Part of our Investment Performance Metrics guide

What is the Nominal Rate of Return?

A nominal rate of return is nothing but the total amount of money that is earned from a particular investing activity before taking various expenses like insurance, management fees, inflation, taxes, legal fees, staff salaries, office rent, depreciation of plants and machinery, etc into the due consideration. It’s the basic return offered by investment and post deducting inflation and taxes in the investment period, the actual return would be relatively lower.

- The nominal rate of return is a measure that indicates the overall percentage increase or decrease in the value of an investment without adjusting for inflation.

- To calculate the nominal rate of return, subtract the initial investment amount from the final investment value, divide the result by the initial investment amount, and then multiply by 100 to express it as a percentage.

- The nominal rate of return provides a fundamental understanding of an investment’s performance and can be valuable for comparing different investment options.

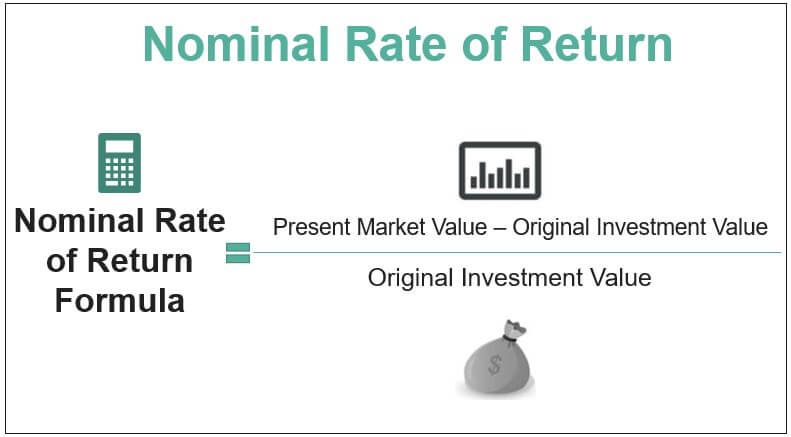

Formula

The formula for the nominal rate of return is represented as follows :

Examples

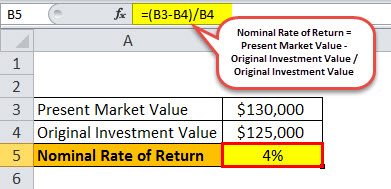

Example #1

An individual has made an investment of $125,000 in a no-fee fund for a time of 1 year. At the end of the year, the value of investment increases to $130,000.

Therefore, the nominal rate of return can be calculated as follows,

= ($130,000 – $125,000 )/$125,000

Nominal Rate of Return = 4%

While computing returns from investments, the difference between nominal rate and real return is determined, and this will adjust to the existing purchasing power. If the expected inflation rate is high, the investors would further expect a higher nominal rate.

One should note that this concept can be misleading. For instance, an investor may be holding a Government/Municipal Bond and a Corporate bond that has a face value of $1,000 with an expected rate of 5%. One would assume that the bonds are of equal value. However, corporate bonds are generally taxed @25-30% in comparison to Government bonds, which are tax-free. Thus, their real rate of return is completely different.

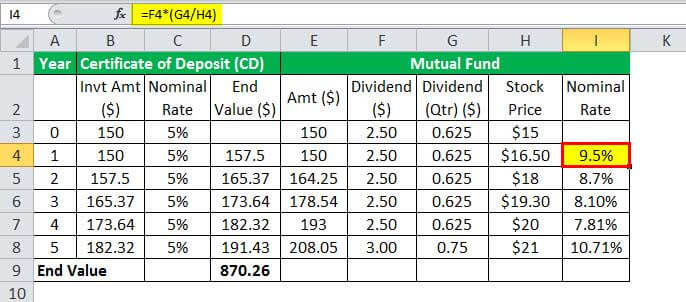

Example #2

Assume Andrew purchases a CD (Certificate of Deposit) worth $150 at an annual rate of interest of 5%. Thus, annual earnings is = $150 * 5% = $7.50.

On the other hand, if Andrew invests $150 in a reputed Mutual fund, which also generates an annual return of 5%, the annual return will still be $7.50. However, a mutual fund offers an annual dividend of $2.50, causing a difference in the two classes of investments.

The below table shall be helpful in understanding the differences:

(End Value = Base Investment Amount * Nominal Rate)

- Year 1 = 2.50 * (0.625 / 16.5) = 9.50%

- Year 2 = 2.50 * (0.625 / 18) = 8.70%

- Year 3 = 2.50 * (0.625 / 19.3) = 8.10%

- Year 4 = 2.50 * (0.625 / 20) = 7.80%

- Year 5 = 3.00 * (0.750 / 21) = 10.70%

Since the mutual fund is offering a dividend as well, the quarterly dividend is computed and multiplied with the stock price to compute the Nominal Rate of Return.

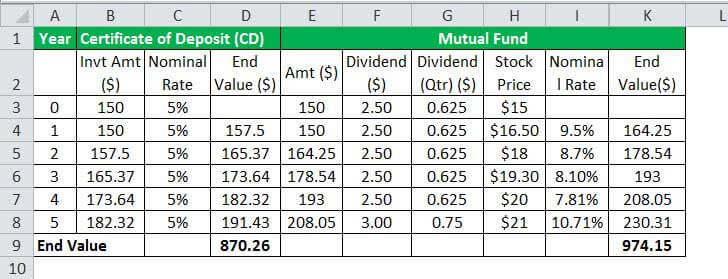

One should make a note that despite both investment opportunities offering an identical rate of return, factors such as dividends, in this case, have a direct impact on the nominal rate of return, which is being offered.

The above example also takes into consideration the change in dividend and the direct impact it has on the nominal rate.

Real vs. Nominal Interest Rates

→ Explore all 43 Interest Rates articles

Economists make extensive use of real and nominal interest rates while assessing the value of investments. In fact, the real rate uses Nominal Interest rate as a base from which the impact of inflation is reduced:

Real Interest Rate = Nominal Interest Rate – Inflation

However, there are certain differences in both concepts:

| Real Interest Rate | Nominal Interest Rate |

|---|---|

| It’s adjusted to eliminate the impact of inflation, reflecting the real cost of funds to the borrower and the real yield to investors. | It does not factor out the inflation impact. |

| It offers a clear idea of the rate at which their purchasing power increases or decreases. | Short-term rates are set by the Central Bank. They can keep it low to encourage customers to assume more debt and increase spending. |

| It can be estimated by comparing the difference between Treasury Bond Yield and Inflation-Protected Securities of the same maturity. | Rate is quoted on loans and bonds. |

How to Calculate Real Interest Rates from Nominal Interest Rate?

This exercise can be very useful in understanding the impact of economic factors such as inflation and taxes. Also, from the perspective of various investments, one may want to know how much a Dollar invested is expected to yield in the future.

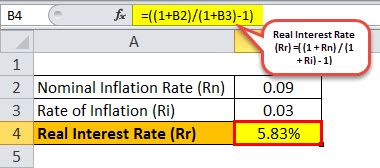

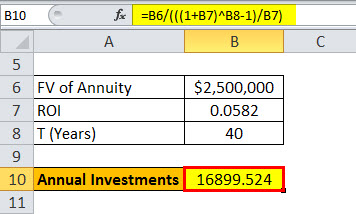

Let’s assume, Archie is currently 25 years old and has a plan to retire at the age of 65 years (40 years from present). He expects to accumulate around $2,500,000 in current dollars at the time of his retirement. If he can earn a nominal return of 9% per year on his investments and expect a rate of inflation around 3% annually, how much must be his investment amount every year to meet the goal?

The relationship between nominal and real interest rates is a bit complex, and thus the relationship is multiplicative and not additive. Thus, Fisher’s equation is helpful, whereby:

Real Interest Rate (Rr) =( (1 + Rn) / (1 + Ri) – 1)

Whereby, Rn = Nominal Inflation Rate and Ri = Rate of Inflation

Thus, Rr = (1+0.09) /(1+0.03) – 1

1.0582 – 1 = 0.0582 = 5.83%

The annual investment using the Future Value formula of Annuity

This signifies that if Archie makes a saving of $16,899.524 (in today’s dollars) every year for the next 40 years, he would have $2,500,000 at the end of the term.

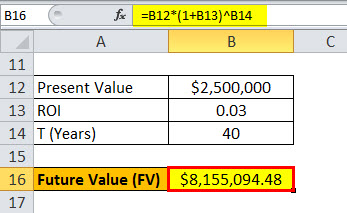

Let us look at this problem the other way around. We need to establish the value of $2,500,000 in its present value using the Future Value formula:

FV = 2,500,000 (1.03)40 = 2,500,000 * 3.2620

FV = $8,155,094.48

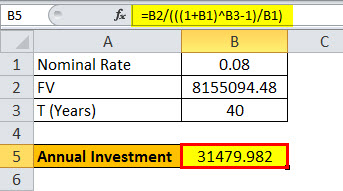

This means that Archie will have to accumulate over $8.15 mm (Nominal rate) at the time of retirement for achieving the goal. This will further be solved using the same formula of FV of Annuity assuming an 8% nominal rate:

Thus, if Archie were to invest an amount of $31,479.982, the goal will be achieved.

It should be noted here that the solutions are equivalent, but there is a difference due to inflation adjustment every year. Therefore, we are required to grow each payment at the rate of inflation.

The nominal solution requires an investment of $31,480.77, whereas the real interest rate after accommodating inflation requires an investment of $16,878.40, which is a more realistic scenario.

Frequently Asked Questions (FAQs)

1. What are the applications of the nominal rate of return?

The nominal rate of return is widely used in finance and investing. It is commonly employed in various applications, such as portfolio performance evaluation, financial planning, and assessing the profitability of investments. By considering the actual cash flows received or paid during a specific period, the nominal rate of return helps investors and analysts assess the growth or decline of their investments.

2. Can the nominal rate of return be negative?

Yes, the nominal rate of return can be negative. A negative nominal rate of return indicates a loss or decline in the value of an investment over a given period. For example, this can occur when the investment’s value decreases, resulting in a negative return.

3. What are the limitations of a nominal rate of return?

The nominal rate of return has certain limitations. Firstly, it does not account for inflation, which can significantly impact the purchasing power of investment returns. Therefore, to assess the real value of an investment, it is essential to consider the inflation-adjusted or real rate of return. Additionally, the nominal rate of return may not capture other costs, such as taxes, fees, or transaction costs, which can affect the overall returns.

Recommended Articles

This has been a guide to Nominal Rate of Return & its definition. Here we discuss how to calculate the Nominal Rate of Return using its formula and examples. You may learn more about accounting from the following articles –