What Is Drawing Account?

A drawing account is a contra owner’s equity account used to record the withdrawals of cash or other assets made by an owner from the enterprise for its personal use during a fiscal year. It is temporary and closed by transferring the balance to an owner’s equity account at the end of the fiscal year.

The word drawings refer to a withdrawal of cash or other assets from the proprietorship/partnership business by the Owner/Promoter of the business/enterprise for personal use. Any such withdrawals made by the owner lead to a reduction in the owner’s equity invested in the Enterprise. Therefore, it is crucial to record such withdrawals (made by the owner) over the year in the balance sheet of the enterprise as a reduction in owner’s equity and assets.

Drawing Account Explained

A Drawing Account is an account in the books of the business which is used to record the transactions involving the withdrawal of something by the owner of the business who has his capital invested in the business, generally proprietorship or partnership business. Drawings can be made in the form of cash which is an asset for every business. Even inventory, machinery or equipment, if taken out of the business, will come under withdrawal. Therefore, it brings the value of owner’s equity down.

- The owner’s drawing account a contra owner’s equity account to an associated owner’s equity account.

- It is used to record the transaction of an owner withdrawing cash or other assets from its proprietorship enterprise for personal use.

- Drawing account entry is temporary in nature, which is closed at the end of the fiscal year and starts with zero balance to record the owner’s withdrawals in the next fiscal year.

- It is closed at the end of the fiscal year by transferring the balance from the drawing account to the owners’ equity capital account.

- It’s useful in keeping track of distributions made to owners in a partnership business, thus helping avoid any disputes between business partners.

However, it is important that every business, be it sole proprietor, partnership or any other form, should be well informed about the rules and regulations of withdrawal in the form of asset of cash. If this is not clear, then it may cause legal issues. Since the fund is going out due to withdrawal, it is necessary to record the transactions correctly and in a systematic manner in the owner’s drawing account so that there are no financial issues and lack of liquidity in the business later on. Profitability should not be affected by this in any way, because businesses cannot sustain if cash flow is restricted.

Nature Of Drawing Account

Let us study the nature of this type of account in details.

- Tracking capital – This account’s primary purpose is to keep a tab on the amount of money that the members may withdraw for personal use from the entity. This is crucial because over withdrawal will affect cash flow and liquidity in a negative way and result in problems in meeting not only the day-to-day expenses, but also block the funds needed for growth and expansion.

- Not a permanent account – It is not permanent in the sense that it is started freshly every year, in order to track the money withdrawn by the partners from the business, therefore making drawing account entry a temporary account. After accounting for the entire year, it is credited in the general ledger. Whatever balance remains it is transferred to the capital or in the balance sheet, the owner’s equity side.

- Not treated as an expense – Even though the account exibits a reduction in the funds that are available within the entity, it is not treated as an expense incurred in it. It simply depicts the amount that has been taken out for personal use by the members, which is a fall in owner’s equity.

- Not for big corporations– This kind of account is not meant for big corporations. This is because, in their case, the identity of the business and owners are separate. So, a separate account is not needed. However, for small businesses, this partners drawing account helps in separating the business from the personal usage of money by owners.

Thus, the above points clearly specify the characteristics of this form of account and it is important to have a good understanding of the same so that the related transactions can be easily identified and recorded correctly.

Example

To understand the concept of the partners drawing account and its utility, let’s start with a practical example of a transaction in a sole proprietorship business. Assuming the owner (Mr. ABC) started the proprietorship business (XYZ Enterprises) with an investment/equity capital of $1000.

The Balance sheet of XYZ Enterprises as on 1st April 2017 is as below:

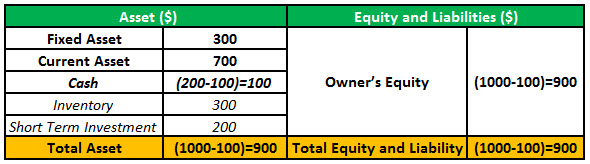

Suppose Mr. ABC takes out $100 from the business for personal use during the financial year FY18. The impact of the above transaction on the Balance sheet will be a reduction in the cash balance and the owner’s equity capital by $100. Therefore, the Balance Sheet after the transaction will look like this:

The above demonstration is one example of a transaction; however, in proprietorship/partnership, the owners generally may do multiple transactions during a fiscal year for personal use. There is a mechanism to record such transactions and adjust the Enterprise’s drawing account in balance sheet for such transactions where the Owner uses business resources (cash or goods) for personal use.

Journal Entry

Extending our discussion from the initial section of the article where we have taken the example of Mr. ABC (Owner) making a withdrawal of $100 from its proprietorship business (XYZ Enterprises) for personal use. This transaction will lead to a reduction in the owners’ equity capital of the XYZ Enterprises and a reduction in the Cash Balance of the enterprise.

Since this account is set up as a contra owner’s equity account to record this and similar other transactions of this nature, the following transactions will be recorded in the drawing account. Its Journal entry for the above cash transaction by the owner will be recorded with a debit in the owner’s and as a credit in the cash account. The entries for the above transactions will be as below:

Since it is a temporary account, it is closed at the end of the financial year. At the end of the financial year, the drawing account balance will be transferred to the owner’s capital account, thereby reducing the owner’s equity account by $100.

Therefore, at the end of the Year owner’s equity balance will be as below:

Owner’s equity capital= (1000) +Drawing account balance = (1000) +(-100) =$900

Also, the Cash account on the asset side of the balance sheet at the end of financial year FY18 will reduce by $100, and a closing balance will be as below to show the drawing account in balance sheet:

Cash= (200-Cash withdrawals) = (200-100) =$100

Therefore, the balance sheet position of XYZ Enterprises at the end of the fiscal year FY18 to include the impact of an above-discussed transaction will be as below.

Recommended Articles

This has been a guide to what is Drawing Account. We explain it with journal entries, along with example and nature of the account. You may also take a look at some useful articles:-