Part of our General Ledger guide

What Is Record To Report (R2R)?

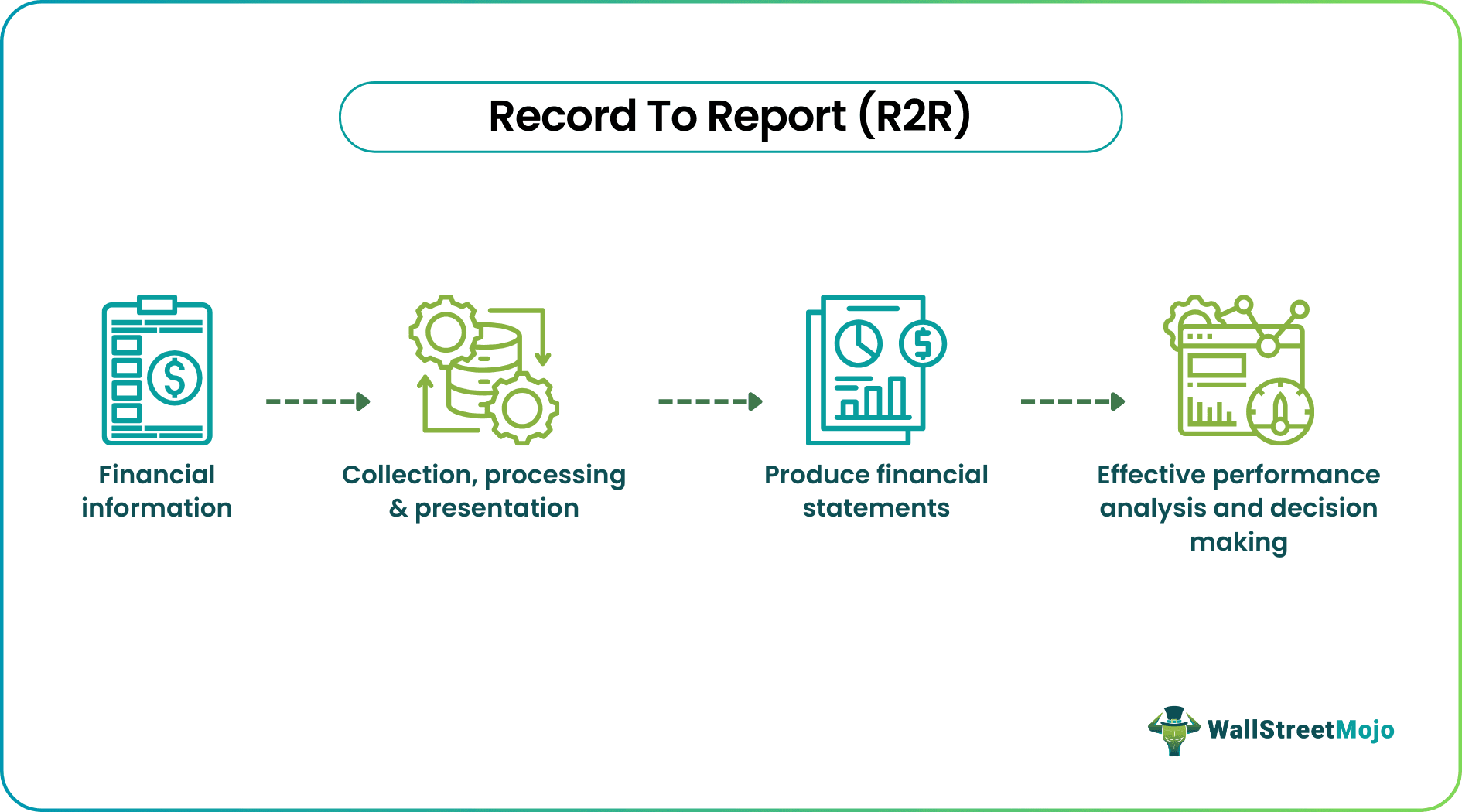

Record to report (R2R) is a process used by finance and accounting professionals with the intent to gather, analyze, and present financial data. The process aids in providing correct, relevant, and timely information that contributes to strategic feedback in finance and operations.

Feedback helps in analyzing the management’s efficiency through its acquired experiences. The information obtained through R2R helps with the performance analysis. The progress achieved by the business is assessed and compared with the overall market performance. It allows stakeholders and senior management to see how closely their expectations match reality.

- Record to report is a management process that provides financial, operational, and strategic feedback.

- The process includes gathering, transforming, and disseminating relevant, timely, and accurate information to relevant parties.

- It provides feedback on the status of overall goals and the market’s actual performance. Firms can gain a competitive edge and become competent, agile, and coordinated through superior management procedures.

- The reporting, consolidation, closing, and processing cycles are the steps involved in the R2R process.

Record To Report Explained

Record to report is a management process that provides financial, operational, and strategic feedback. The record part entails recording an organization’s financial transactions. On the other hand, the report entails producing financial records, such as balance sheets, profit and loss statements, and budget reports. It is done to understand the performance of a business. The process includes gathering, transforming, and disseminating relevant, timely, and accurate information to relevant parties. They include stakeholder groups both inside and outside the organization and senior management. This helps them be aware of how much their expectations have been realized.

The R2R works out two things:

- The management excellence framework offers feedback to every other management process. However, this stage comes last in the framework because a tangible business result can only be achieved by pushing strategies to execution.

- It manages the management process. It determines whether or not they are efficient and whether or not the costs exceed a certain percentage. It is thus a key performance indicator (KPI) in measuring the cost of management processes involved as part of overall business costs. It assesses how these processes support managers to keep them in touch with reality. This is done through forecast accuracy, which is a quality indicator. Other indicators include speed, “time to report, ” time to close,” and “time to respond,” among others. “Time to report” is the amount of time required to combine the data from various business systems to report it to the outside world.

Process Steps

The record to report steps involves the following:

#1 The Processing Cycle

The revenues, purchases, and expenditures for business units across the corporation are recorded during the recording process. The organization’s financial transactions are recorded during this phase, which involves processing the data and transactions and compiling and indexing them to ensure accuracy. They collect all the information needed to produce financial statements and management reports from various sources, such as journal entries, general accounting activities, and procure-to-pay cycles. It is the primary source of the vast majority of the data needed for the Record to Report process. As a result, data integrity is essential since low-quality data results in rework, manual intervention, and general inefficiencies. These slow down the overall process.

#2 Close Cycle

The close cycle is the period between posting transactions to the general ledger and the financial reporting systems locking down the general ledger. The finance professionals transfer balances from temporary accounts to permanent accounts upon closing. Temporary accounts look at a specific period and may contain income, expenses, or dividends paid. Meanwhile, the permanent accounts display the company’s long-term financial performance or position. The organization prepares for its upcoming accounting period by balancing temporary accounts to zero. After recording and processing financial data, finance and accounting professionals lock the general ledger at the end of the accounting period. The organization’s reporting needs will determine whether this time frame is monthly, quarterly, or yearly.

#3 Consolidation Cycle

This stage, often called the reconciliation and validation stage, entails reviewing the recorded transactions and classifying them into relevant groups. This stage enables them to group related data and ensure they have everything needed to create reports for stakeholders. This phase includes elimination, intercompany balance reconciliation, and the data generation needed to create financial statements.

#4 Reporting Cycle

It is the official procedure for obtaining, integrating, analyzing, and disseminating data. Financial reports regarding the organization are produced by finance and accounting specialists. These experts better understand the company after checking the data for completeness and accuracy. Then, they produce various reports, including profit and loss statements, balance sheets, income statements, and other compliance, performance, or profitability records. The senior management, business unit managers, and the organization’s leaders get these reports from the team. These reports might also be distributed to other parties who need to evaluate the organization’s financial operations, including investors or regulatory organizations. They can create forecasts for the future and implement strategic changes to enhance operations or financial performance using the information from these reports.

Examples

Let’s look into a few examples of record to report:

Example #1

Suppose Dan recently opened a “Jason’s R2R Services” business that provides R2R services to companies. He desired to advertise some of the services he provides, and the brochure included the following:

- Instructions on creating and managing accounting records, including sales invoices, statements, payments, etc.

- Keeping track of monthly, quarterly, or yearly accounts.

- Creating a balance sheet and annual profit and loss accounts.

- Forecasting cash flows and budgeting.

- Keeping all paperwork and financial records updated.

- Accounts receivable and accounts payable management.

- Keeping track of management accounting information.

- Reconciling financial statements regularly.

Example #2

Suppose ABC Inc. embraces cloud-enabled technology to streamline its record to report (R2R) process. This has facilitated the digitization and automation of various aspects of finance departments’ monthly, quarterly, and annual record to report (R2R) process. This effort has primarily focused on automating the early stages of the R2R period close, leading to quicker derivation of trial balances. They also focus on the need for a digitized process where general ledger or consolidation tool outputs seamlessly combine with other content, automatically populating reports that can be collaboratively approved and published.

Best Practices

Some of the best practices that can be useful for the optimization of the record to report process are:

- Complying with local and international accounting standards helps the company stay focused and on track. This prevents error through deviation and makes rectification and correction easier.

- Creating relevant strategic, financial, and operational performance indicators for each stage of the strategy-to-success framework using data.

- Choosing the optimal presentation method for the information based on the type of performance indicator, the preferences of the users, and the security requirements.

- Present findings to relevant internal and external stakeholders in a complete, accurate, and timely manner.

- Moderating stakeholder communication, etc.

Frequently Asked Questions (FAQs)

1. What is a record to report cycle?

The record to report cycle is the duration to complete an R2R process. It aggregates existing collection methods to display performance reports prepared for management. The cycle involves various steps, such as recording the transactions, processing the transactions, closing the cycle, consolidating the data, and reporting.

2. Why is a record to report important?

It presents a review of the status of overall goals and actual performance in relation to the market, which strategists require. R2R reveals anomalies and performance variation analysis, another business planning requirement. Firms can gain a competitive edge and become competent, agile, and coordinated through superior management procedures.

3. What is an R2R analyst?

The record to report (R2R) accounting analyst provides end-to-end accounting services. These services are provided in accordance with international standards. The procedures adopted will also comply with the usual standard accounting procedures. This ensures that reality is portrayed and necessary corrective actions can be taken.

Recommended Articles

This has been a guide to what is Record To Report (R2R). Here, we explain the topic in detail, including its steps examples, and best practices. You can learn more about financing from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.