Part of our General Ledger guide

What is T Account?

T Account is a visual presentation of accounting journal entries that are recorded by the company in its general ledger account in such a way that it resembles the shape of the alphabet ‘T’ and depicts credit balances graphically on the right side of the account and debit balances on the left side of the account.

A T account ledger is an informal way of addressing a double-entry bookkeeping system. On the top, the name of the ledger is mentioned, the left side is for debit entries, and the right side is for credit entries within the ledger. It is essentially a visual or graphical representation of the company’s accounts which can be used to present, scrutinize, or review.

T Accounts Explained

In a T account, all business transactions impact at least two of the company’s accounts in such a way that if one account gets a debit entry, then another account will get a credit entry of the identical amount to close each transaction that occurs. For different account types, a debit and a credit may increase or decrease the account value.

- For an asset account, a debit entry on the left side increases to the account, while a credit entry on the right side results in a decrease to the account. It implies that a business that receives cash will debit the asset account, while a cash pay-out will credit the account.

- On the other hand, for a liability account or a shareholders’ equity, a debit entry on the left side decreases the account. In contrast, a credit entry on the right side increases the account.

- In a revenue/gain account, a debit entry translates into a decrease in the account, and a credit entry translates into an increase.

- On the other hand, in an expense/loss account, a debit entry translates into an increase in the account, and a credit entry translates into a decrease.

Putting all the accounts together in a tabular form depicting the impact on each account type:

| Account Type | Debit | Credit |

|---|---|---|

| Asset | Increase | Decrease |

| Liability | Decrease | Increase |

| Shareholder’s Equity | Decrease | Increase |

| Revenue/Gain | Decrease | Increase |

| Expense/Loss | Increase | Decrease |

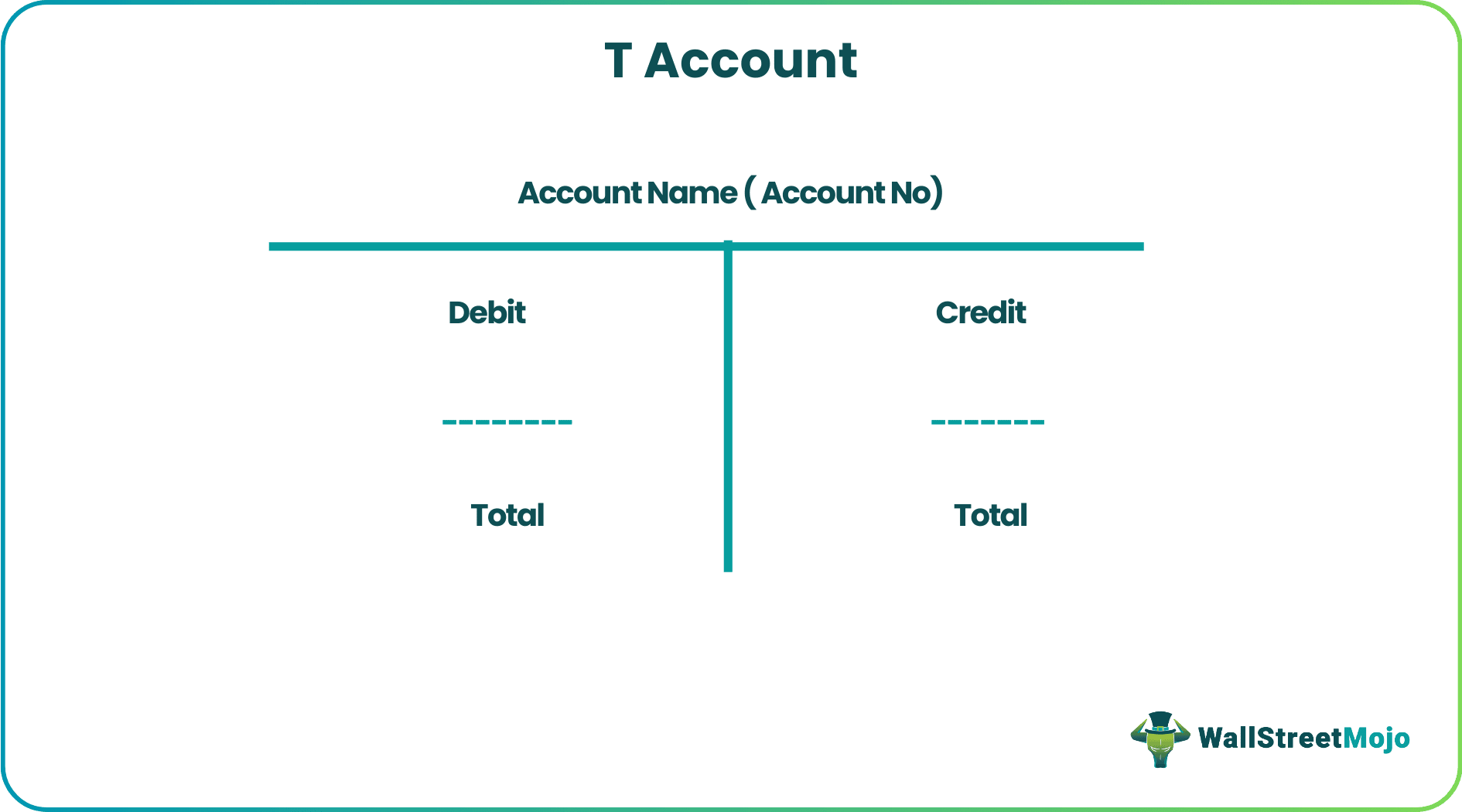

Format

Let us understand the format of a T account ledger and how it is designed in a way where it gives the individual reviewing it an ease of locating entries.

The name of the account is written above the “T” along with the account number (if available), while the total balance for each “T” account is written at the bottom of the account. The format of the T Account is given below –

- The shape supports the ease of accounting so that all additions and subtractions to the account can be tracked and represented easily.

- It is a useful facet of the double entry accounting method as it displays how one side of an accounting transaction impacts another account, which, in a way, helps simplify more complex transactions.

- A T account is especially useful in the case of a compilation of challenging and complex accounting transactions where the accountant intends to track how the transaction impacts all other parts of the financial statements.

- It can be helpful in the avoidance of erroneous entries in the accounting system.

Examples

Let us take an example of T accounts with the following two transactions-

Example #1

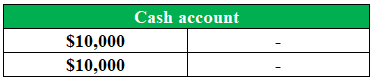

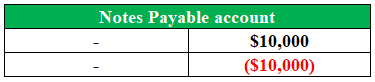

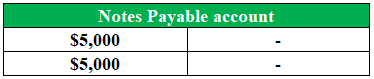

On January 01, 2018, a company ABC Ltd borrowed $10,000 from a bank:

This transaction will increase ABC’s Cash account by $10,000, and its liability of the Notes Payable account will also increase by $10,000. The T account balance must be debited to increase the Cash account, since it is an asset account. On the other hand, t the account must be credited o increase ABC’s Notes Payable account, since it is a liability account.

Example #2

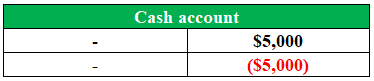

On February 01, 2018, ABC Ltd repaid a bank loan of $5,000:

This transaction will decrease ABC’s Cash account by $5,000, and its liability Notes Payable account will also decrease by $5,000. To reduce the Cash account, the account must be credited since it is an asset account. On the other hand, the Notes Payable account is expected to be debited since it is a liability account.

The below table presents the general journal entries for the two transactions mentioned in the T accounts above.

Related Terminologies

Let us understand the concept in depth through understanding the related terminologies of a T account balance through the discussion below.

#1 – General Ledger

A general ledger is a formal representation of a company’s financial statements where the debit account and credit account records are validated with a trial balance. A general ledger offers comprehensive documentation of all financial transactions of the company over a certain period. A general ledger is the repository of all account-related information required to prepare a financial statement. The typical accounts include accounts of assets, liabilities, shareholders’ equity, revenues, and expenses, etc.

#2 – Double Entry Accounting

The double-entry accounting method is a fundamental concept that drives contemporary bookkeeping and accounting techniques. It is built on the fundamental premise that every financial transaction has an equal and opposite impact on at least two different accounts. The accounting equation’s underlying concept is Total Assets = Total Liabilities + Shareholders’ Equity.

Recommended Articles

This article has been a guide to what is T-Account. Here we explain its examples, format, and related terminologies in detailed manner. You may also find some useful accounting articles below –

Recommended Articles

Continue with these closely related articles from the same guide.