Part of our Investment Strategies guide

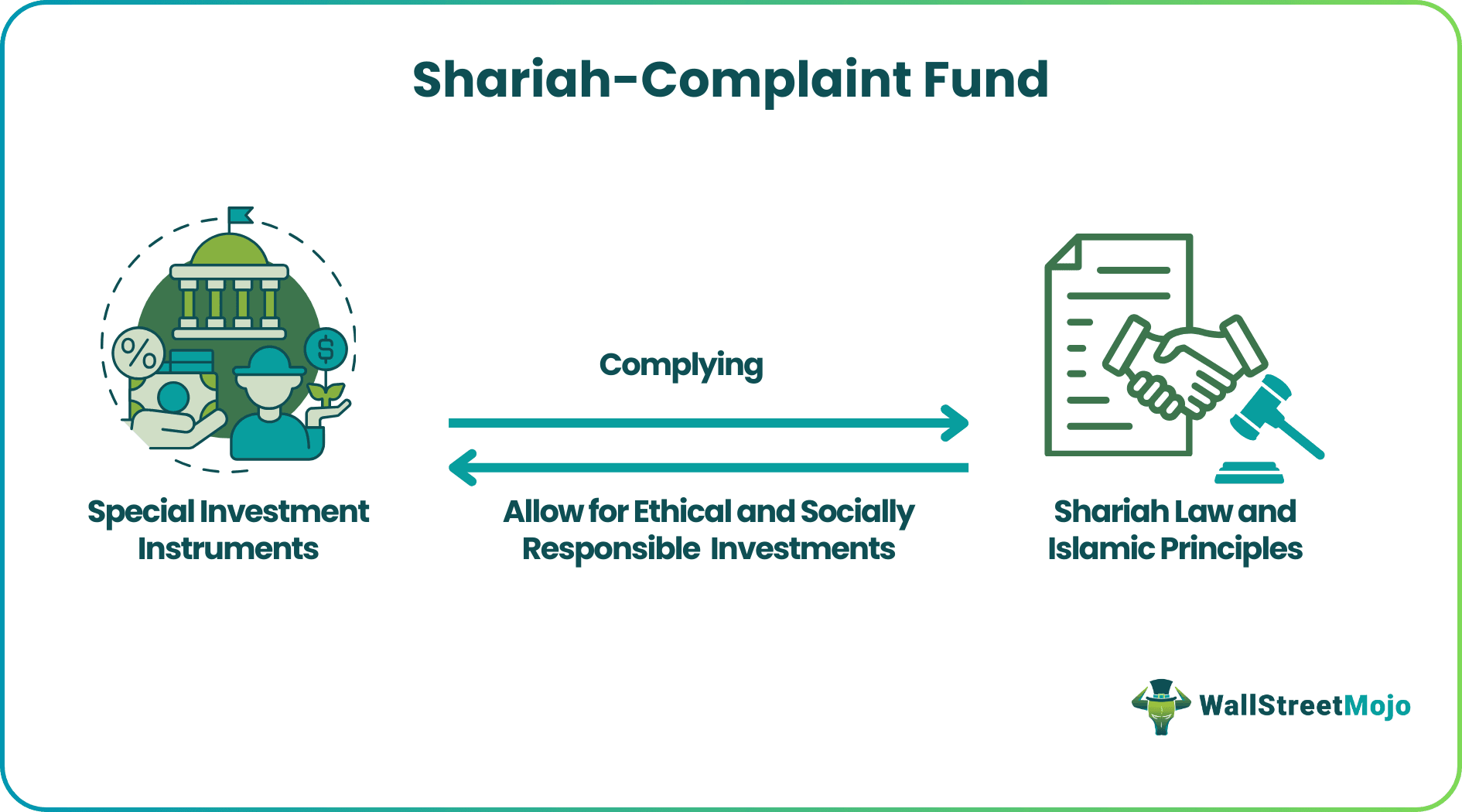

What Are Shariah-Compliant Funds?

Shariah-compliant funds are investment vehicles that adhere to Islamic principles and values. These funds are designed for investors who wish to align their investments with ethical and socially responsible guidelines outlined by Shariah law.

Like socially responsible funds falling under the Environmental, Social, and Governance (ESG) category, Shariah-compliant funds avoid investing in businesses involved in gambling, adult entertainment, pork-related products, tobacco, weapons, and alcohol. Instead, they primarily invest in real estate, exchange-traded funds, and private equity. These funds undergo a Shariah screening process to ensure compliance with Islamic principles.

- Shariah-compliant funds are Islamic investment vehicles that adhere to the Shariah principle and avoid interest, harm to the environment or humanity, and cater to ethical investors.

- These funds avoid interest-based investments but have lower liquidity than conventional funds.

- Shariah-compliant funds adhere to Islamic principles, avoid interest-based investments, involve Shariah boards for oversight, operate under profit-sharing frameworks, promote socially responsible sectors, and may have limited liquidity.

- They offer various investment categories such as equity funds, Sukuk funds, ETFs, bond funds, money market funds, real estate funds, Islamic funds, and Islamic Balanced Funds, catering to ethical investors.

Shariah-Compliant Funds Explained

Shariah-compliant funds are investment instruments governed by Shariah law and designed to conform to Islamic principles. Their operation resembles socially responsible investing, as these funds meticulously assess and categorize potential investments based on Shariah law guidelines. The rapid growth of Shariah-compliant funds can be attributed to the significant increase in petrodollar liquidity during 2002-03.

A Shariah board is established to oversee the management of Shariah-compliant funds. This board determines which sectors align with Shariah principles and may add them to the fund’s investment portfolio. Simultaneously, they have the authority to remove, restrict, or blocklist assets or investment instruments that do not adhere to these principles. This ensures that investors do not unintentionally support companies involved in illegal or harmful activities.

According to a report from the Malaysia Islamic International Financial Center, global assets within Shariah-compliant funds experienced substantial growth despite the economic challenges posed by the Covid-19 pandemic. The report also highlights a 21.2% year-on-year increase in the global sukuk market. Both sovereign and corporate/quasi-government sectors contributed to this rise.

Shariah-compliant funds serve multiple purposes. They enable Muslim investors to allocate their funds in a permissible (halal) manner, thereby promoting economic activities in Islamic nations while safeguarding society and the environment from harmful industries like alcohol and drugs.

These funds also play a crucial role in preserving the faith of Muslim investors and encouraging the adoption of profit-sharing methods over traditional interest-based banking. As a result, they have spurred the development of various financial products and indexes based on Shariah compliance, offering an alternative investment avenue that upholds ethical principles and directs investments toward Islamic nations.

Features

Many investors choose to allocate their funds to morally and environmentally friendly investments, making it essential to understand the key features of these Shariah-compliant funds:

- Alignment with Shariah: Shariah-compliant funds strictly adhere to Shariah law, following Islamic principles and guidelines.

- Restricted Investments: These funds only invest in companies that comply with Shariah law. Businesses involved in haram (forbidden) activities or usury-based practices are strictly avoided.

- Shariah Board Oversight: Shariah-compliant funds are overseen by a Shariah board responsible for ensuring compliance with Islamic law and principles.

- Profit Sharing: These funds typically operate on a profit-and-loss sharing (PLS) framework, where investors share in the profits or losses generated by the underlying assets.

- Liquidity: Shariah-compliant funds often have lower liquidity levels due to smaller market demand, making them less readily tradable.

- Costs: These funds may entail higher costs compared to conventional investments due to the increased due diligence required for Shariah compliance.

- Social Responsibility: Shariah-compliant funds promote investments in socially responsible sectors, such as renewable industries.

- Debt and Interest Restrictions: These funds maintain specific Shariah-compliant debt levels in their investments and avoid interest-bearing assets in their portfolios.

- Exclusion of Prohibited Industries: Shariah-compliant funds exclude sectors involving defense, gambling, and interest-based finance, aligning with Islamic values and ethics.

- Passive and Active Management: Shariah-compliant funds may employ passive or active management strategies. Passive strategies replicate the performance of Shariah-compliant indices, while active management involves fund managers making investment decisions.

Types

Various categories of Shariah-compliant funds cater to different investment preferences:

- Equity Funds: Sharia-compliant equity funds invest in companies that adhere to Islamic principles, making them a preferred choice for investors seeking Sharia-compliant investments.

- Sukuk Funds: These funds invest in Sukuk, Islamic bonds compliant with Shariah principles, providing returns from fixed-income investments.

- Exchange-Traded Funds (ETFs): Shariah-compliant ETFs track specific Shariah-compliant indices, offering transparent and liquid investment options akin to traditional ETFs.

- Bond Funds: Shariah-compliant bond funds invest in bonds issued by governments or companies, enabling investors to share in the profits and losses.

- Money Market Funds: Shariah-compliant money market funds, consisting of short-term debt securities, do not pay interest, aligning with Shariah principles.

- Real Estate Funds: These funds, including Real Estate Investment Trusts (REITs), invest in lawful purposes like commercial or residential properties, making them suitable for Sharia-compliant investments.

- Islamic Funds: These funds strictly adhere to Islamic finance principles and invest in permissible assets like real estate, bonds, and equities.

- Islamic Balanced Funds: Combining Sukuk and equity investments in a balanced manner, these funds offer diversified investment opportunities to investors.

Examples

Let us take the help of a few examples to understand the topic.

Example #1

SEDCO Capital, based in Saudi Arabia, is a prominent player in the field of Shariah-compliant fund management. They manage over $5.9 billion in assets with a focus on ethical and ESG-driven investments. In 2021, they expanded their offerings, including the SEDCO Capital REIT, which boosted the fund’s total assets by $187.2 million. Furthermore, they collaborated with Lombard Odier to launch an ESG-focused Shariah-compliant fund targeting developed market equities.

Example # 2

Imagine one wants to invest ethically following Islamic principles in a Shariah-compliant fund. These funds avoid interest-based investments and prioritize sharing risks while steering clear of excessive uncertainty. Technology like asset tokenization allows them to invest in assets like real estate by dividing them into smaller pieces represented as tokens on a blockchain to make this easier. This way, more investors can participate while staying in line with Shariah law.

Tokenization also benefits crowdfunding, making Islamic bonds called Sukuk more accessible, boosting market liquidity and efficiency. In essence, Shariah-compliant funds combined with tokenization provide ethical investment opportunities, appealing to those who prioritize Islamic principles in their investments.

Pros And Cons

Pros and cons are the following:

#1 – Pros

- Islamic Principles: Shariah-compliant funds follow Islamic rules, making them a good choice for Muslims seeking investments in line with their faith.

- No Interest: These funds avoid interest-based investments, which is important for investors who want to avoid such practices.

- Diversification: Shariah-compliant funds spread investments across different areas, reducing risk.

- Ethical: Investing in these funds promotes ethical choices by avoiding businesses that conflict with Islamic values.

- Long-Term Focus: Many of these funds have a long-term approach, which can benefit investors looking to build wealth over time.

- Low Debt: These funds usually have minimal debt exposure, reducing the risk of heavy borrowing.

- Tax Benefits: In some places, Shariah-compliant investments can provide tax advantages to attract ethical investors.

#2 – Cons

- Less Liquidity: Shariah-compliant funds are often not easy to buy or sell quickly, leading to longer waiting times for transactions.

- Higher Costs: Managing and ensuring Shariah compliance can be more expensive in these funds, potentially reducing returns.

- Risk of Underperformance: Some Shariah-compliant funds may perform worse than conventional ones on certain measures, affecting returns.

- Long-Term Focus Only: These funds typically focus on the long term and may not suit those seeking short-term gains or easy access to their money.

- Higher Volatility: Due to limited investment options, Shariah-compliant funds may experience more ups and downs in value.

- Interpretation Differences: Interpretations of Shariah law can vary, leading to differences in how these funds are structured and potential confusion among investors.

Frequently Asked Questions (FAQs)

1.What are the risks of investing in Shariah-compliant funds?

Investing in Shariah-compliant funds carries risks. These funds might have fewer investors, making them less liquid. Additionally, they lack the same government oversight, potentially leading to higher volatility than conventional funds.

2.How do I choose a Shariah-compliant fund?

When choosing a Shariah-compliant fund, consider a few key factors. First, prioritize your investment goals and risk tolerance. Next, examine the fund’s track record and its associated costs. Lastly, ensure a reputable company manages the fund experienced in Shariah-compliant funds.

3.What is the future outlook for Shariah-compliant funds?

Shariah-compliant funds hold a promising future. Investor interest is growing as the global Islamic finance market expands rapidly. The demand for these funds will naturally increase alongside the growth of the Islamic finance industry.

4.Where can I buy Shariah-compliant funds?

Multiple distribution channels exist for buying Shariah-compliant products, such as banks, brokerage houses, and online investing platforms. Before making a purchase, it’s vital to ensure that the Shariah-compliant fund is registered with the necessary regulatory bodies.

Recommended Articles

This has been a guide to what are Shariah-Complaint Funds. Here, we explain the topic in detail, including its features, types, examples, and pros & cons. You can learn more about it from the following articles –