Part of our Macroeconomics guide

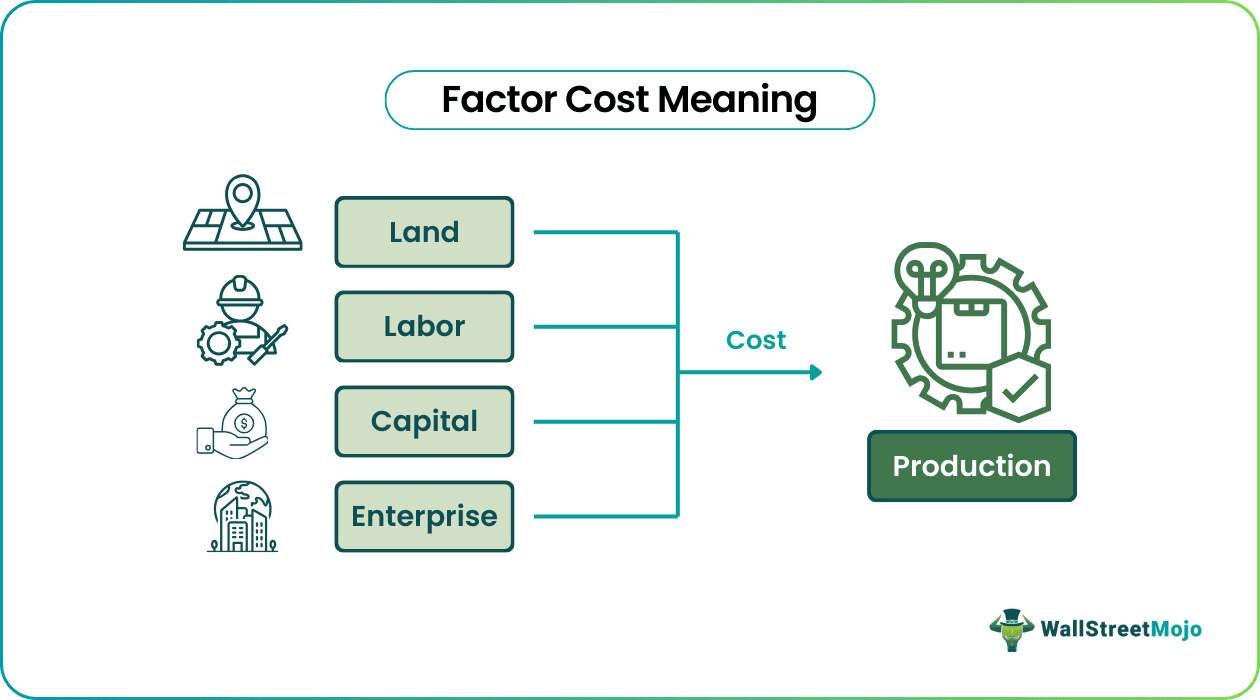

What Is Factor Cost?

Factor cost can be defined as the total cost of all the factors of production in manufacturing a good. Factors of production include capital, land, labor, and enterprise. It does not account for the subsidies received and taxes paid. Hence, it is not the same as the market price.

Also known as national income by type of income, it can present a picture of the cost of factors of production in a country. Since the government maintains regular data on GDP or NNP at factor cost, they can lay down economic policies to support manufacturers.

- Factor cost refers to the total input value that goes into manufacturing a good. Here, the cost of all the relevant factors of production is added.

- At factor cost, a few national income parameters include NNP, GNP, and GDP. The last and the GDP at market price are the two most important measures any government considers.

- Also, when firms calculate the cost of each factor of production, they can find the best possible combination to minimize the cost, thus maximizing the profit.

Factor Cost In Economics Explained

Factor cost is significant in an economy and for a firm involved in manufacturing, as it can indicate what proportion of its cost comes from one factor of production – land, labor, capital, and enterprise.

Business is all about profit maximization. An important part of this is cost minimization. So, when firms can identify which factor is expensive, they can implement measures to avoid unnecessary costs or find less expensive alternatives.

Also, when governments analyze the cost of factors of production in an economy, they can see how each factor contributes to commercial activities. This is important because if the government sees a change in any economic trend or if a factor becomes a barrier to the business, it can establish policies to ease the economy.

For example, suppose there are labor market tensions due to which manufacturing activities have halted. In that case, the government can intervene and help the laborers and the employers find common ground. This will propel economic activity.

Formula

Let’s look at a few measures of national income at factor cost.

- Gross Domestic Product at factor cost

This is a commonly used parameter and helps calculate the output in terms of factors of production.

GDP–FC = GDP–MP + Subsidies – Indirect Taxes

- Net National Product at factor cost

This measures the total value of the cost of factors of production and net factor income abroad, i.e., the amount earned by domestic citizens overseas.

NNP–FC = NNP–MP – Indirect Taxes

- Net Value Added at factor cost

It accounts for the value of commodities and services produced in a country but excludes taxes and depreciation.

NVA–FC = GVA – Depreciation + Subsidies – Indirect Taxes

But we must understand some concepts before using these formulas to arrive at the final result.

- Gross value added (GVA) denotes the value of all goods and services produced in an economy.

GVA = Final value – Value of intermediate consumption

- Gross domestic product at market price (GDP-MP) is the final value of the economic activities in a country at the price at which consumers buy them, hence market prices. It is a widely used measure.

GDP-MP = GVA x MP

- Net national product at market price (NNP-MP) is the final value of economic activities a country produces domestically and internationally, with less depreciation.

NNP-MP = GNP-MP – Depreciation

GNP-MP = GDP-MP + Net factor income abroad

Calculation Example

Let’s work out a quick example. From the information given below, calculate the GDP-FC, NNP-FC, and NVA-FC.

| Particulars | Value (in a million dollars) |

| Domestic sales | 200 |

| Exports | 80 |

| Depreciation | 15 |

| Input goods | 130 |

| Indirect taxes | 15 |

| Imports | 75 |

| Investments | 85 |

| Government spending | 150 |

| Subsidies | 5 |

| Net factor income from abroad | 30 |

GVA = Final value – Intermediate consumption

= (Domestic sales + Exports) – (Input goods)

= (200 + 80) – 130 = $150 million

GDP = Consumption + Investment + Government Spending + Net Exports

= 200 + 85 + 150 + (80 – 75)

= $440 million (Since we are considering the final value, this is GDP-MP)

GNP-MP = GDP-MP + Net factor income abroad

= 440 + 30

= $470 million

NNP-MP = GNP-MP – Depreciation

= $470 – 15

= $455 million

GDP-FC = GDP-MP + Subsidies – Indirect Taxes

= 440 + 5 – 15

= $430 million

NNP-FC = NNP-MP – Indirect Taxes

= 455 – 15

= $440 million

NVA–FC = GVA – Depreciation + Subsidies – Indirect Taxes

= 150 – 15 + 5 – 15

= $125 million

Factor Cost vs Market Price

Factor cost is the total value of the inputs that go into manufacturing a good. It concerns each of the factors of production. The market price, on the other hand, is the final value of a good. It is the price that a buyer pays to purchase the commodity.

The former doesn’t include indirect taxes or subsidies. But these are added to it before selling the product, which constitutes the market price.

Market Price = Factor Cost + Indirect Taxes – Subsidies

Usually, most countries consider national income calculated at market price, as it includes taxes and presents a more accurate picture of expenditure and consumption. However, national income at factor cost is important, too, as it can show the efficiency of each factor of production.

Frequently Asked Questions (FAQs)

1. What isGDP at factor cost?

GDP-FC refers to the total cost of each factor of production. It is an important parameter, second only to GDP-MP (GDP). GDP-FC can be calculated by subtracting the value of indirect taxes from GDP-MP and adding the value of subsidies received.

2. What isNNP at factor cost?

NNP-FC is the total production cost with respect to each factor, plus net factor income from abroad.

3. What is GNP at factor cost?

GNP-FC is the value of GDP-FC minus indirect taxes. It can also be computed by adding net factor income from abroad to GDP-MP and subtracting indirect taxes. Hence, the bottom line is that it considers output without including taxes.

4. What are factor cost and market price?

Factor cost is the cost of factors of production or the total value of inputs, whereas the market price is the final value of the product being sold, which includes indirect taxes.

Recommended Articles

This article has been a guide to what is Factor Cost. We explain the topic in detail, its formula (GDP, NNP, NVA), calculation example, and comparison with the market price. You may also find some useful articles here –