Gross Sales Meaning

Gross Sale is a measure of the company’s total sales, be it products or services or both reported by an entity during a particular period, excluding the returns, allowances, rebates, and discounts. It is also called top-line sales. In informal terms, we can say that the revenue from the products has moved off the shelves and reached the customers. It is a gross value, meaning it does not consider any of the adjustments.

How to Calculate Gross Sales?

Sum up the invoice value of all the items sold during the particular period. Then, calculate the sales value based on the selling price before deducting discounts, rebates, returns, or any allowances. By doing this, we will arrive at the top line sales value of the company.

Gross Sales formula can be represented as below –

Gross Sales Formula = Sum of all the Values in Sales Invoices

Gross Sales Examples

Let us now look at examples to calculate Gross Sales.

Example #1

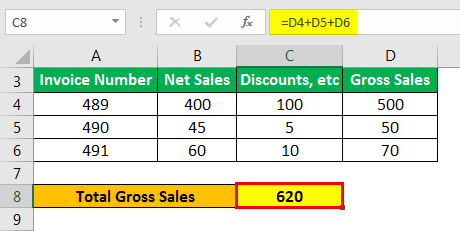

Calculate gross sales from the following invoice details given below –

- Invoice 489 – The net sales were $400. However, a $100 discount was given on the said invoice.

- Invoice 490 – The net sales after the return of goods were $45. $5 of goods were returned.

- Invoice 491 – A shoe had a small defect. After the allowance was given, the total amount paid by the customer was $60. An allowance of $10 was given to the customer for the defect.

Solution:

First, we will calculate sales for each invoice.

Invoice 489

- Gross sales (Invoice 489) = Net Sales + Discount

- = $400 + $100

- = $500

Invoice 490

- Gross sales (Invoice 490) = Net sales + Sales Return

- = $45 + $5

- = $50

Invoice 491

- Sales (Invoice 491) = Net sales + Allowance

- = $60 + $10

- = $70

Now the total will be –

- = $500 + $50 + $70

- = $620

Therefore, the total sales are $620.

Gross Sales Example #2

If a company records revenue from sales of $3 million, the company will record this as the top line sales.

In the same example, if we consider that the company allows a discount of 1% on sales, i.e., $30,000, and refunds $10,000 on account of warranties, returns, etc.

Here also, the top-line sales would be the same as $3 million, but the figure which would consider all the above factors would be net sales. Net sales, hence, would be = $3,000,000 – $30,000 – $10,000 = 2,960,000.

Most investors usually get confused with terms like Gross Sales, Revenue, and Net Sales. Let us now analyze the differences between the three terms.

Revenue vs Sales Explained in Video

Gross Sales vs. Revenue

Since sales form the major block of the total revenue to the company, sales and revenue are the two terms that are often used interchangeably. But there is a slight difference. Let us understand this with the help of a table summarizing the differences between the two.

| Sr. No | Gross Sales | Revenue |

|---|---|---|

| 1 | It is the total income generated by a company from the sales of the company. | Total income generated by a company; |

| 2 | Gross Sales = Units Sold * Sales Price. | Revenue = Sales + Other Income |

| 3 | It indicates the selling capability of the company in the market. | Revenue indicates the ability of the company to allocate resources, invest money, and earn more money. |

Gross Sales vs. Net Sales

| Sr. No | Gross Sales | Net Sales |

|---|---|---|

| 1 | They are the total sales value without any deductions. | Net Sales are the total sales value after deductions from gross. |

| 2 | It is a ‘gross’ figure and hence would be higher in value compared to the net sales. | Net Sales is the total after refunds, discounts, allowances, etc. have been deducted. |

| 3 | Needless to say, It is dependent on the sales that happened during the year and not on net sales. | It is dependent on gross sales since it is derived from net sales. |

| 4 | Gross Sales = Units Sold * Sales Price. | Net Sales = Sales – All Required Deductions |

| 5 | Deductions include Operating expenses, i.e., operational expenses are deducted | Deductions include non- operational expenses, i.e., non-operational expenses are deducted |

| 6 | Though called as the top-line sales, it is slightly less accurate and gives a deceiving picture of the actual sales of the company. | It gives a much more accurate picture of the company’s sales and its realization from sales. This measure is more suitable to be known as top-line sales. |

Presentation of Gross Sales in Accounts

- They are the first title that we can see in an income statement.

- It consists of all the sales transactions made during the period stated in the heading of the income statement, be it monthly, quarterly, half-yearly, or yearly.

- Sales discounts, rebates, returns, and allowances are deducted in the next line.

- After deducting the sales discounts, returns, and allowances from gross sales, the balancing figure is presented in the third line as net sales.

Uses

Some of the uses are as follows:

- It calculates the break-even sales volume at which costs become equal to the sales revenue.

- It is used for various managerial and accounting functions.

- Targets are set to the sales team and marketing personnel, often based on the gross sales figure.

- This measure is important for retail businesses to file tax returns periodically.

Limitations

Some of the limitations are as follows:

- The value is misleading because the amount of sales figures presented are overstated.

- It is a figure that is not subject to any adjustments, only after which the actual sales value can be determined. For this reason, it is not the most sought-after sales value for decision-making or arriving at conclusions.

- This value is only relevant in the consumer-retail industry, where major sales are made.

- The gross sales value prevents consumers from determining.

Conclusion

The sum of all the receipts from sales of an entity unaffected by any adjustments is gross sales. Although they have their uses in accounting, presentation, and tax payment, they are not of much use after the net sales have been calculated. At first glance, it may look good, but that may be before the exorbitant discounts, refunds, sales returns, and adjustments, which might not look as good. Hence, net sales is a slightly more practical sales figure because it represents the value after accounting for adjustments.

Recommended Articles

This article has been a guide to what gross sales are and their meaning. Here we discuss the formula to calculate gross sales and its uses, presentation, and limitations. You can learn more about accounting from the following articles –