What is LIFO Liquidation?

LIFO liquidation is an event of selling old inventory stock by companies that follow the LIFO Inventory Costing Method. During such liquidation, the stocks valued at older costs are matched with the latest revenue after-sales, due to which the company reports higher net income, which results in payment of higher taxes.

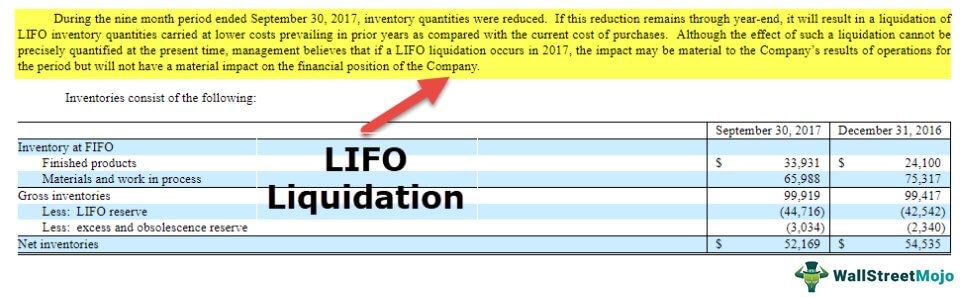

We note from the above SEC Filings; that the company mentions that the inventory quantities were reduced. The carrying cost of the remaining inventory is lower than that of the previous year. If this situation continues for the remaining part of the year, the LIFO liquidation may happen and will impact the results of operations.

Example of LIFO Liquidation

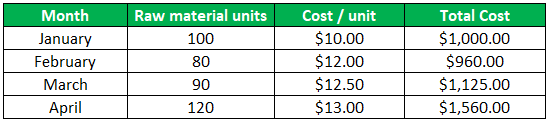

ABC Company manufactures menswear shirts and has the following textile inventory based on periodic cycles:

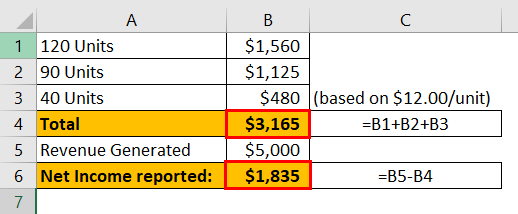

Suppose that ABC has to complete an order of 250 shirts and assume that for each shirt, 1 unit of raw material is used up. ABC will have to liquidate a complete April inventory of 120 units, a March inventory of 90 units, and 40 units from the February inventory to complete the order.

It is known as LIFO Liquidation, where the last in stock is first out, followed by the next layer based on the requirement.

Based on the sales, consider each shirt is sold for $20.00, and the revenue generated is $5,000.00. However, the cost of raw materials is calculated as below:

If all Raw Material was procured in April?

In such a situation wherein the company would have procured all the raw material in April based on the requirement, then below would have been cost and revenue calculations:

raw material cost = $13 x 250 = $3,250/-

In this case, the company would have reported a lower net income.

Here, we note that in the case of such liquidation,

LIFO Liquidation Terminologies

LIFO liquidation has certain terminologies, as mentioned below:

#1 – LIFO layer

Periodic segregation of inventory based on a particular frequency for calculation of closing stocks. This term provides the number of units, cost/unit, the total cost of inventory, etc., for a particular period cycle.

For example,

Inventory during each year is a LIFO layer.

#2 – LIFO Reserve

LIFO is majorly used for reporting purposes. It is the difference between inventory calculated by methods other than LIFO and the inventory calculated per LIFO. Sometimes, companies follow more than inventory management methods for different types of stocks. Hence, there is a difference between actual and LIFO inventory, known as LIFO reserve.

#3 – LIFO Inventory Pool

While LIFO liquidation, inventory may be segregated and pooled together with similar other items (forming groups of items) for better and more realistic calculation. Each group is called a LIFO Inventory Pool.

Advantages

- An increase in sales may indicate an increase in demand for the company’s manufactured product.

- Better than FIFO liquidation, as tax liability reduces due to the increased cost of the latest inventory.

- The movement of older inventory refers to the liquidation of older stocks.

- The LIFO liquidation method is helpful for the movement of perishable items with lesser tax liability in comparison to the FIFO inventory method.

- Aids to the company’s decision to launch a new product as per market demands and change in taste of customers;

- Prior forecast of an increase in potential sales may drive companies to pile up required raw materials at lower costs, to liquidate later when raw material prices rise.

- The LIFO method of inventory system is useful when raw material costs are dynamic and are predicted to rise in the future.

Disadvantages

- Higher tax liability in than the liquidation of stocks procured as per requirement.

- Refers to the company’s lack of analysis on sales and purchase

- It may relate to future financial shortcomings for the company, since liquidation refers to lack of procurement.

- It may refer to a threat to its product acceptance in the market, so the company may decide to liquidate its existing and old stock before new procurement.

- It leads to incorrect calculation of income from sales and hence affects all financial statements and ratios.

Limitations of LIFO Liquidation and Other Similar Techniques

The calculation of profits from pure LIFO liquidation techniques may be misleading towards actual income calculation.

Some companies use the Dollar-value LIFO method for inventory liquidation. As per this method, the current value of the inventory is first discounted to the base layer based on the current inflation rate. Then the real dollar increase is determined, which is then escalated to arrive at the real value of inventory at present (and not the current value based on current cost prices).

With this calculation method, profits that are derived are more practical and realistic.

Important Points

- LIFO liquidation is beneficial when the company has a bullish view of inventory costs. In other cases, the company may foresee an increase in sales.

- It may be forecasted. In such a case, if the raw materials costs are predicted to rise, the company can stock up its raw materials gradually at lower costs and then liquidate later, thus booking higher profits.

- It may be beneficial for short-term profits. However, it may not be practical to be used permanently.

- In general use of this practice (without any planned liquidation), the market may perceive this as the company’s shortfall in funds or lack of analysis of sales, or even financial threats for the company.

Conclusion

Following LIFO liquidation may be tempting to distort the financial statements and evade taxes compared to FIFO inventory; however, it is not treated as the best practice bylaws. There have been various discussions to amend laws around such liquidation so that companies follow more ethical approaches to reporting.

It may be tweaked a little in the form of other similar techniques to give more meaningful data, which can also help better report financial information for the company.

Recommended Articles

This has been a guide to what LIFO liquidation is and its definition. Here we discuss LIFO Liquidation examples and their effect on financial statements, advantages, and disadvantages. You can learn more about accounting from the following articles –