Part of our Investment Strategies guide

Factor Investing Definition

Factor investing refers to an investment strategy using factors to select securities. Investors can employ single or multi-factor investing strategies. Investors invest more in stocks exhibiting the selected factors to generate higher returns with limited additional risk.

The factor which drives the returns can be style factors like value or macroeconomic factors like GDP. This factor-based technique forms the core of beta strategies which increases return on investments and lowers the risk in the long term. An example of the factor-based model describing the stock returns is the Fama–French three-factor model explaining returns with the market, value, and size factors.

- Factor investing refers to a strategy that selects stocks based on a specific style or macroeconomic factors to enhance diversification and returns.

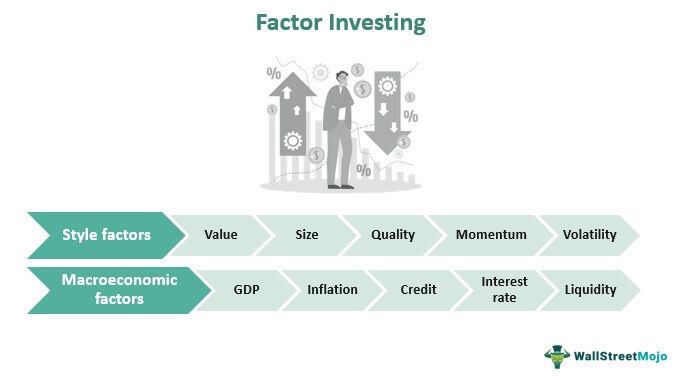

- The style factors are momentum, quality, value, size, and volatility. The macroeconomic factors are liquidity, credit, inflation, interest rates, GDP, etc.

- The concept started with or derived from the CAPM model, where the factor driving stock return is the market.

- Another pioneer model in the field is the Fama–French three-factor model explaining returns with the market, value, and size factors.

Factor Investing Explained

The factor investing method is derived from the Capital Asset Pricing Model (CAPM) developed in the early 1960s by William Sharpe, Jack Treynor, John Lintner, and Jan Mossin. According to the CAPM framework, systematic risk or market risk is the main factor determining the return on investment. Then evolved the Fama–French three-factor model explaining returns with three factors: market, value, and size factor. Later, researchers like Barr Rosenberg, Eugene Fama, and Kenneth French extended the CAPM to include certain systematic factors like value, small size, and momentum to explain the returns.

Deviating from the efficient market hypothesis, the following factors contributing to alpha generation can create a portfolio delivering excess returns overtime beating the market. Factors are categorized into style factors and macroeconomic factors. Popular style factors are value, size, quality, momentum, and volatility. The macroeconomic factors are GDP, inflation, credit, interest rate, and liquidity.

Factor Based Investing Styles

Let’s explain the style factors used in factor investing based asset allocation in brief:

Value

The value factor suggests and identifies the inexpensive stocks, that is, the stocks with a low market price compared to their fundamental value derived from the books of accounts. It is identified using techniques calculating book to price, earnings to price, book value, sales, earnings, cash earnings, net profit, dividends, cash flow, etc.

Size

Based on the market capitalization size, there are small-cap and large-cap stocks. Based on historical data, small-cap stocks possess growth potential, higher risk, and return The drawback is that small-cap stocks are not well-known, are riskier, and may incur a loss, but there is always room for growth over time, which fuels high returns. So size factor focus on obtaining excess returns of small entities. It is identified using the market capitalization values available.

Volatility

The low volatility concept sticks to selecting low volatility stocks, which means stocks with relatively stable returns compared to the broader market. According to the low volatility anomaly, the low volatility stocks give higher returns than highly volatile stocks based on historical data analysis. It is identified using techniques like standard deviation, downside standard deviation, a standard deviation of idiosyncratic returns, beta, etc.

Momentum

The momentum factor directs to pick stocks based on the past performance. If the stock exhibited strong performance in the past, it is expected to continue its success in the future. It is identified using techniques like relative returns and historical alpha.

Quality

The quality strategy selects the entities’ stocks with stable and strong financial performance, promising a regular return flow. Such companies are identified by determining ROE, earnings stability, dividend growth stability, balance sheet strength, financial leverage, [accounting policies, management strength, accruals, cash flows, etc. It is one of the common factor investing elements used.

Example

Through single-factor and multi-factor indexes, FTSE Russell Factor Indexes provide exposure to the performance of six well-known stock market factors (quality, size, value, momentum, volatility, and yield). These six elements are determinants of stock market performance.

Let’s consider two groups. One with factors, value, and small size for selecting stocks. Value stocks exhibit a higher value based on accounts books than stock market values. Then, small stocks have smaller capital and outstanding shares than other public listed companies. Another group contains growth and large stocks. Growth stocks are valued higher than their book values, and large stocks will have a significant market share.

Source: Forbes

From the above chart, if we compare value stocks to growth stocks (Russell 3000 value to Russell 3000 growth stocks) and small stocks to large company stocks (Russell 2000 small to Russell 1000 large stocks), it reveals the following:

In the aughts (2000-2009):

- Value stocks and small stocks performed well

- Growth and large stocks showcased a poor performance

In the most recent decade, teens (2010-2019):

- Growth stock outperforms value stock

- Large outperformed small stocks

Frequently Asked Questions (FAQs)

What are the 5 factors in factor investing?

Factors used to select securities are categorized into two types: style factors and macroeconomic factors. Popular style factors are value, size, quality, momentum, and volatility. The common macroeconomic factors are GDP, inflation, credit, interest rate, and liquidity.

What is momentum factor investing?

The stocks will be selected based on the successful past performance when the momentum factor is used. They are anticipated to maintain past or recent price trends in the future. However, they face the risk of trend reversals. The technique used to identify such stocks are relative returns and historical alpha.

What is factor investing ETF?

While designing or creating a factor ETF, the assets selected can be based on predetermined factors. For instance, a size factor ETF will tend towards smaller firms with high growth potential. Whereas a momentum factor ETF follows stocks showing an uptrend, and a value factor ETF prefers undervalued stocks.

Recommended Articles

This has been a Guide to Factor Investing & its Definition. We explain factors like momentum, factor investing-based asset allocation, and ETFs. You can learn more about accounting from the following articles –