Part of our Revenue Recognition guide

What is Contra Revenue?

Contra Revenue is a difference in gross revenue and net revenue. It usually has a debit balance and is a helpful tool for the company to know the product specifications, whether it is optimum or not, as per customer requirements.

Types of Contra Revenue

- Sales Returns – If the company sells the goods and it returns due to some reasons such as defective goods or if they are not as per customer requirement, sales return decreases the sales and debtors if sales are made on credit.

- Sales Allowance/Rebate – If the company sells the goods and has some minor defects, then it sells such goods with some rebate/ allowance.

- Sales Discount – When the company sells the goods to a customer who purchases in cash mode, the company allows the discount to that customer for prompt payment. This discount is also known as a cash discount.

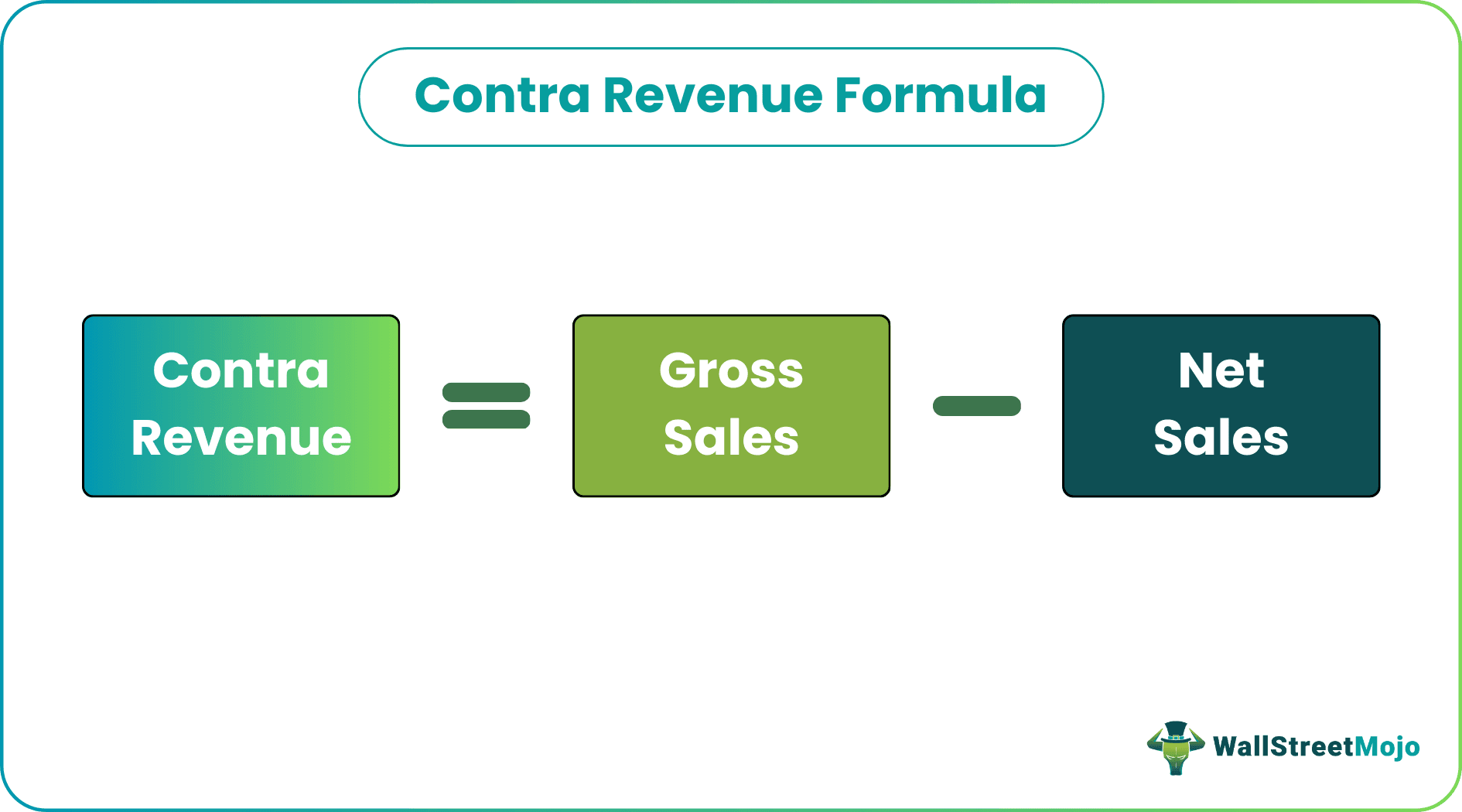

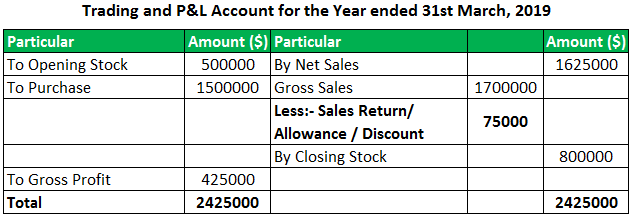

Formula

CR = Gross Sales – Net Sales

Examples of Contra Revenue

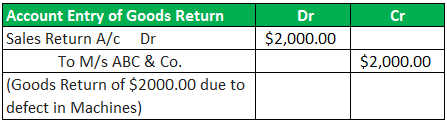

Example #1 – Based on Sales Return

M/s L&T Limited sells the construction equipment machines to M/s ABC & Company for $15000.00 on Credit. After some days, M/s ABC & Co. return the construction equipment machines & $2000.00 due to a defect in them.

In the above case, the CR amount is $2000.00, which will be adjusted from sales to $15000.00, and in the accounting book, sales are to be recorded at $13000.00.

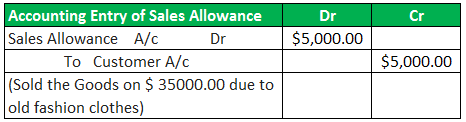

Example #2 – Based on Sales Allowance

M/s XYZ Company has some old fashion clothes, and they want to sell the same on an urgent basis. There is a customer in the market who wants to purchase such clothes, but he knows the market scenario of the cloth industry. M/s XYZ Company agrees to sell the goods for $ 5000 less than the original sale amount, which is $40000.00.

In the above case, the company will bear a loss margin of $5000.00 on clothes, and the same will be adjusted from the sales account. The CR amount is $5000.00

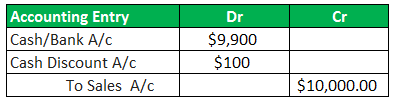

Example #3 – Based on Cash Discount

M/s EFG & Co. sells the Goods $10000.00 with Cash/Sales Discount @ 1% to M/s MNO & Co…

In the above case, the company will bear a loss margin of $100, and the contra revenue amount is $100.00.

Accounting of Contra Revenue

The company should minus the sales return/allowance/discount from gross sales in the above case.

There is one more method that can be used for accounting which is as below:-

In the above method, we debit the contra revenue account in the trading account, but generally, the company uses the first method of accounting for contra revenue.

Revenue vs Income Explained in Video

Advantages

- The effect of contra revenue in income statements provides accurate financial information for the company.

- The company can estimate the quality of products based on sales return quantity and amount of product.

- Sale Discount increases the cash inflow and reduces bad debts.

- Due to the sale discount, the company gets prompt payment, which reduces the collection efforts of staff.

Disadvantages

- If the company is manufacturing such products that have market competition, then the company will have to maintain the policy of sales return, sales allowance, and sales discount.

- It increases the extra cost and time for accounting for such transactions.

- It decreases the profit and profit margin of the company.

- Contra Revenue accounting policy is applicable for Small Businesses.

Limitation

- It increases the extra efforts of the company.

- Accounting for contra revenue is very complicated, as the same is increased accounting work. It adversely affects many accounts such as cash account if the company sells the goods on cash, debtors account, if the company sells the goods on credit, stock account, and sales, account as the same as reversed.

- The company will have to maintain separate human resources for such accounting.

Important Points

- A company should have a policy not to return the goods sold and not provide sales rebates and discounts on products.

- The company should know the reasons for the increase in contra-revenue every month to save extra cost and time.

- The company should use the first method of accounting for contra revenue so that financial statements can be represented better and as per accounting guidelines.

Conclusion

The company should maintain a separate accounting of contra revenue for a better presentation of financial statements and estimate the product’s quality.

Recommended Articles

This has been a guide to what is Contra Revenue Account & its definition. Here we understand the formula of contra revenue along with journal entries examples, advantages, disadvantages, and limitations. You can learn more about accounting from the following articles –