What Are Quick Assets?

Quick Assets refer to the Assets which are liquid and can be easily converted into Cash by liquidating the same in the market like FDs, Liquid Funds, marketable securities, Bank Balances, etc., and form an essential component in the financial ratio analysis of the company to showcase strong working capital.

You are free to use this image on your website, templates etc, Image creditPlease provide us with an attribution link[/wsm-img-crd-tooltip]

These assets can be converted to cash quickly, and there is no substantial loss of value while converting an asset into cash. Quickly, it means that assets can be converted to cash in a year or less. Companies manage such assets prudently to remain solvent and liquid.

- Quick assets, such as FDs and bank balances, are highly liquid assets that can be easily converted into cash through market liquidation.

- They play a critical role in a company’s financial ratio analysis, showcasing its substantial working capital.

- Quick assets can be swiftly converted into cash with minimal loss of value, typically within a year or less, highlighting their high liquidity and ease of conversion.

- A higher quick ratio is favorable for a company. It signals that it possesses more liquid assets than its current liabilities, indicating a stronger ability to meet short-term obligations.

Quick Assets Formula

The formula is straightforward, and it can be calculated by subtracting inventory from the current assets.

Quick Assets Formula = Current Assets – Inventory

Quick Assets Explained in Video

List of Quick Assets

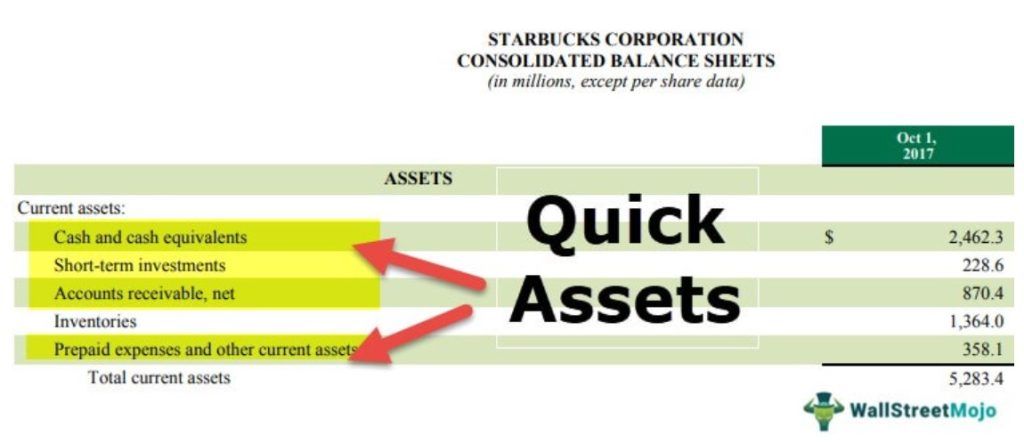

source: Starbucks SEC Filings

These are found on the balance sheet of the Company, and it is the sum of the following list of quick assets:

- Cash

- Marketable securities

- Accounts receivable

- Prepaid expenses and taxes

- Short-term investments

#1 – Cash

Cash includes the amount kept by the Company in bank accounts or any other interest-bearing accounts like FDs, RDs, etc. Cash and Cash Equivalents in Starbucks were at $2,462.3 in FY2017 and $2,128.8 million in FY2016.

#2 – Marketable Securities

There are liquid securities openly traded in the market. Such securities can be easily sold at the quoted price in the market and converted to cash.

#3 – Accounts receivables

Account receivables are the amount the Company is still to receive from the goods and services they have provided to its customers. The Company has already given the services, but they are yet to receive the payment. Hence the Company files it as an asset in the accounts book. Account receivables should be determined properly, and only those amounts should be added if the receivables can be collected within one year or less. Uncollectible, stale receivables, or long-term receivables generally for Companies in the construction business should not be added for calculating quick assets.

Accounts Receivables in Starbucks increased to $870.4 million in FY2017 compared to $768.8 million in FY2016.

#4 – Prepaid expenses

Prepaid expenses are the expenses the Company has already paid but it is yet to receive the service. Such services should be consumed within one year to be added to the calculation. Prepaid expenses could be rent expenses.

Prepaid expenses and other current assets in Starbucks were at $358.1 million in FY2016 and $347.4 million in FY2016.

#5 – Short-term investments

The company’s short-term investments are investments that are expected to convert into cash within one year. These generally consist of stocks, bonds, and other securities, which can be liquidated quickly and as and when required. Short-Term Investments in Starbucks were $228.6 million in FY2017 and $134.4 million in FY2016.

Inventory is not added to the calculation because inventories can take a longer period to be sold and then converted to cash. Inventories do not have a stipulated period; hence, we remove them while calculating the accounts receivables.

Quick Assets Examples

Examples #1

A Company XYZ has $ 5000 as cash, $ 10000 as marketable securities, and $ 15000 as accounts receivables, which will be received in 2 months. What are the total liquid assets of the Company?

- Quick assets Formula = Cash + Marketable Securities + Accounts Receivables = 5000 + 10000 + 15000 = $ 30,000

Examples #2

A Company MNP has $ 50000 of current assets with $ 30000 as inventories. What is the value of the quick assets on the Company’s balance sheet?

- QA = Current assets – Inventories

- QA = 50000 – 30000 = $ 20000

Analysts use these to measure a company’s liquidity of a Company in the short term. Based on its line of operations, the Company keeps some of its assets in the form of cash, marketable securities, and other asset forms to maintain its liquidity needs in the short term. A vast amount of such assets than required in the short term may imply the Company is not using its resources effectively. Small QAs or smaller than the liabilities arising in the short term means that the Company may require additional cash to meet its demand.

How do Financial Analysts use it?

To compare the two Companies – financial analysts use the quick assets ratio or acid test ratio. It is called the acid test ratio concerning an acid test done by the gold miners in ancient times. The metal mined from the mines was put to an acid test, whereby if it failed from eroding from the acid, it is a base metal and not gold. If the metal passed the test, it was considered gold.

Thus, the quick ratio is considered an acid test in finance, where it tests the Company’s ability to convert its assets into cash and pay off its current liabilities.

The quick ratio is calculated by dividing it by current liabilities.

Quick Assets ratio = (Cash + Cash equivalents + Short-term investments + Current receivables + prepaid expenses)/ Current liabilities

Most Companies use long-term assets to generate revenue; hence, it would not be prudent for the Company to sell off long-term assets to meet current liabilities. Thus, a quick ratio puts the Company’s finances to test its ability to meet its current liabilities.

source: ycharts

As compared to its Peers, Colgate has a very healthy quick ratio. While Unilever’s Quick Ratio has been declining for the past 5-6 years, we also note that the P&G Quick ratio is much lower than Colgate’s.

Quick Assets Ratio Example

Let us consider the following example to measure quick ratio:

The balance sheet of a Company XYZ is as follows:

- Cash: $ 10000

- Accounts receivables: $ 12000

- Inventory: $ 50000

- Marketable securities: $ 32000

- Prepaid Expenses: $ 3000

- Current liabilities: $ 40000

Thus, quick ratio = (Cash + Accounts receivables + Marketable securities + Prepaid Expenses)/ Current liabilities

- quick ratio = (10000 + 12000 + 32000 + 3000)/40000

- quick ratio = 57000/40000 = 1.42

Higher the quick ratio is more favorable for the Company as it shows the Company has more liquid assets than the current liabilities. A ratio of 1 indicates the Company has just sufficient assets to meet the current liabilities. In contrast, the ratio of less than 1 indicates the Company may face liquidity concerns in the near term.

Conclusion

The quick asset is the number of assets on the Company’s balance sheet, which can be quickly converted into cash without significant losses. Companies try to maintain an appropriate amount of liquid assets considering the nature of their businesses and volatility in the sector. The quick asset ratio or the acid test ratio is significant for the Company to remain liquid and solvent. Analysts and business managers maintain and monitor the ratio to meet the Company’s obligations and provide the turn to shareholders/investors.

Frequently Asked Questions (FAQs)

1. What is quick asset vs. quick liabilities?

Quick assets are a company’s most liquid assets that can be easily converted into cash within a short period, typically including cash, marketable securities, and accounts receivable. On the other hand, quick liabilities are a company’s current obligations or liabilities that are expected to be settled within a short period, usually within one year, and are typically used in calculating financial ratios such as the quick or acid-test ratio to assess a company’s short-term liquidity.

2. Is other current assets quick asset?

Other current assets may or may not be considered quick assets, depending on their liquidity. Quick assets are typically limited to cash, marketable securities, and accounts receivable, which are expected to be converted into cash quickly.

3. Is notes receivable a quick asset?

Notes receivable may or may not be considered a quick asset, depending on their liquidity. For example, if notes receivable are expected to be collected within one year and can be easily converted into cash, they may be considered as part of the quick assets. However, if notes receivable have longer maturity periods or are not easily converted into cash, they may not be considered quick assets.

Recommended Articles

This article has been a guide to what Quick Assets are. Here we provide its formula to calculate quick assets along with examples and a list of items included. We also discuss how the Quick Assets Ratio is used by Financial Analysts. You may learn more about Basics of Accounting from the following articles –