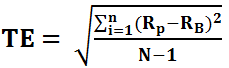

Formula for Tracking Error (Definition)

Tracking Error Formula is used in order to measure the divergence arising between the price behavior of portfolio and price behavior of the respective benchmark and according to the formula Tracking Error calculation is done by calculating the standard deviation of the difference in return of the portfolio and the benchmark over the period of time.

Tracking error is simply a measure to gauge how much the return of a portfolio or a mutual fund deviates from the return of an index it is trying to replicate in terms of the components of an index and also in the term of the return of that index. There are several mutual funds where the fund managers of that fund aim to construct the fund by closely replicating the stocks of a particular index, by trying to add stocks in his fund with the same proportion. There are two formulas to calculate the tracking error for a portfolio.

The first method is to simply make the difference between the portfolio return and the return from the index it is trying to replicate.

Tracking Error = Rp-Ri

- Rp= Return from the portfolio

- Ri= Return from the index

There is another method to calculate the tracking error of a portfolio with respect to the return from the index the portfolio is tracking.

The second method takes the standard deviation of the return of the portfolio and the benchmark.

The only difference is in this method; it is like calculating the standard deviation of return of the portfolio and that of the index the portfolio is trying to replicate. The second method is the more popular one and is used when the time series of data has a long history; in other words, when the historical data for the return of two variables are available for a longer period of time.

Key Takeaways

- Tracking Error measures the consistency of an investment or portfolio’s performance compared to a benchmark index, indicating the degree of deviation in returns.

- The Tracking Error Formula computes the standard deviation of the difference between investment and benchmark returns over a specific period, providing a statistical measure of return dispersion.

- Tracking Error helps investors and fund managers assess an investment strategy’s or portfolio management’s efficacy.

- Lower tracking error signifies closer alignment with the benchmark, while higher tracking error indicates greater divergence.

Explanation

Tracking error is a measure to find out how much the return of a portfolio or a mutual fund deviates from the return of an index it is trying to replicate in terms of the components of an index and also in the term of the return of that index. But most of the time, it doesn’t get replicated exactly in terms of the return, due to various factors like the timing of buying the stocks, the personal judgment of the fund manager to alter the proportion depending on his style of investment.

Other than these, the volatilities of the stocks in the portfolio and the various charges that are attached for an investor when they invest in a mutual fund also result in deviation of the returns of a portfolio and the index the portfolio tracks.

Examples

Example #1

Let us try to do the calculation of the tracking error with the help of an arbitrary example, say for mutual fund A, which is tracking the oil and gas index. It is calculated by the difference in the return of the two variables.

Tracking Error calculation = Ra – Ro&G

- Ra= Return from the portfolio

- Ro&g= return from the oil and gas index

Suppose the return from the portfolio is 7%, and the return from the benchmark is 6%. The calculation will be as follows,

In this case, the tracking errors for the portfolio will be 1%.

Example #2

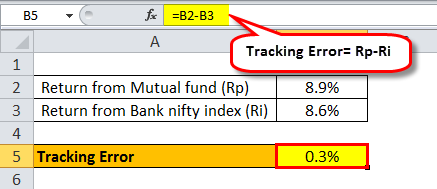

There is a mutual fund managed by a fund manager in SBI. The name of the fund in question is SBI- ETF Nifty Bank. This particular fund is constructed by taking the components of bank nifty closely in the proportion by which the banking stocks are in the bank nifty index.

Tracking Error = Rp-Ri

One year return from the portfolio is 8.9%, and the one-year return from the Nifty benchmark index is 8.6%.

In this case, the tracking errors for the portfolio will be 0.3%.

Example #3

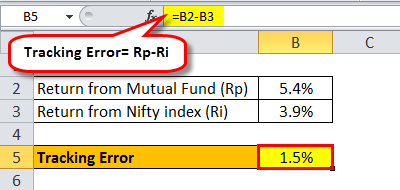

There is a mutual fund managed by a fund manager in Axis Bank. The name of the fund in question is Axis Nifty ETF. This particular fund is constructed by taking the components of the nifty 50 closely in the proportion by which the index stocks are in the Nifty index.

One year return from the portfolio is 5.4%, and the one-year return from the Nifty benchmark index is 3.9%.

In this case, the tracking errors for the portfolio will be 1.5%.

Use of Tracking Error Formula

It helps the investors of a fund to understand whether the fund is closely tracking and replicating the components of the index it is putting up as a benchmark. It showcases whether the fund manager is trying to actively track the benchmark or he is putting his style in order to modify it. It also helps the investors to find out whether the charges are high enough for the fund to impact the return of the fund.

Frequently Asked Questions (FAQs)

1. How is Tracking Error different from Alpha?

Tracking Error measures the variability in returns between an investment and its benchmark, providing insight into how much the investment deviates from its benchmark performance. In contrast, Alpha represents the excess return of an investment over its benchmark, indicating the investment manager’s ability to generate additional returns.

2. What is a satisfactory level of Tracking Error?

The satisfactory level of Tracking Error depends on the investment strategy and investor’s objectives, and it varies across different investment styles and asset classes. For example, active managers may aim for a higher Tracking Error to justify their active management fees. Conversely, passive managers may strive for a lower Tracking Error to closely track the benchmark and minimize deviations

3. What are the limitations of the Tracking Error Formula?

The Tracking Error formula has several limitations. Firstly, it relies on historical data, which may not accurately reflect future market conditions. Secondly, it may fail to capture all sources of risk, such as style drift or liquidity risk. Thirdly, benchmark selection and rebalancing frequency can affect the formula’s accuracy, as different benchmarks and frequencies can yield different Tracking Error results.

Recommended Articles

This has been a guide to Tracking Error Formula. Here we discuss how to calculate tracking error for the portfolio along with examples and a downloadable excel template. You can learn more about financing from the following articles-