Written byRutan BhattacharyyaRutan BhattacharyyaFinance Content Writer & EditorRutan is a Finance and AI Content Strategist specializing in content development, digital learning, and audience growth. He creates and manages finance and AI content across articles, blogs, YouTube scripts, and course landing pages while coordinating cross-functional course development and video production5+ years of experienceMutual FundsStocksView Full Profile

Reviewed byDheeraj Vaidya, CFA, FRMDheeraj Vaidya, CFA, FRMContent Reviewer & Course DirectorDheeraj is a former J.P. Morgan and CLSA Equity Analyst with nearly two decades of experience in financial modeling, valuation, equity research, and corporate finance. He specializes in helping students and professionals develop practical and in-demand finance skills through structured and AI-powered,20+ Years of experienceCFA, FRM, IIT Delhi, IIM LucknowFinancial ModelingView Full Profile

UpdatedFeb 7, 2025

Read Time12 min

What is Treynor Ratio?

Treynor ratio is a metric widely used in finance for calculations based on returns earned by a firm. It is also known as a reward-to-volatility ratio or the Treynor measure. The metric got its name from Jack Treynor, who developed it and used it first. A higher number indicates a more suitable investment or is considered a good Treynor ratio.

The Treynor ratio is similar to the Sharpe ratio, where excess return over the risk-free return, per unit of the volatility of the portfolio, is calculated with the difference that it uses beta instead of standard deviation as a risk measure, hence it gives us the excess return over the risk-free rate of the return, per unit of the beta of the overall portfolio of the investor.

The Treynor ratio is comparable to the Sharpe ratio, which determines the excess return over the risk-free return per unit of portfolio volatility. This method uses beta as a risk measure instead of standard deviation. It calculates excess return over the risk-free rate per unit of the investor’s portfolio beta.

It measures the additional profits a company could have earned on certain assets based on market risk. It helps managers make informed investment decisions.

It assesses portfolio performance by measuring profits. It was named after its inventor, Jack Treynor. A higher ratio indicates better performance.

Treynor Ratio Explained

Treynor Ratio can be explained as a number that measures the excess returns the firm could have earned by some of its investments with no variable risks, assuming the current market risk. The Treynor ratio metric helps managers relate the returns earned in excess over therisk-free rate of return with the additional risk that has been taken.

Ratios that use the beta, the Treynor ratio being one of those, could also be best fitted to compare short-term performance. There have been a lot of studies on the long-term stock market performance, and a study of Buffett’s record at Berkshire Anne Hathaway has shown that low beta stocks have performed better than high beta stocks, whether on a risk-adjusted basis or in terms of raw, unadjusted performance basis.

It must be noted here that the direct and linear relationship between higher beta and higher long-term returns might not be as robust as it is believed to be. Academics and investors will invariably argue about the most effective strategies for activity risk for years to come. In truth, there may be no measure to be regarded as the perfect measure of risk. However, despite this, the Treynor ratio will at least offer you some way to match the performance of a portfolio by considering its volatility and risk, which can create more helpful comparisons than just a simple comparison of past performances.

Formula

In the Treynor ratio formula, we don’t consider the entire risk. Instead of that, systematic risk is considered. The understanding of the formula shall give us a clear understanding of the concept and its related factors and shall help us identify a good Treynor ratio as well.

Treynor ratio formula is given as:

Here, Ri = return from the portfolio I, Rf = risk free rate and βi = beta (volatility) of the portfolio,

The higher the Treynor ratio of a portfolio, the better its performance. Therefore, when analyzing multiple portfolios, using the Treynor ratio formula as a metric will help us analyze them successfully and find the best among them.

How To Calculate?

Treynor ratio calculation is done by considering the beta of an investment to be its risk. The β value of any investment is the measure of the investment’s volatility in the current stock market position. The more the volatility of the stocks included in the portfolio, the more the β value of that investment will be.

The β value can be measured, keeping the value of 1 as a benchmark. The β value for the whole market is taken equal to 1. A portfolio with a high number of volatile stocks will have a beta value greater than 1. On the other hand, if an investment has only a few volatile stocks, the β value of that investment will be less than one, indicating a negative Treynor ratio.

Stocks with a higher beta value have more chances to rise and fall more easily than other stocks in the stock market with a relatively lower beta value. So when considering the market, the average comparison of beta values cannot give a fair result. Hence, comparing investments with this measure is not practical. So here comes the utility of the Treynor ratio because it helps compare investments or stocks with nothing common to get a clear performance analysis.

Examples

Now that we have an understanding of a good and negative Treynor ratio and the outline of the concept, let us apply this theoretical knowledge into practical situations through the examples below.

Example #1

Investment

Beta Value

Percentage of Return

Investment A

1.00

10%

Investment B

0.9

12%

Investment C

2.5

22%

To carry out the Treynor Ratio calculations, we also need the risk-free rate of the three investments. Let us assume all three investments here have a risk-free rate of 1.

Now we can carry out the Treynor Ratio calculation by using the Treynor ratio formula, which is as follows: –

For investment A, the Treynor ratio formula comes out to be ( 10 – 1 ) / (1.0 * 100) = 0.090

For investment B, the Treynor ratio comes out to be ( 12 – 1 ) / (0.9 * 100) = 0.122

For investment C, the Treynor ratio comes out to be ( 22 – 1 ) / (2.5 * 100) = 0.084

We can notice from the obtained Treynor ratio values that Investment B has the highest Treynor ratio; hence, this is the investment with a relatively lower beta value. Therefore, the Treynor ratio for Investment A is 0.090, for Investment B is 0.122 and for Investment C is 0.084. So, in this case, Investment B is said to be the investment with the best performance among the three investments we have analyzed. Similarly, Investment A is the second-best, while Investment C is the lowest-performing investment among the three.

Now, let us consider the raw analysis of the performance of the investments. When we look at the return percentages, Investment C is supposed to perform best with a return of 22%, while Investment B must have been chosen to be the second-best. But from the Treynor ratio calculation, we have understood that Investment B is the best among the three. In contrast, despite having the highest percentage, Investment C is the worst-performing investment among the three. This difference in the results came because of the use of the measure of the risk in the Treynor ratio calculation.

Example #2

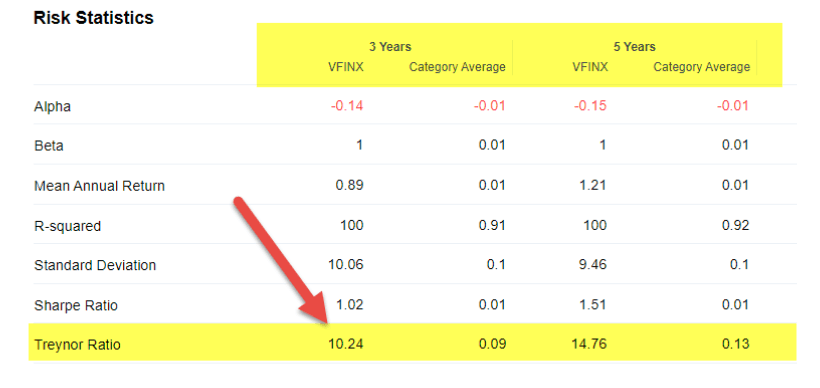

Mutual fund companies communicate the performances of their funds on a periodic basis. They communicate their performances through a document called the fact sheet. This analysis is also conducted by external companies to show investors the best funds to invest in, sector-wise.

The fact sheet has information about various types of risks. For instance, the standard deviation calculation shows the total risk involved in the fund, Beta is a measure of the market risk.

However, for seasoned investors, it is important to understand the risk-adjusted returns as well to know if the kind of risk they are taking is converted into appropriate returns. This is exactly where the analysis of a good Treynor ratio and Sharpe ratio comes into the picture.

Application in Mutual Funds

Mutual funds are considered to be a good option to invest in, and determination of the risk-free return is something you should surely consider before deciding to invest in a mutual fund. Like all other investment options, mutual funds also carry risks and are a long-term investment option; one should seriously consider all risks associated with it and always consider a mutual fund with lessrisk tolerance to provide a good rate of return from the investment.

Market risk: Market scenarios are ever-changing, and market risks largely affect mutual funds. The change in market trends can affect how investment returns income, which is true for mutual funds. The common risks involved in mutual funds are the following:

Industry risk: Industry-based risks are common in the market. Any investment in the industry in which a decline or a piece of bad news occurs will change how the market behaves. And therefore, it may affect the number of returns made.

Country risk: The particular country where the investment goes makes them affected by the country-based risks. Any scenarios taking place in that country can significantly affect how the investments behave. Things like elections, government norm changes, and natural disasters can change the rate of return investment in that country provides the investors.

Currency risk: The change in the exchange rate of currencies also affects the financial market greatly. Business organizations do business in different countries, which include multiple currencies. So the change in an exchange rate of a currency in which business is done can affect how the market behaves. So the currency risk is important to consider while calculating the Treynor ratio.

Interest rate risk: The interest rates and the bond prices are greatly related. An increase in interest rate can cause a decline in bond prices, and a reduction in the same can increase bond prices. So the risk related to the interest rate is important to consider.

Credit risks: Timely payment against the debts or loans taken by the investor is important, and a failure in this can give rise to credit risks. Credit dues can inversely affect the business of the investor.

Principal risk: Any fall in prices, like that of the equipment used by the firm, can affect the business too.

Fund manager risk: The fund manager’s job has to be done perfectly. Any error in the fund manager’s work can adversely affect the funds. This is called the fund manager risk, so the proper working of the worker in the investment firm is important to obtain a good Treynor ratio and hence a good rate of return.

As we have seen, investors must find mutual funds to help them meet their investment objectives at the required risk level. And they should realize that gauging the risk involved in a mutual fund scheme just based on the NAV of the fund reports might not be a holistic assessment. It is noteworthy that, in a fast-rising market, it’s not altogether tough to clock higher growth if the fund manager is willing to take up a higher risk. There have been many such occasions in the past, like the rallies of 1999 and early 2000, as well as manymid-cap stock rallies. Therefore, assessing the past returns clocked by the mutual fund in isolation would be inaccurate because they will not indicate the extent of risk you have been exposed to as an investor.

Limitations

Although the Treynor ratio is considered a better method to analyze and find out the better-performing investment in a group of investments, it does not work in several cases. The Treynor ratio does not consider any values or metrics calculated utilizing the management of portfolios or investments. Therefore, this makes the Treynor ratio just a ranking criterion with several drawbacks, making it useless in different scenarios.

Further, it can be effectively used for analyzing multiple portfolios only if given that they are a subset of a larger portfolio. In cases where the portfolios have varying total risk and similar systematic risks, they will be ranked the same, making this ratio useless in the performance analysis of such portfolios.

Another limitation of the Treynor ratio occurs because of the past consideration done by the metric. This ratio gives importance to how the portfolios behaved in the past. In reality, the investments or portfolios are ever-changing. We can’t analyze one with just past knowledge as the portfolios may behave differently in the future due to changes in market trends and other changes.

For example, if a stock has been giving the firm a 12% rate of return for the past several years, it is not guaranteed that it will go on doing the same thing in the years to follow. The rate of return can go either way, which is not considered by the Treynor ratio.

The Treynor ratio formula has an inherent weakness: its backward-looking design. It’s possible, maybe even more likely, for an investment to perform differently in the coming periods from how it has done in the past. For instance, a stock with a beta of 3 might not essentially have the market’s volatility thrice forever. Likewise, an investor should not expect a portfolio to make money at an 8% rate of return over the coming ten years just because it did so over the past ten years.

In addition, some might take issue with utilizing beta as a measure of risk. Several accomplished investors say that the beta and negative Treynor ratio can’t give a clear picture of the involved risk. For many years, Warren Buffett and Charlie Munger have argued that the volatility of an investment isn’t the true measure of risk. They might argue that risk is the likelihood of a permanent, not temporary, loss of capital.

Treynor Ratio vs Sharpe Ratio

Sharpe ratio is a metric similar to the Treynor ratio used to analyze the performance of different portfolios, taking into account the risk involved.

The main difference between the Sharpe ratio and the Treynor ratio is that unlike the use of systematic risk used in the case of the Treynor ratio, the total risk or the standard deviation is used in the case of the Sharpe ratio. The Sharpe ratio metric is useful for all portfolios, unlike the Treynor ratio, which can only be applied to well-diversified portfolios. The Sharpe ratio reveals how well a portfolio performs compared to a riskless investment. The common benchmarks used to represent a riskless investment are the U.S.Treasury bills or bonds.

The Sharpe ratio first calculates either the expected or the real return on investment for an investment portfolio (or even a personal equity investment), subtracts the riskless investment’s return on investment, and then divides that result by the standard deviation of the investment portfolio.

The first purpose of the Sharpe ratio is to determine whether you’re creating a considerably bigger return on your investment in exchange for accepting the additionalrisk inherent in equity investment, as compared to investing in riskless instruments. Both methodologies work for determining a “better performing portfolio” by considering the risk, making it more suitable than raw performance analysis. Thus, both ratios work similarly in some ways while being different in others, making them suitable for different cases.

Frequently Asked Questions (FAQs)

Is it possible to have a negative Treynor ratio?

A Treynor ratio can be negative in one of two ways: a negative return or a negative beta. We cannot categorically state whether one ratio is superior to another.

What is the difference between the information ratio and the Treynor ratio?

The information ratio demonstrates the fund manager’s capacity to produce active returns continuously. Better funds have information ratios. The Treynor ratio is a risk-adjusted return based on systematic risk, often known as market risk or beta.

What is a common weakness of Jensen’s alpha and the Treynor ratio?

The Treynor ratio and the Jensen alpha share the flaw that they depend on beta estimates, which can vary greatly depending on the source, resulting in an inaccurate risk-adjusted return calculation.

Recommended Articles

This has been a guide to what Treynor Ratio. Here we explain its formula, calculations, examples, and limitations, and compared it with the Sharpe ratio. You may learn more about financing from the following articles –