What Is Real Interest Rate?

Real interest rates are the interest rates derived after considering the impact of inflation, which is a means of obtaining inflation-adjusted returns of various deposits, loans, and advances. Hence, it reflects the real cost of funds to the borrower; however not generally used in deriving cost.

Thus, the effect of inflation is removed, and the remaining value shows the actual cost of borrowing for the borrower and the actual yield for the lender. Is shows the compensation in case of a borrower’s default or any changes in the rules and regulations.

- Real interest rates are those that have been calculated after considering the effects of inflation. These rates can be used to calculate the returns on various deposits, loans, and advances adjusted for inflation.

- Inflation is taken into account by the real interest rate. It offers a way to determine the inflation-adjusted returns on even the most basic deposits, bond investments, or recurring loans.

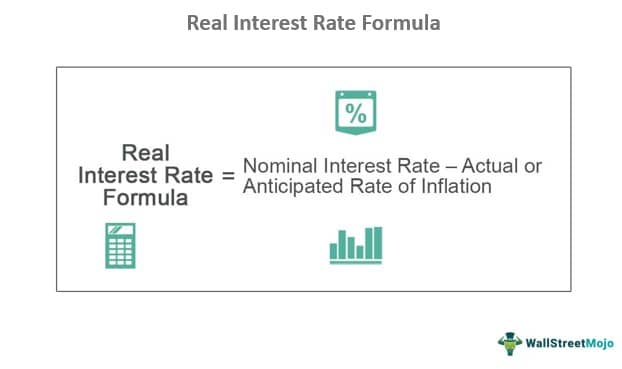

- The nominal interest rate can be used to get the real interest rate for that investment by subtracting the actual or predicted inflation rate.

- It displays the magnitude of the rise or falls in purchasing power. Market-based price increases cause inflation, which causes a proportionate decrease in the purchasing power of money.

Real Interest Rate Explained

Real Interest rates are the rates calculated after considering the inflation-adjusted values of various loans and deposits. It shows the effect in the purchasing power of borrower. Taxes and inflation need to be accounted for to calculate the real returns on any investment and an understanding of this concept is the first step in that direction.

It helps assess and understand how inflation directly impacts any returns on investment and becomes a guiding factor for choosing the right investment avenue. This is also the first step to understanding how macroeconomic forces shape individual money choices and results, thus laying a foundation for making more informed choices by individuals and groups. However, the calculated real interest rate must be taken as an anticipatory value.

Formula

It can easily be calculated by by using the equation for real interest rate and subtracting the actual or expected inflation rate from the rate of interest quoted for any saving or investment, also known as the nominal interest rate.

It helps bring the fact in perspective that investment should first be evaluated for whether it would help retain the purchasing power of initial investment before one even begins to think of actual profits.

How To Calculate?

The equation for real interest rate is used to find the rate of inflation and is calculated on a yearly or monthly basis, and it forms an important economic indicator apart from impacting national and personal finances. Consumer Price Index (CPI) tracks how inflation impacts the prices of consumer goods in the retail sector. This is usually considered the benchmark for measuring inflation and is widely used for making calculations where inflation is taken into account.

Since price rise impacts economic activity more directly than most other factors, governments release figures for the anticipated inflation rate for the coming months and years as well. This is often described as a range for want of exactness, and accurate figures can only be obtained for years passed. Nevertheless, despite being approximations, these anticipated figures hold a great deal of relevance when making estimates for the economy as a whole.

CPI figures come in handy for calculating this rate and help provide a reliable approximation of what one might earn on an investment. Moreover, equipped with the understanding of inflation-adjusted equilibrium real interest rate, one can choose suitable investment avenues and avoid going along with options where the inflation rate might exceed the nominal interest rate, resulting in negative RIR, as we have already discussed.

This would effectively take away the purchasing power of the amount originally invested. By comparison, it would be better to spend the money on consumables instead of investing if the returns don’t keep up with the anticipated inflation rate.

Examples

Let us understand how to calculate long term real interest rate, with the help of some examples.

If an investor made a fixed deposit of $10,000 with an annual interest rate of 3% but the rate of inflation for that year is 3%, the calculation of the real interest rate would be like this.

Solution-

- Nominal Interest Rate =3%

- Actual or anticipated rate of inflation = 3%

Real Interest Rate = Nominal Interest Rate – Actual or Anticipated Rate of Inflation

Therefore,

- =3% – 3% =0%

In our example, it turns out to be 0% which means that the purchasing power of the investment stayed at the same level without experiencing any real change in either direction.

In our example, it turns out to be 0% which means that the purchasing power of the investment stayed at the same level without experiencing any real change in either direction.

If, in the same example, the nominal interest rate was 5% and the inflation rate was the same at 3%, it would result in a 2% real interest rate calculation indicating inflation-adjusted returns. This essentially means the purchasing power of investment went up by 2% in that year.

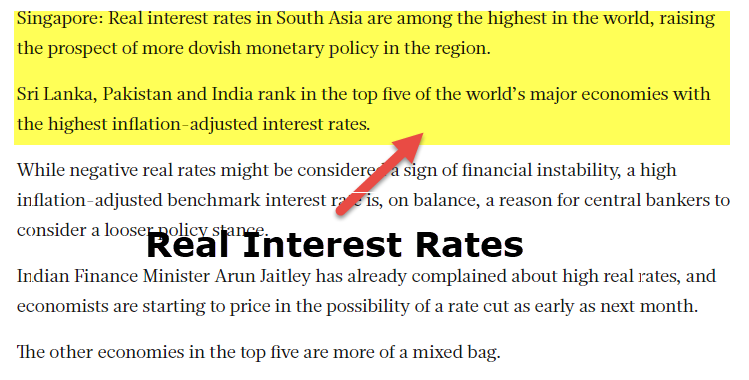

source – gulfnews.com

Taking the basic idea one step ahead, this equilibrium real interest rate is useful in understanding how an investment works and if the returns could be aligned with the goals. Based on an idea of how much one might earn on a specific investment, viable alternatives can also be explored to achieve the investment objective. For instance, if someone is earning 3% annually in a regular savings account, it might translate into a 1% decline in purchasing power if the inflation rate for that year is 4%.

This is why even if the rate of inflation might not appear like an important factor to consider, it can significantly impact the investments.

Thus, the above examples explain how to calculate long term real interest rate.

Uses

Let us understand the uses of real interest rate data.

- It offers a sneak peek into this elegant idea of purchasing power at work by considering the impact of inflation on the returns of any investment.

- Purchasing power and inflation are two interlinked concepts that come into focus here and play a key role in determining the direction of any economy and the state of personal finances.

- It shows the extent of the increase or decline in purchasing power. The rise in prices based on market factors leads to inflation and results in a proportional decline in purchasing power of money, so any fixed amount doesn’t buy an equal amount of goods at different points of time.

- Purchasing power is in a constant state of flux, and inflation is the deciding factor to control which governments create policies to stabilize the economy and help afford its people the worth of their money.

Thus, the above points clearly state the uses of real interest rate data.

Real Interest Rate Vs Nominal Interest Rate

- The nominal interest rate is the one quoted for any deposit or investment, which is simply the percentage of the original amount earned in the form of interest in a specific period. The nominal interest rate does not consider any factor that might affect the rate of interest or returns on an investment, including inflation, in that sense. It is not very helpful in getting an idea of actual returns.

- On the other hand, the real rate takes into account inflation. It provides a means to calculate inflation-adjusted returns on the simplest deposits or investments in a bond or even a regular loan. Utilizing the nominal interest rate, one can deduct the actual or anticipated inflation rate to arrive at the real rate for that investment.

Frequently Asked Questions (FAQs)

How do real interest rates affect inflation?

Real interest rates are interest rates that have been lowered to account for inflation. It reflects the real cost of money to a borrower after adjustment and the real return to a lender or investor.

Why are real interest rate fluctuations significant?

When real rates are extremely low or negative, it makes sense to borrow money and take a small risk; when real rates are higher, it becomes more expensive to borrow, and you can choose to play it safe and forego getting a loan.

What factors impact the real interest rate?

The supply and demand of credit affect interest rate levels; higher or lower levels of demand for credit will result in higher or lower interest rates, respectively.

What are negative real interest rates?

Interest rates fall below 0% with negative interest rates, a type of monetary policy. When there are clear indications of deflation, central banks and other authorities employ this uncommon policy instrument.

Recommended Articles

This has been a guide to what is Real Interest Rates. We explain its formula, differences with nominal interest rate, how to calculate, examples and uses. You may learn more about macroeconomics from the following articles –