Part of our Revenue Recognition guide

What Is Deferred Revenue Expenditure?

Deferred revenue expenditure is an expenditure that is incurred in the current accounting period, but its benefits are incurred in the following or the future accounting periods. This expenditure might be written off in the same financial year or over a few years.

Let us take an example. In the case of a startup company, the firm invests heavily in marketing and advertising initially. They do this to capture some position in the market and amongst competitors. This expense, done initially, reaps the benefits over several years.

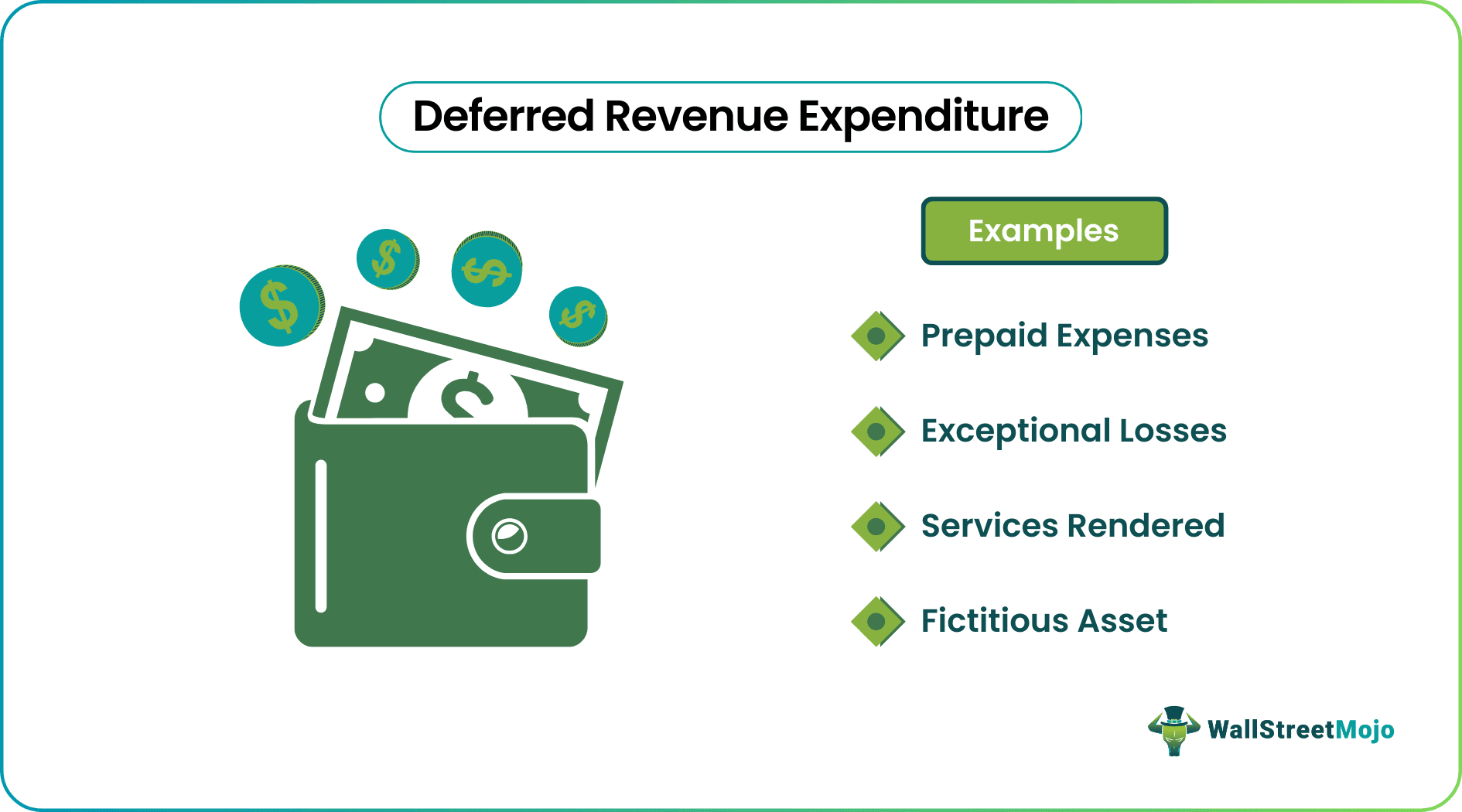

Examples of Deferred Revenue Expenditure

- Prepaid Expenses: The firm makes a substantial investment in certain activities like sales promotion activities – the benefit will be incurred over the number of accounting periods, but the expenditure is born in the same year. This expenditure will be written off over several periods.

- Exceptional Losses: Expenditure relating to exceptional losses by, for example, an earthquake, floods, or unforeseen losses by loss or confiscation of property.

- Services Rendered: Since the expenditure for the services rendered cannot be allocated to one year only, there be no asset created with such expenditure—for example, the cost of research and development for the company.

- Fictitious Asset:Fictitious assets in cases whose benefit is derived over a long period.

Unearned Revenue (Sales) Explained in Video

Features

- Expenditure is characterized by revenue and its features.

- The benefit of the expenditure is accrued for more than one year of an accounting period.

- The expense is huge since it’s a one-time investment for the business and is therefore deferred over a period, which is more than one accounting period.

- These accrue over the future years, either partially or entirely.

Differences between Capital Expenditure and Deferred Revenue Expenditure

- The CAPEX is written off using depreciation expense. However, in the case of deferred revenue expenditure, it is written off over the following 3 to 5 years from the year incurred.

- The benefits from capital expenditure accrue for a more extended period in the business, like ten years or more. On the other hand, the benefits from deferred revenue expenditure are reaped between 3 to 5 years of the business.

- Capital expenditure is incurred, which helps in the creation of the asset. Since the investment helps create assets, these can be created into cash as and when required by the business. These revenue expenditures are incurred mostly on sales promotion and advertising activities and, therefore, cannot be converted to cash.

- Capital Expenditure is done towards any investment that increases a business’s earning capacity. It may mean purchasing an asset for the business like purchasing a plant, machinery, building, copyrights, etc. On the other hand, revenue expenditures mean making an investment that maintains the earning capacity of the business. The company would benefit from this revenue expenditure throughout one accounting period to some 3 to 5 years.

Recommended Articles

This article has been a guide to Deferred Revenue Expenditure and its definition. Here we discuss deferred revenue expenditure examples and their differences from capital expenditure. You can learn more about accounting from the following articles –