What Is Calculate Quick Ratio?

The quick Ratio Formula is one of the most important Liquidity Ratios for determining the company’s ability to pay off its current liabilities in the short term and is calculated as the ratio of cash and cash equivalents, marketable securities, and accounts receivables to Current Liabilities. The quick ratio formula finance determines how fast a company can repay its current liabilities.

It determines how a company can repay its current liabilities without having to source more finance or sell inventory. A higher ratio would depict higher liquidity for the company. Meaning, they can repay their immediate liabilities without too much hassle. It is considered to be a more conservative approach in comparison to the current ratio.

Key Takeaways

- The quick ratio formula is a vital liquidity ratio that assesses a company’s ability to meet short-term debts. It is calculated by dividing the sum of cash, cash equivalents, marketable securities, and accounts receivables by current liabilities.

- The quick ratio provides a more accurate evaluation of short-term liquidity compared to the current ratio. It helps management ensure sufficient quick assets are available to settle short-term liabilities on the balance sheet.

- A well-managed short-term financial position is reflected in this ratio, instilling confidence in investors and creditors.

Explanation

Quick ratio formula is used to determine how a company is equipped to meet their immediate payments or current liabilities without having to sell more from their inventory or secure additional financing.

The Quick Ratio is a more stringent measure of short-term liquidity than the Current Ratio. Quick Assets are the ones that can convert to cash in the short term or 90 days. The important difference between the Current Ratio formula and the Acid Test Ratio formula is that we exclude Inventory & Prepaid Expenses as a part of Current Assets in the Quick Ratio formula.

Inventory is excluded because it is assumed that the stock held by the company may not be realized immediately. Such a situation will make liquidating the inventory more trickier and more time-consuming. The inventory could be in the form of Raw materials or W-I-P.

The ratio of 1 or more indicates that the company can pay off its current liabilities with the help of Quick Assets and without needing to sell its long-term assets and has sound financial health. Care must be exercised in placing too much reliance on acid test ratio without further investigating; E.g., Seasonal businesses, which seek to stabilize production, might have a weak Quick ratio during its period of slack sales, but a higher one in case of its peak business season. Such situations may prove tricky to know the company’s actual financial position.

Quick Ratio Explained in Video

Formula

Let us understand the formula used for quick ratio formula accounting before we dwell deeper into the concept.

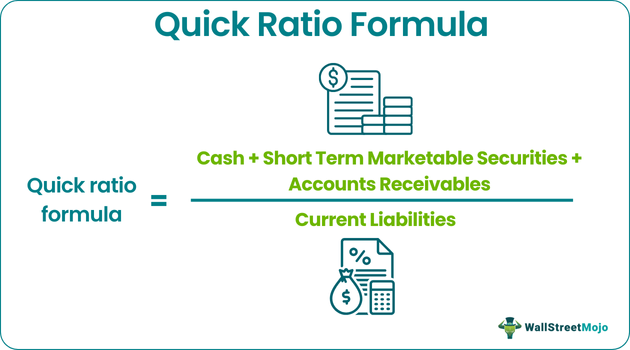

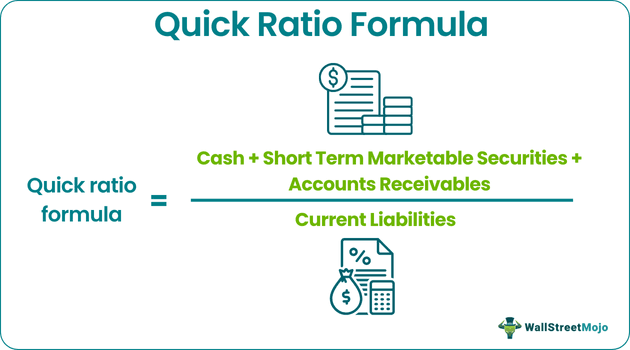

Quick Ratio = (Cash + Short Term Marketable Securities + Accounts Receivables) /Current Liabilities

OR

In case the company is not giving a breakup of Quick Assets, then:

Examples

Let us understand the quick ratio financing with the help of a few examples. There practical examples will help us understand the concept in depth.

Example #2

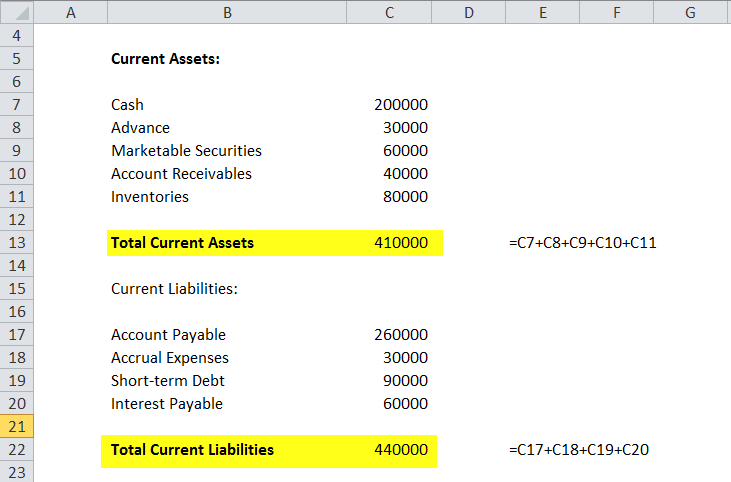

Masters Co. Ltd has the following details:

Current Assets:

- Cash = $200,000

- Advance = $30,000

- Marketable Securities = $60,000

- Account Receivables = $40,000

- Inventories = $80,000

Total Current Assets = $410,000

Current Liabilities:

- Account Payable = $260,000,

- Accrual Expenses = $30,000,

- Short-term Debt = $90,000,

- Interest Payable = $60,000.

Total Current Liabilities = $440,000.

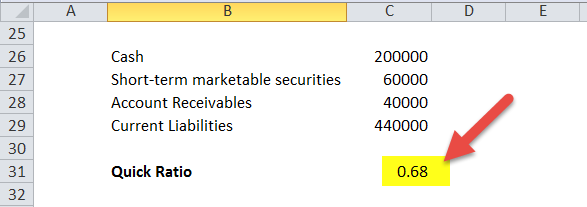

Previous years quick ratio was 1.4 and the industry average is 1.7

Calculation of acid test ratio formula:

Quick ratio formula = (Cash + Short-term marketable securities + A/c’s Receivable) / Current Liabilities

= ($200,000 + $60,000 + $40,000) / ($440,000)

= ($300,000) / ($440,000)

= 0.68

Example #2

As noted from the below graph, the Cash Ratio of Microsoft is a low 0.110x; however, its quick ratio is a massive 2.216x.

Excel Template

Using an Excel sheet can be easier in a lot of cases. Therefore, let us understand how to carry out quick ratio formula finance through the template below.

One needs to provide the two inputs of Total Current Assets and Total Current Liabilities.

Calculation of acid test ratio

Acid test ratio = (Cash + Short-term marketable securities + A/c’s Receivable) / Current Liabilities

Significance

Let us understand the significance of quick ratio formula accounting through the explanation below.

- Keeping track of the Quick ratio helps the management determine whether they are maintaining optimum levels of Quick assets to take care of its short-term liabilities in their balance sheets.

- It showcases a well-functioning short-term financial cycle of a company.

- It improves the company’s credibility with the investors by gaining and maintaining their trust in the value of their investments.

- Also, the company’s creditors know that their payments will be made on time.

Frequently Asked Questions (FAQs)

What is the importance of the quick ratio formula?

The quick ratio formula, also known as the acid-test ratio, is essential for assessing a company’s short-term liquidity and ability to meet immediate financial obligations. It focuses on quick assets, such as cash, cash equivalents, marketable securities, and accounts receivable, to provide a more stringent measure of a company’s ability to pay off current liabilities without relying on inventory sales.

What are the limitations of the quick ratio formula?

While the quick ratio is valuable, it has limitations. Excluding inventory from quick assets may not accurately represent a company’s liquidity if it relies heavily on inventory sales. Additionally, the formula may not consider the timing of accounts receivable collections, potentially affecting the interpretation of a company’s liquidity position.

What is the difference between the current ratio and the quick ratio?

The current ratio and quick ratio are both liquidity ratios but differ in the components they consider. The current ratio includes all current assets, including inventory, in the numerator, while the quick ratio only includes quick assets (cash, cash equivalents, marketable securities, and accounts receivable). The current ratio provides a broader view of a company’s short-term liquidity, while the quick ratio offers a more conservative measure that excludes inventory.

Recommended Articles

This article has been a guide to what is Quick Ratio Formula. Here we explain its examples, and provided a downloadable Excel template, and a calculator. You may also have a look at these articles below to learn more about Financial Analysis –