Part of our Revenue Recognition guide

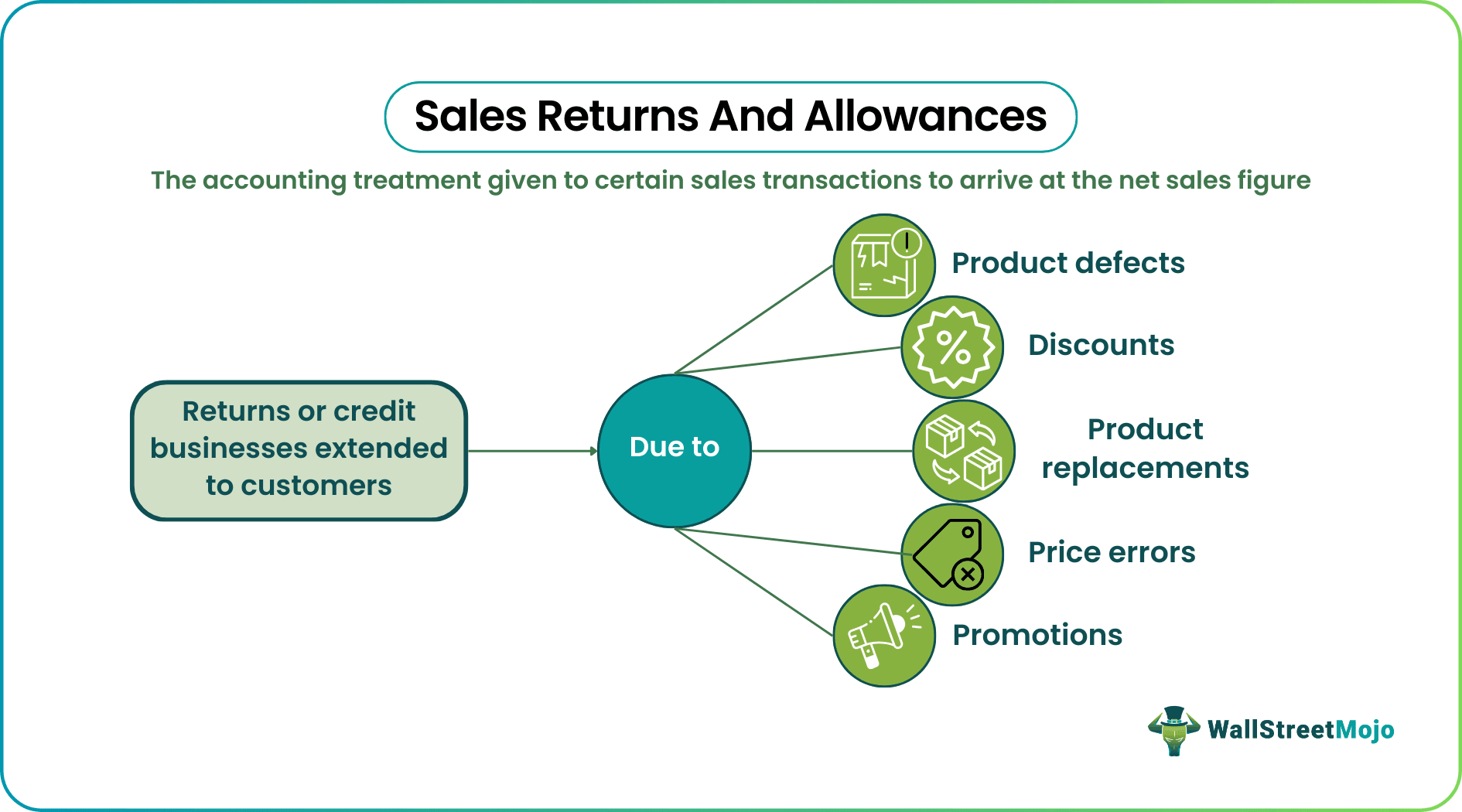

What Are Sales Returns And Allowances?

Sales Returns and Allowances (SRA) are contra-revenue accounts with negative balances. They are used to record product returns and allowances issued to customers. For this, businesses deduct the amount identified under the returns and allowances head from the gross sales figure, and the net sales figure is derived from this calculation.

Retailers and shop owners can leverage this data to identify issues with product shipping, understand customer return and refund reasons, and inform investors and creditors about the reduction in revenue due to returns, allowances, and discounts. When customers accept damaged products in return for a discount on the selling price, these accounting entries are made.

- Sales returns and allowances are associated with contra revenue accounts that show debit balances. These accounts document both customer-initiated product returns and allowances granted by a company to its customers.

- Businesses use this information to determine issues with product quality, shipping, customer expectations and satisfaction levels, refund volume, etc. They also use it to update creditors and investors about the nature and reasons for refunds, concessions, and rebates.

- The formula to compute it is gross sales revenue less net sales revenue.

- When a customer returns a product or requests an allowance, a credit note in duplicate is issued. This is recorded in two accounts and given the following accounting treatment: Reduce the revenue account and Increase the contra account.

Sales Returns And Allowances Explained

Sales returns and allowances are important figures in accounting, reflecting the reduction in a company’s revenue due to returned products and customer discounts. Sales returns refer to the situations where customers bring purchased products back to the seller and demand a partial or full refund due to defects, damage, general dissatisfaction, incorrect item description, wrong item, etc. Sales allowances, on the other hand, are discounts given to customers for keeping such defective or unwanted products instead of returning them.

It usually appears as a line item in the income statement that shows the reduction in gross sales. It is a contra account to the sales account. The SRA normal balance is usually a debit balance, unlike sales accounts, which have a credit balance.

When customers receive damaged products, they typically ask for refunds or wish to be compensated via suitable discounts. In such cases, sellers extend credits or refunds, depending on customers’ demands, and record such transactions in the prescribed accounting format. Failing to record and track these returns and allowances properly can lead to several adverse consequences for companies. Some of them are as follows:

- Tracking a company’s expenses becomes tough.

- Accurate sales figures will not be available.

- There will be a mismatch between sales and products in stock.

- As the total sales value of returned items will be unclear, companies will not be able to understand the reasons for returns. It means quality improvement will become challenging.

- Evaluating the total amount of allowances in the context of gross sales is crucial for performance analysis.

- Functions like logistics, inventory control, quality assurance, and customer service can only be improved based on SRA insights.

If a retailer records considerable SRA for specific products, it is advisable to sell at a discount and earn revenue instead of spending more money on returning them to the supplier. This will also help clear the inventory faster than under normal circumstances.

SRA gives valuable business insights and input. Companies can track product quality, logistics and inventory management efficiency, pricing and promotion strategies, and customer satisfaction levels, among other things. To determine debit or credit entries, a company must record the refunds (total and partial) and discounts to reflect revenue reduction. However, they must also record the relevant credit entries in case of partial refunds and discounted sales.

All returned items and items subject to discounts/allowances must be reflected in the company’s income statement. These returns and allowances, in turn, reduce either credit sales, accounts receivable, or cash in the company’s balance sheet.

How To Record?

For any item returned or sold at a discount, a credit memo in duplicate is created. The customer receives the original copy, and the seller keeps the duplicate of the memo. Credit memos are then used to either make SRA journal or voucher entries in the existing SRA journal; they are recorded under the relevant serial numbers. The entries are made in the following format:

| Date | Account credited (name of the account) | Credit memo no. (recording the item returned) | Posting reference (used for posting the entries) | Amount (sales price of the returned item) |

Next, the sales returns and allowances are recorded using two accounts:

- Revenue account: The original sales price of goods is recorded here.

- Contra revenue account: It contains the details of returns, allowances, and discounts given to customers, reducing the value of the original selling price.

| Journal entry | |

| Revenue | Original selling price |

| Contra revenue | Sales returns and allowances |

The contra revenue account has a debit balance since it is subtracted from the sales revenue account.

- For credit sales: The seller credits the Accounts Receivable account for the amount of the refund or discount granted. This reduces the outstanding balance that the customer owes.

| Credit Sales – Returns and Allowances | ||||

| Account Name | Account Type | Financial Statement | Debit | Credit |

| Sales Returns and Allowances | Contra Revenue | Income Statement | $$ | |

| Accounts Receivable | Asset | Balance Sheet | $$ | |

- For cash sales: The seller credits the cash account for the value of the returned/allowed item as the money is being returned to the customer.

| Cash Sales – Returns and Allowances | ||||

| Account Name | Account Type | Financial Statement | Debit | Credit |

| Sales Returns and Allowances | Contra Revenue | Income Statement | $$ | |

| Cash | Asset | Balance Sheet | $$ | |

To record the normal balance of sales returns and allowances in financial statements, a business must record contra-sales revenue in the revenue section to show the following:

- SRA is a contra-revenue account; it has a debit balance and offsets the Sales account. It is listed directly below the Sales account on the income statement, typically as a deduction.

It can be recorded as shown below:

| Income Statement for SRA | ||||

| Account Name | Account Type | Financial Statement | Debit (-) | Credit (+) |

| Sales revenue – Gross | Revenue | Income Statement | $$ | |

| Sales Returns & Allowances | Contra revenue | Income Statement | $$ | |

| Sales revenue – Net | Net balance = (Revenue – Contra revenue) | Income Statement | $$ | |

Examples

Let us study a few examples to understand the topic.

Example #1

Suppose a customer bought a leather jacket from Jill, a shop owner, for $300. However, a week later, they returned the jacket, citing problems with its fitting and quality. Jill processed the return and refunded $300.

- Sales returns and allowances = $(-300)

- Accounts receivables = $300

In the income statement, the SRA account is subtracted from sales to denote contra revenue. If this entry is not made, Jill’s records might wrongly reflect revenue instead of contra revenue.

Example #2

Jenny has a lamp shop in New York. She made total sales of $10,000 in a month. However, some customers found problems with their lamps and returned them. The total number of lamps returned amounted to $1,000. Now, Jenny must record this amount to ensure her financial statements reflect the true picture of her business.

- For credit sales, Jenny must debit Sales Returns & Allowances and credit Accounts Receivable.

- For cash sales, she must debit Sales Returns & Allowances and credit Cash.

Her income statement reflects the following:

Sales revenue = $10,000

Less: Sales Returns & Allowances = $1,000

Jenny’s net sales = $9,000

Frequently Asked Questions (FAQs)

1. What type of account are sales returns and allowances?

Since sales returns and allowance are debited from gross sales, it has a negative balance. Therefore, due to the negative balance, these accounts are also called contra-revenue accounts. By recording the total sales returns and allowances separately in contra revenue accounts, management closely monitors overall sales against the percentage of returns and allowances in a given period.

2. Is sales returns and allowances a temporary account?

Accounts, such as earned interest, sales discounts, and sales returns, are considered temporary accounts for accounting purposes. However, in general, companies consider other relevant factors while determining the accounting treatment of a business transaction.

3. Are sales returns and allowances an expense?

No. Sales returns and allowances are not expenses, but they are recorded as deductions from a company’s gross sales. This account has a negative or debit balance, so it is also called a contra-revenue account.

4. How to calculate sales returns and allowances?

The formula used to calculate it is:

Contra Revenue Account = Gross Sales Revenue – Net Sales Revenue

Recommended Articles

This has been a guide to what are Sales Returns And Allowances. Here, we explain the concept along with how to record them, and their examples. You can learn more about financing from the following articles –