What Is The Net Realizable Value Formula?

The Net Realizable Value formula refers to the mathematical expression or equation that helps calculate the net realized profits expected to be obtained from the sale of assets less the amount incurred in the process of achieving the sales figure. It is primarily used to identify and value the inventory or receivables.

Net Realizable Value of an asset is at which it can be sold after deducting the cost of selling or disposing of the asset. Since in NRV, a firm also considers the cost, hence it is known as a conservative approach to the transaction.

Net Realizable Value Formula Explained

The net realizable value formula calculates the net realizable value and gives a figure that firms can expect as profit. This is obtained when the disposable costs related to sales is subtracted from the selling price of an asset. Based on this figure obtained, the firms determine the value of their asset.

The firm remains concerned about evaluating the assets properly, which makes calculating NRV a conservative approach, indicating that the firm should not overstate the profit by showing a lesser value of its assets.

NRV is the valuation method which is adopted by the firms to ensure they price the assets properly. To calculate, the selling price of the asset is considered and then, the other costs incurred to achieve the sales is subtracted from it. These costs are disposale costs, including transport fees, taxes, etc.

For any company, accounts receivables and inventory are the two asset forms that it maintains. The net realizable value formula helps in determining the value of both. The NRV analysis that companies perform is accepted by generally accepted accounting principles (GAAP) as well as International Financial Reporting Standards (IFRS).

Net Realizable Value Explained in Video

How To Calculate?

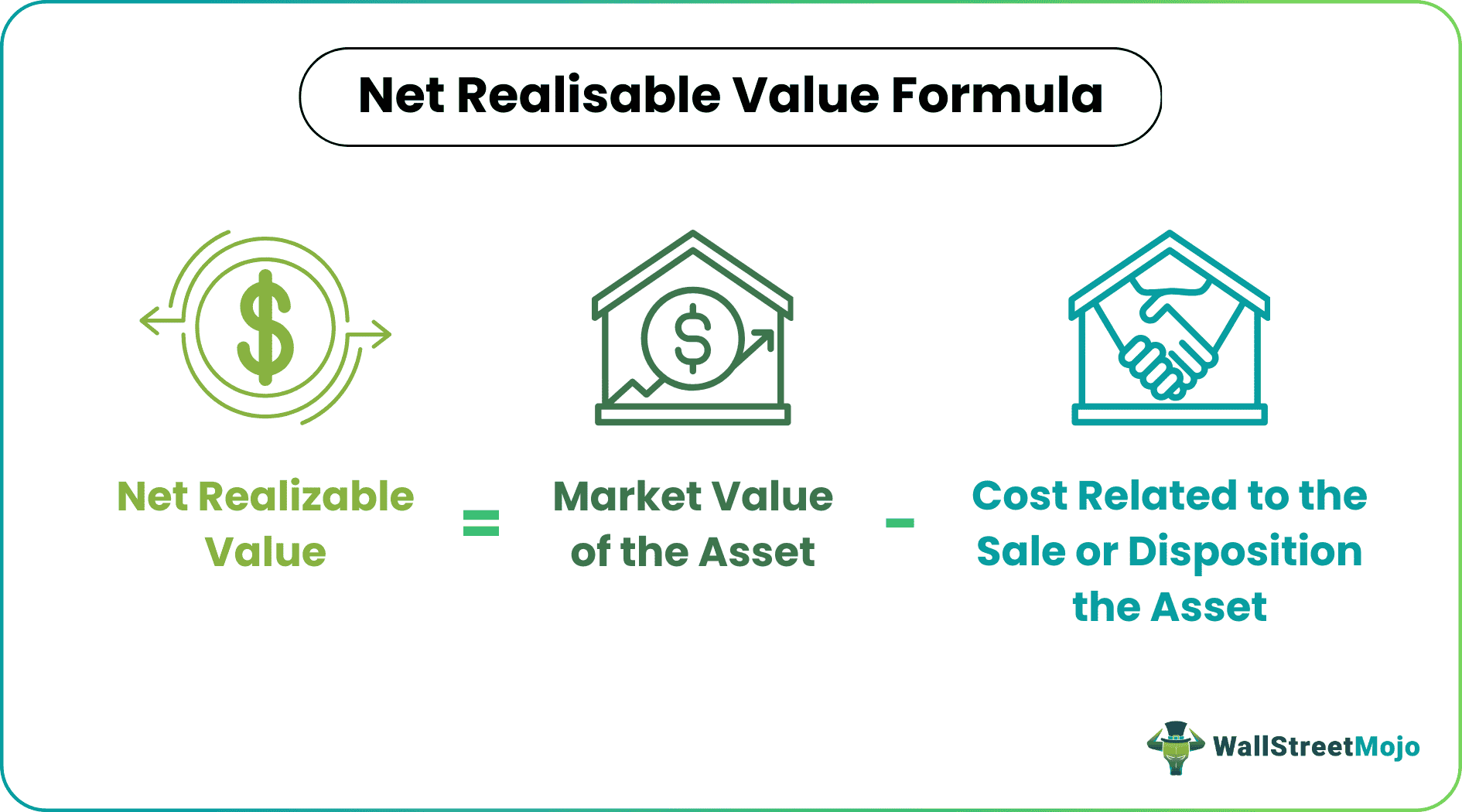

The formula used for calculating NRV is:

Net Realizable Value Formula = Market Value of the Asset – Cost Related to the Sale or Disposition of the Asset

However, it is important to know the steps to follow to make an accurate calculation besides knowing the formula. Listed below is a series of steps that one must consider for a reliable NRV analysis.

For calculating NRV, below steps is to be taken:

Identify the market value of the asset.

Identify the cost related to the sale of the asset.

Subtract the cost from the market value of the asset.

It is calculated by subtracting the cost of selling or disposing of the asset from its market value.

NRV = Market Value of Asset – A Cost of Selling that AssetUnder the cost of selling, the firm calculates any kind of costs which are associated with the sale of that asset, such as transportation or commission cost.

If the asset is Accounts Receivable, then, there is no physical cost such as transportation. But there can be some customers who can default on paying to the company. For calculating NRV of Account Receivables, a firm will have to calculate that amount that can be defaulted by customers, which are known as “Provision for Doubtful Debts.”

NRV of Account Receivables = Market Value- Provision for Doubtful Debts

Examples

Let us consider the following examples to understand how net realiable value formula works:

Example #1

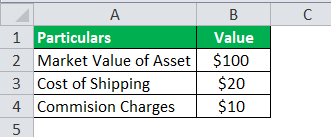

Let’s say a firm has an asset with a market value of $100. The cost of shipping that asset is $20, and commission charges are $10.

Use the following data for the calculation of the Net Realizable Value.

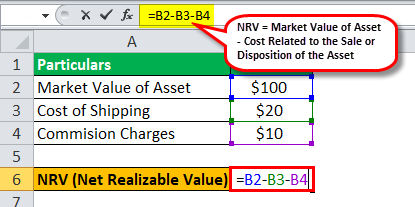

Calculation of Net Realizable Value can be done as follows,

The total cost of selling = $30

Hence Net Realizable Value of Asset = $100 – 30

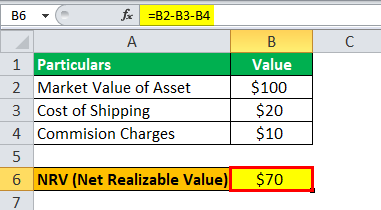

NRV will be –

NRV =$70

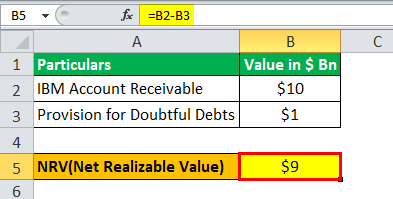

Example #2

IBM is a US-based software company with more than $80 Bn of revenue per year. In the Financial year 2019, the market value of Accounts Receivable (which is an asset) for IBM is $10 Bn. This means IBM is expected to receive this amount from customers who have already been recognized as revenue in its accounts. So, the value of this asset is $10 Bn. But for calculating the Net Realizable Value, IBM will have to identify the customers who can default on their payments. This amount is entered into accounts as “Provision for Doubtful Debts.” Let’s say this amount is $1 Bn.

Use the following data for the calculation of the Net Realizable Value.

So Net Realizable value for “Account Receivable” for IBM can be calculated as follows:

NRV = Market Value- Provision for Doubtful Debts

NRV= 10- 1

NRV will be –

Hence with conservative method NRV of Account Receivable for IBM is $9 Bn.

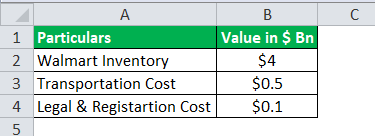

Example #3

Walmart is a US-based retail supermarket chain-based company with around $500Bn of revenue in 2018. In the Financial year 2018, the market value of inventory (which is also an asset) for Walmart is around $44 Bn. Out of it, Walmart is going to sell some part of the inventory to another company for $4 Bn for offloading purposes. Walmart needs to decide the NRV of this part of the inventory. For that, Walmart needs to calculate the cost associated with the Sale of Inventory. The transportation cost is $500 Mn, and legal and registration charges are $100 Mn.

Use the following data for the calculation of the Net Realizable Value.

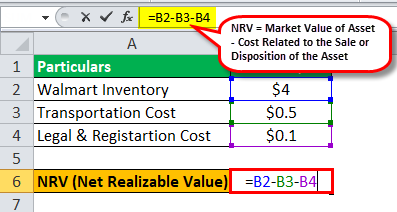

So NRV can be calculated as per below method:

NRV Formula = Market Value- Transportation Cost – Legal and Registration Cost

NRV = 4-0.5- 0.1

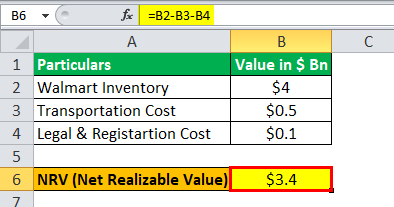

The NRV will be –

Hence with the conservative method, the NRV of Inventory is $3.4 Bn.

Relevance and Use

Net realizable value formula helps compute the net realizable value, which helps entities understand how worthy their assets are. Some of the significance of this value calculated using this formula are as follows:

- The net realizable value (NRV) formula can be used to determine the value of an asset more conservatively. Usually, GAAP requires companies to not overstate the value of an asset that can increase the profit and send some wrong signals to investors.

- NRV also considers the cost of selling in its equation, so NRV comes out to be lower than the market value of an asset.

- NRV is an important metric in the “lower cost or market method of accounting.” In the lower cost or market method, the value of inventory should be shown lesser between the historical cost and the market value in the accounts. If the company cannot determine the market value of inventory, then NRV can be a proxy for the same.

Recommended Articles

This has been a guide to what is Net Realizable Value Formula. We explain it with how to calculate, examples, relevance & a downloadable Excel template. You can learn more about accounting from the following articles –