What Is The Ending Inventory Formula?

The Ending Inventory formula refers to the mathematical equation that helps calculates the value of goods available for sale at the end of the accounting period. Usually, it is recorded on the balance sheet at a lower cost or its market value.

The ending inventory value depends on different factors, which are taken into consideration for the formula to ensure the volume of goods available at the end of an accounting period is accurate. These factors or components include the beginning inventory (at the beginning of an accounting year), the purchases, and the sales figures.

Ending Inventory Formula Explained

Ending Inventory is the value of goods or products that remain unsold, or we can say that remains at the end of the reporting period (Accounting period or financial period). It is always based on the market value or cost of the goods, whichever is lower. It makes sense to keep track of the Inventory as the same is carried forward to the next reporting period (Accounting or Financial) and becomes the Beginning Inventory. Any inaccurate measure of Ending Inventory will result in financial implications in the new reporting period.

Also, the valuation of Inventory has a widespread impact on the various line items on the Income Statement (namely, Cost of goods sold, Net Profit, and Gross Profit) and Balance Sheet (namely, Current Assets, Working Capital, Total Assets, etc.) which will ultimately impact the various important financial ratios (namely, Current Ratio, Quick Ratio, Inventory Turnover Ratio, Gross Profit Ratio, and Net Profit Ratio to name a few).

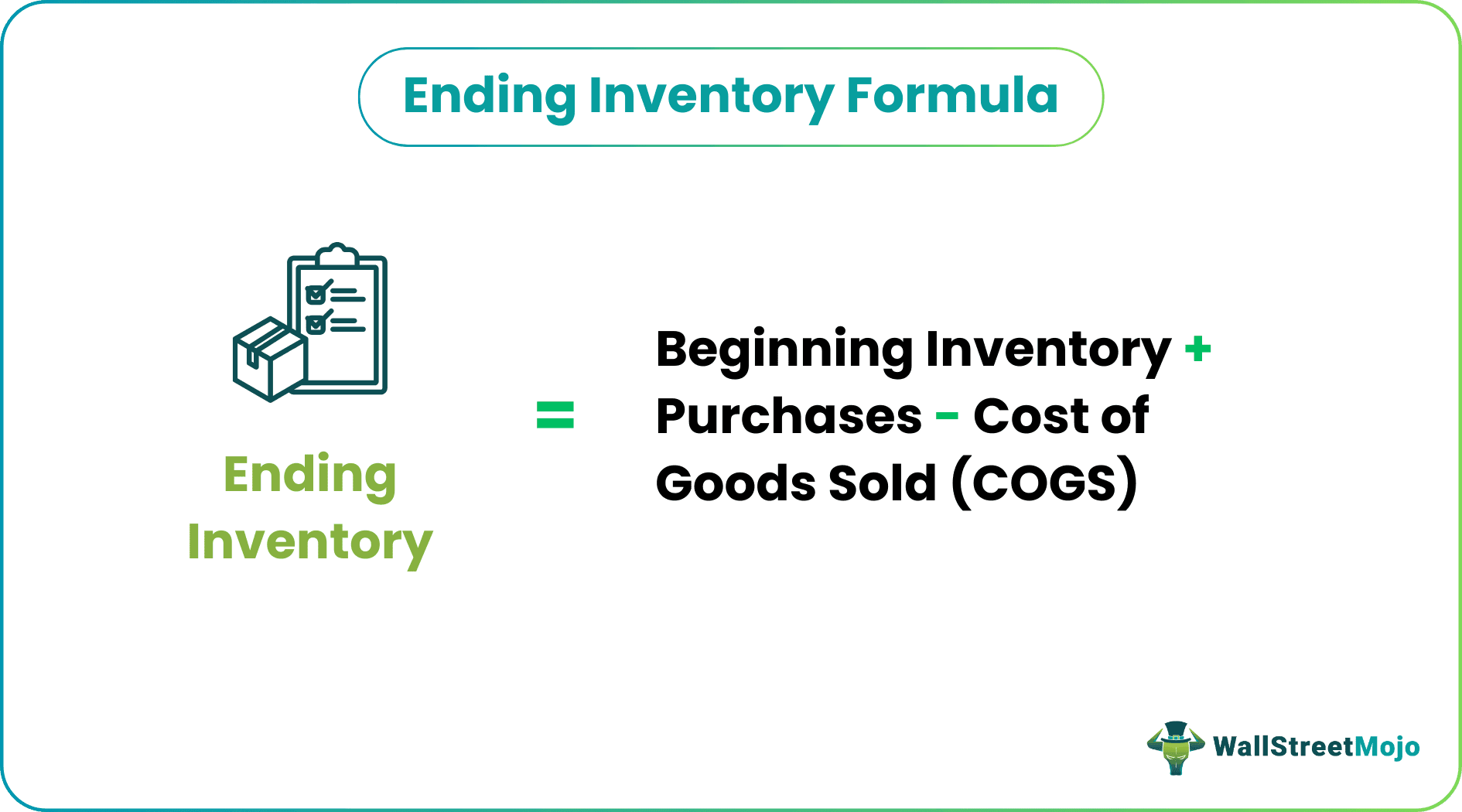

The formula that makes calculating the inventory at the end of an accounting year is given below:

Ending Inventory = Beginning Inventory + Purchases -Cost of Goods Sold (COGS)

It is also known as a closing stock and normally comprises three types of Inventory namely:

- Raw Materials

- Work in Process (WIP)

- Finished Goods

Methods

The firm’s value Ending Inventory calculation is based on any of the three methods mentioned below:

#1 – FIFO (First in First Out Method)

Under FIFO Inventory Method, the first item purchased is the first item sold, which means that the cost of purchase of the first item is the cost of the first item sold, which results in the closing Inventory reported by the business on its Balance sheet showing the approximate current cost as its value is based on the most recent purchase. Thus in an Inflationary environment, i.e., when prices are rising, the Ending Inventory will be higher using this method than the other methods.

#2 – LIFO (Last in First Out Method)

Under the Last In First Out Inventory Method, the last item purchased is the cost of the first item sold, which results in the closing Inventory reported by the Business on its Balance Sheet depicting the cost of the earliest items purchased. Ending Inventory is valued on the Balance Sheet using the earlier costs, and in an inflationary environment, LIFO ending Inventory is less than the current cost. Thus in an Inflationary environment, i.e., when prices are rising, they will be lower.

#3 – Weighted Average Cost Method

Under this, the average cost per unit is computed by dividing the total cost of goods available for sale. Ending Inventory is valued by multiplying the average cost per unit by the number of units available at the end of the reporting period.

Examples (with Excel Template)

Let us consider the following instances to understand how ending inventory is calculated using formula:

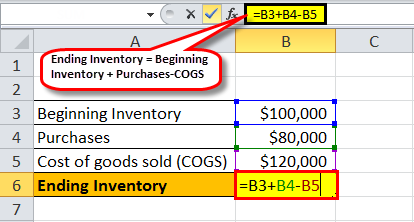

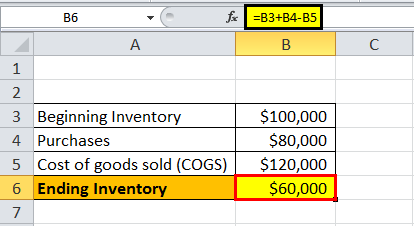

Example #1

ABC Limited started the production with an opening Inventory worth $100000. During January, ABC Limited purchased Inventory amounting to $50000 on 16th January and $30000 on 25th January. On 29th January, ABC Limited sold products amounting to $ 120000. Calculate the Ending Inventory for the same.

So, it will be –

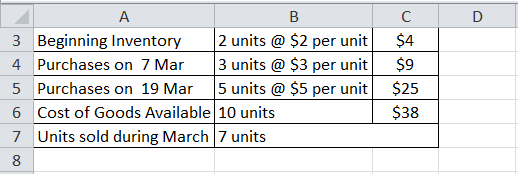

Example #2

XYZ Limited has furnished the Inventory data for March 2018. Do the ending inventory Calculation under the LIFO, FIFO, and Weighted Average Cost Method.

Inventory Data –

By using the above-given data, do the calculation using all three methods.

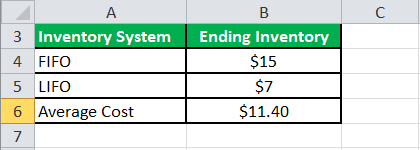

Using FIFO Ending Inventory Formula

Since the first purchased units are sold first, the value of the seven units sold at the unit cost of the first units purchases and the balance of 3 units, which is the ending Inventory cost, is as follows:

- = 3 units @ $5 per unit= $15

Using LIFO Ending Inventory Formula

Since the last purchased units are sold first, the value of the seven units sold at the unit cost of the last units purchases and the balance of three units, which is the ending Inventory cost, is as follows:

= 2 units @ $2 per unit + 1 units @ $3 per unit = $7

Using Weighted Average Cost Ending Inventory Formula

Since the units are valued at the average cost, the value of the seven units sold at the average unit cost of goods available and the balance of 3 units, which are the ending Inventory cost, is as follows:

- Average Cost per unit= ($38/10) = $3.80 per unit

- = 3 units @ $3.80 per unit= $11.40

Therefore,

Thus we can see the value of the Inventory is affected to a large extent by the method of valuation that the business in question adopts.

Recommended Articles

This has been a guide to Ending Inventory Formula. Here, we explain the concept along with the methods to calculate and examples. You can learn more about Accounting from the following articles –