Part of our General Ledger guide

Suspense Account Meaning

A suspense account is the general ledger account that the company uses for recording transactions temporarily. When recording those transactions, the accountant may be unsure of the type of account most appropriate to record those transactions. It helps companies keep their accounting books in an organized manner.

It helps ensure that all the transactions are recorded under the correct heads. It improves the quality of book-keeping and proper representation of all the transactions. It is like a temporary shelf where all the “miscellaneous” items can be parked until their actual nature can be ascertained. When we record uncertain transactions in permanent accounts, it might create balancing issues.

Suspense Account Explained

A suspense account is a temporary account where entries with discrepancies and doubtful factors are parked. Toward the end of the accounting period, all discrepancies are sorted and accounted for to their permanent entities.

Sometimes, accounting teams don’t have all the necessary information for a particular transaction. Regardless of that, they need to record every transaction to keep their ledger books up to date, and this is where the suspense account comes in handy, as they are not sure where to record general ledger entries.

- As the name suggests, all the transactions recorded in this account are “suspense” for the accountant. Hence, accountants need to gather more information about the nature of these transactions to move them into their correct accounts.

- It is vital to understand that all the transactions are temporarily recorded in this account. Although there is no standard amount of time set by regulatory authorities to clear this account. Ultimately the accounting team must move all the transactions into their correct accounts as soon as they can ascertain their exact nature.

- This account is not meant to manipulate the books of accounts. Instead, it is used to give some leeway to the accountant to find the true nature of some transactions to make the ledger books more robust.

- Depending on the nature of the transaction, it can be either an asset or a liability. If they cannot ascertain the true nature of a particular investment, then this account will be classified as a current account. In similar ways, it could also be used to park an “unclassified” liability.

Examples

Let us understand how suspense account entries work and how it helps accounting teams with the help of a couple of examples.

Example #1

An accountant was asked to record a few journal entries written by the finance head of a large corporation. There was one transaction whose nature could not be ascertained at recording. The accountant recorded the “unclassified” amount in the general ledger suspense account to complete the assignment by the deadline.

He will move the amount from the Suspense account to the appropriate account as soon as he gets more information about the nature of the transaction. Hence this account helped him to keep the transaction in the books of accounts and, at the same time, deter him from putting it under the wrong category.

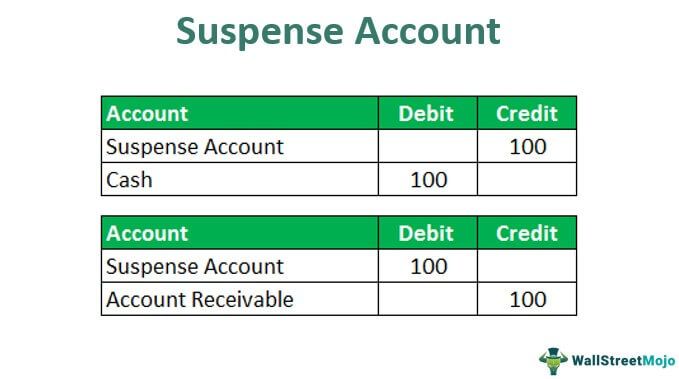

Example #2

When you receive cash of $100 from the client but are not sure about the transaction against which he made this payment, then you can 1st pass this entry, and once you can determine that then, you can reverse this transaction in the following manner-

Purpose

A suspense account format is used in different scenarios for different companies and their specific needs. Let us understand how it is used in real and practical scenarios through the discussion below.

#1 – When preparing a trial balance

A trial balance is the closing balance of an account that we calculate at the end of the accounting period. When the two sides of the trial balance don’t match, we hold the difference in a suspense account until we correct it. If the debits in the trial balance are larger than credits, we record the difference as a credit. If the credits are larger than debits, we record the difference as a debit. Then, we close the account after making the necessary adjustments so that it’s no longer part of the trial balance.

#2 – Uncertainty regarding the payment maker

When we cannot match the payment from a particular client with the account receivables balance, we can park that payment in the suspense account to match the client’s outstanding dues with the payment and cross-verify it with the client.

#3 – Uncertainty regarding the classification of the transaction

When the business is unsure about the account in which they need to park a particular transaction, it is best to put the transaction in a suspense account and consult with your accountant before making any decision.

Recommended Articles

This article has been a guide to Suspense Account meaning. Here we explain its examples, purpose, entries and calculations in detail. You can learn more about accounting with the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.