainly impact the geopolitical risk scenario.

Frequently Asked Questions (FAQs)

Does Country Risk Premium include currency risk?

The Country Risk Premium involves economic risks like recessionary conditions, higher inflation, sovereign debt burden, default probability, currency fluctuations, and unfavorable government regulations like expropriation or currency controls.

When to use Country Risk Premium?

One may utilize the Country Risk Premium when the additional premium is needed to satisfy investors for the higher risk of investing abroad. Therefore, it is essential to consider this when investing in foreign markets. In addition, it is generally higher for developing markets than developed nations.

Does equity risk premium include Country Risk Premium?

CRP is similar to Country Equity Risk Premium. The risk premium is imposed on equity investing. Often, the two terms are used interchangeably.

How does the country risk premium affect investment decisions?

The country risk premium directly affects the expected return on investment in a country. A higher country risk premium implies a higher expected return, which can attract investors seeking higher potential yields. Conversely, a lower country risk premium may make an investment less attractive than other countries with lower perceived risk. It can influence capital flows, foreign direct investment, and the cost of capital for businesses operating in that country.

Recommended Articles

This article is a guide to Country Risk Premium. We discuss its meaning, country risk premium calculation, country risk premium formula, and examples. You can learn more about finance from the following articles: –

Recommended Articles

Continue with these closely related articles from the same guide.