What Is Accrued Revenue?

Accrued revenue refers to a situation where the goods or services have been delivered to the client but the payment for the same has not been received. Accrued revenue journal entries are passed and accounted under the amount receivables in the balance sheet of the company to reflect the value that their clients owe them.

According to accrual accounting principles, recording the revenues is important in the period it was executed. It is called the revenue recognition principle. It is a common feature in the service industry where contracts last well beyond one year. Therefore, these adjustment entries reflect the amount of business done in the period, which otherwise, would not be reflected.

Examples

The most common accrued revenue is the interest income (earned on investments but not yet received) and accounts receivables (the amount due to a business for unpaid goods or services.)

Let us understand the concept in detail with the help of a few practical examples that would give us an in-depth understanding of the concept.

Example #1

- M/s ABC (company) has agreed with M/s K (Individual) to provide 12 plants and machinery in a year. Company ABC identified each plant and machinery as a milestone of the project, and accordingly, they will recognize the revenue after each milestone.

- In this case, Company ABC can recognize revenue on completion of each plant and machinery as accrued revenue whether the same has been billed monthly or once a year. The company ABC can record the same revenue in the books of account, and simultaneously M/s K can record accrued expenses in their books.

Video Explanation of Accrued Revenue

Example #2

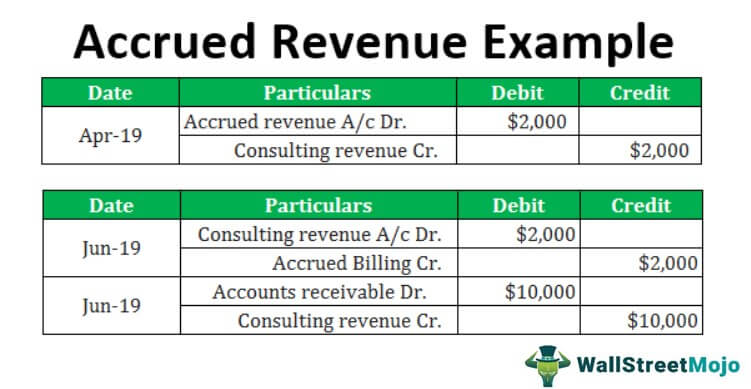

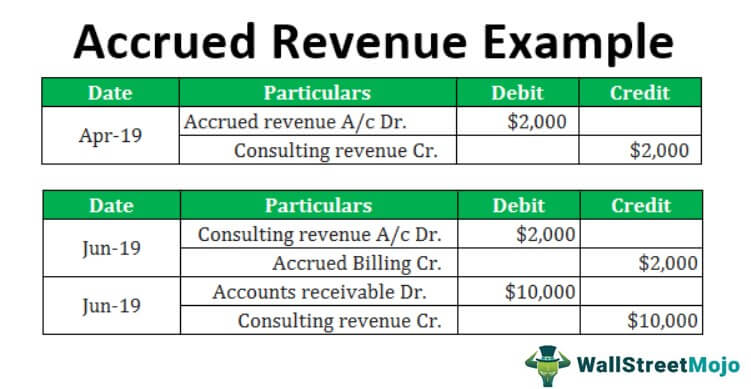

- Company X is a consultancy firm that provides consultancy services to its clients. They charge their clients per-hour basis, i.e., $ 10 p/hr. In April 2019, they had given the consultancy for around 200 hrs. However, the work has not yet been completed, and company X won’t raise the invoice until June 2019, when Company X is expecting to raise the final bill of around $ 10,000.

- Company X records accrued revenue in the books amounting to Rs. $ 2000 ($10 x $ 200) as their income for January 2019, even though the same has not been billed to their client or received payment for the work.

- When company X sends the invoice in June 2019, accrued revenue of $ 10000 shall be converted into accounts receivables. When the client pays the amount, it will get converted into cash.

Example #3

- Mr. A owns a shop that provides his shop to the shopkeeper on a monthly rent of $ 500. The shopkeeper pays the monthly rent in the first week of next month. It means the landlord, Mr. A, does not receive the money for monthly rentals until after the services have been given to the shopkeeper.

- At the end of the year, Mr. A’s income statement would show only 11 payments from the shopkeeper since the last month’s rent shall be paid in the next month’s first week. But Mr. A already provided the rental services to the shopkeeper in the last month of the year, so he should show this earned income as accrued income.

- Accordingly, Mr. A records such transactions in the journal entry by debiting the accrued (revenue) account and crediting the revenue account in the account books.

Example #4

- Another type of accrued revenue is known as Accrued interest revenue.

- In this case, suppose if a company provides loans to the other company, they will earn interest income on loan. A company could accrue interest income every month even if the bill of repayments of the loan was raised semi-annually or annually.

- Ex-Company X gives a loan to Company Y says $4000, on which Company X will receive an interest payment of $ 600 every year from Company Y. Even though Company X receives interest at year-end, the same has to be recorded in the books of accounts monthly. The company would debit accrued billing and credit interest revenue once a month on a proportionate basis, i.e., $ 50 per month.

- Upon sending the final invoice to Company Y, Company X shall debit accounts receivables and credit accrued billing of $ 4000.

Example #5

- We should understand the accrued revenue based on journal entries to be passed in the books of accounts.

- Let’s extend example no two cited above, wherein company X provides consultancy services to their clients. Since the above example allows company X to do the billing in June 2019, i.e., at the end of the project, amounting to $ 10,000. Company X shall record the following journal entries into their books of accounts:-

In June 2019, when Company X raises the complete invoice to their client, the following entries shall be passed:-

Example #6

Emeritus, a higher edtech start-up, which is backed by SoftBank announced in 2023 that they would become a profitable venture in the next accounting or assessment year (2023-24). They raised funds in August 2021 and were valued at approximately $3.2 billion in 2023.

Since their structure of education relies highly on their interactive online classes and other modes of education, their co-founder Damera said that their company has only two major forms of revenue- bookings and accrued.

This company has an accrued revenue that accounts for about 80-85 percent of its revenue – at this scale, revenue recognition software helps track earnings accurately across periods. Their revenue in 2020-21 was $130 million approximately which grew two and a half times in 2021-22 to $430 million

Recommended Articles

This article has been a guide to what is Accrued Revenue and its Examples. Here we explain common examples to understand the Accrued Revenue concept in detail. You can learn more about accounting from the following articles –