Part of our Revenue Recognition guide

What Is The Direct Write-Off Method?

The Direct Write-off method is a process of booking the unrecoverable part of receivables that are no longer collectible by removing that part from the books of accounts without prior booking for the provisions of bad debts expenses. It is waived off using the direct write-off method journal entry to close the specific account.

In other words, it can be said that whenever a receivable is considered to be unrecoverable, this method fully allows them to book those receivables as an expense without using an allowance account. It should also be clarified that this method violates the matching principle. As in, Expenses must be reported in the period in which the company has incurred the revenue.

Direct Write-Off Method Explained

The direct write-off method is the simplest method to book and record the loss on account of uncollectible receivables, but it is not according to the accounting principles. It also ensures that the loss booked is based on actual figures and not on appropriation. But it violates the accounting principles, GAAP, matching concepts, and a true and fair view of the Financial Statements.

Seeing and considering all these points, it is concluded that only being a simple method to record the transaction is not the requirement of an accounting transaction. It must be within the rules and laws framed by the bodies for an accounting of transactions so that a true and correct picture of the Financial Statements can be shown to the stakeholder of the entity. Therefore it is not advised to use the Direct Write-off Method to book for the uncollectible receivables. Instead, the company should look for other methods such as appropriation and allowance for booking bad debts for its receivables.

Bad Debts Expenses for the amount determined will not be paid directly charged to the profit and loss account under this method. The direct write-off method is used only when it is inevitable that a customer will not pay. There is no recording of the estimates or use of allowance for the doubtful accounts under the write-off methods.

Journal Entries

→ Explore all 30 Journal Entries articles

Let us understand the journal entries passed during direct write-off method accounting. This shall give us a deeper understanding of the process and its intricacies.

The write off amount is debited as the expense in the period approved to write off in the income statement. It does not affect the sales performance of the entity in the current period and the previous period. It affects only the bottom line of income in the current period. It is because the expenses are recognized in this period. It is probably against the matching principles.

Examples

Let us understand the direct write-off method journal entries with the help of a couple of examples. These examples shall give us a practical overview of the concept and its intricacies.

Example #1

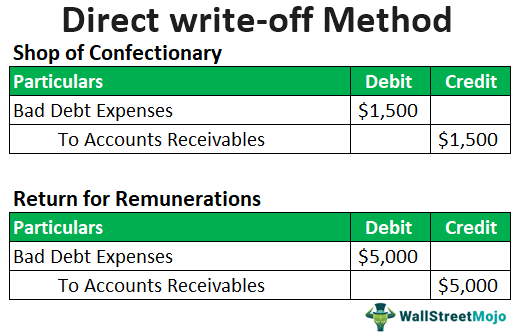

Assume Natalie owns a shop of confectionery. Natalie has many customers who purchase goods from her on credit and pay. One of her customers purchased products worth $ 1,500 a year ago, and Natalie still hasn’t been able to collect the payment. After trying to contact the customer a number of times, Natalie finally decides that she will never be able to recover this $ 1,500 and decides to write off the balance from such a customer. Using the direct write-off method, Natalie would debit the bad debts expenses account by $ 1,500 and credit the accounts receivable account with the same amount.

Example #2

An accounting firm prepares a company’s financial statements as per the laws in force and hands over the Financial Statements to its directors in return for a Remuneration of $ 5,000. The remuneration has been outstanding for a year now. The firm is taking regular follow-ups with the Company’s directors, to which the directors are not responding. The firm then debits the Bad Debts Expenses for $ 5,000 and credits the Accounts Receivables for $ 5,000. The firm partners decide to write off these receivables of $ 5,000 as Bad Debts are not recoverable.

Reasons Why it is not preferred in the Accounting Profession?

Although it is widely followed and an integral part of income tax reporting structure in prominent countries, accounting professionals do not prefer using it for a variety of reasons, let us understand them in detail through the explanation below.

- The accounts receivable at the end of the financial year would be most likely to be reported in the balance sheet at an amount greater than the amount received from those receivables.

- The matching principle isn’t followed as the losses from this account are recognized as bad debts or several uncollectible periods after the income was earned

- The bad debts expenses resulting from the operating activities on credits will appear on the income statement or profit & loss account only after identifying these bad debts and altering them from the company’s accounts receivables.

- The contra asset account compilations are avoided if the direct write-off method is used. No provisions or reporting of provisions are required in this method.

Advantages

Despite the fact that it violates the balancing principle of accounting, it is a mandate under the US income tax reporting. Let us understand its advantages through the discussion below.

- The main advantage of the Direct Write-off method journal entry is that it is straightforward to book and record in books of accounts. Companies only have to pass two journal entries for the amount of the customer’s bad debt.

- The other advantage is that the company can write off its bad debts on its annual tax returns.

- The contra asset account compilations are also avoided if this method is used.

- There are remote chances of error, considering no calculation of estimates of doubtful debts is required. The risk of overstating and understating expenses in the income statements is also minimized.

- Since tax returns are prepared on a cash basis, this method of bad debt expenses is the most appropriate and would save us any extra calculations or work to prepare income tax returns.

Disadvantages

Despite the advantages mentioned above, there are a few factors that prove to be a disadvantage. Let us discuss them through the points below.

- The major disadvantage of the Direct Write-off method accounting is the possibility of expense manipulation because companies record expenses and revenue in different periods.

- Another disadvantage of direct write-off is that the balance sheet is not accurately representing the company’s accounts receivables.

- One major disadvantage is that it fails to maintain the financial statements according to the generally accepted accounting principle (GAAP).

- A violation of accounting principles means that the financial statements are not portraying an accurate and fair view of the business.

- It goes against the accrual system of accounting and violates the matching principle and the prudence concept.

Direct Write-Off Method Vs Allowance Method

Default in debt provided to a client or a third party can be a major pain point for businesses. Accounting for them in the books is an integral part of managing the risks of the business. The two models used for such provisions are the direct write-off method accounting and the allowance method.

Even though they are both used to account for unrecovered debts, there are differences in their fundamentals and implications. Let us understand them in detail through the comparison below.

Direct Write-Off Method

- Under this method, bad debt is directly charged and accounted as an expense as soon as it is clear that it might not be paid.

- The recognition of bad debts is delayed under this method. However, the exact amount is written-off under this method as it is derived from the unpaid invoice.

- It is also vital to note that this method violates the matching principle which states that expenses must be recorded in the same period as the revenue being incurred.

- The unrecovered invoice is debited from accounts receivables and credited to bad debt expenses to close the account.

Allowance Method

- This method is used by creating an allowance account in the same period as the revenue generation or credit sales.

- It is also commonly referred to as allowance for doubtful debts.

- Under this method, it is difficult to determine the exact amount of default as it is recovered from an allowance account and not from the invoice like the previous method.

- It is in ordinance of the matching principle as the allowance account is opened in the same period.

Recommended Articles

This has been a guide to what is the Direct Write-off Method. Here we explain its examples, advantages, disadvantages, and compared it with allowance method. You can learn more about accounting from the following articles –