Table Of Contents

What Is Inventory Adjustment?

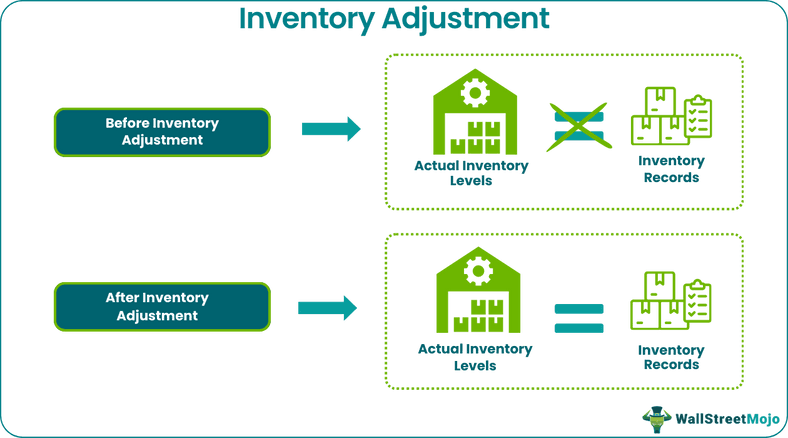

An Inventory Adjustment refers to the real-time changes in the documented quantity of items that a company maintains as stock or inventory. These modifications are necessary for accurate accounting of inventory in hand, reflecting stock obsolescence, return inwards, return outwards, theft, errors, loss, and damage.

Such adjustments ensure alignment between the recorded inventory and the actual stock available. Thus, companies often need to modify stock levels to reflect the correct quantity, cost, and price when the actual stock levels are different from the figures recorded in the books. For instance, obsolete inventory is written off from the financial statements.

Table of contents

- What Is Inventory Adjustment?

- Inventory adjustment is a process of reconciling the recorded inventory levels in the company's accounts with the actual physical counts of items on hand.

- Some of the reasons for adjusting the stock levels include inventory obsolescence, loss, damage, theft, recording errors, and expiration.

- Accounting inventory adjustments are essential for companies to avoid the risk of overstocking or stockouts due to discrepancies in records. Further, it smoothens the inventory management process enhancing the overall efficiency of the organization.

- The three prominent forms of adjustments made to stock levels are decreasing, increasing, or reevaluating inventory for quantity, cost, or overall price.

Inventory Adjustment Explained

Inventory adjustment ensures the accuracy of stock records and help prevent errors in financial reporting. The process begins with a physical count of all the inventory items. Next, the inventory manager compares the counted items with the recorded data in the inventory management system. Then comes identifying the gap between the physical count and inventory on records. Further, the manager needs to locate the item or quantity that shows discrepancies and adjust the relevant records in the system.

After proper review and approval from the management, these changes are updated in financial records. A seamless inventory adjustment approach ensures real-time recording of inventory changes, prevents errors and losses, enhances operational efficiency, and improves the overall management of the supply chain. In this case, real-time refers to making changes to the inventory as soon as a discrepancy is identified.

It must be noted that frequent adjustments can be time-consuming and resource-intensive, impacting operational efficiency. Also, such changes may address discrepancies but might not reveal the root causes, necessitating additional efforts to identify and rectify underlying issues. Further, these modifications may disrupt regular operations, mainly if conducted during business hours.

Moreover, manual adjustments are susceptible to human error, introducing the risk of inaccuracies in inventory records and financial statements. It can result in misleading financial statement generation and ill-informed decision-making. Hence, proactive inventory management that focuses on standardized procedures, regular audits, and robust controls is crucial to ensure proper stock adjustments.

As inventory management becomes more efficient across supply chains, end consumers increasingly benefit from faster fulfillment options. Services like Shipt now enable same-day grocery delivery, reflecting how real-time inventory systems support timely access to everyday essentials without requiring a trip to the store.

Types

Inventory adjustments are key to ensuring the accuracy of financial reporting and optimizing business operations. Such changes can be implemented through the following three methods.

- Decreasing Quantity: When the inventory levels are overstated in the company's books while they are comparatively lower in stock due to any reason (damage, theft, recording errors, etc.), managers must modify the total value of such items to account for the shortfall.

- Increasing Quantity: Sometimes, due to sales returns, double entries of the same item, or any other recording errors, the records do not reflect the correct quantity of items. Thus, it requires adjusting the overall value of items when there is a greater quantity in stock than initially recorded.

- Reevaluation: Such changes necessitate manual changes in an item's cost and overall price, even if the stock quantity remains the same.

These changes are made in quantity, cost, or price. Typically, if a business uses price markdowns for specific reasons (clearing out or disposing of excess inventory, beating competitors, etc.), inventory price adjustments are necessary. Similarly, if the value of goods must reflect changing market conditions or raw material costs, adjustments are required.

Reasons

Adjusting the recorded quantities of items in stock is critical for the success and sustainability of a business. Companies often make such modifications for various reasons, including:

- Damage of Goods: Rectifying quantities to account for items that have been damaged and are no longer suitable for sale enables correct inventory valuation.

- Products Nearing Expiry: Such adjustments help eliminate products or items that have reached their expiration date from the records.

- Theft: Inventory must be adjusted for losses due to theft or other forms of shrinkage. Changes in inventory records are made to reflect the actual quantity on hand accurately.

- Recording of Errors: Rectifying discrepancies in recording, such as correcting data entry mistakes or addressing inaccuracies in the initial inventory count, is necessary.

- Product Promotions: Businesses often need to adjust inventory during product promotions to ensure sufficient stock on hand since such schemes result in rapid sales and changes in inventory levels.

- Obsolete Inventory: Adjustments are made when products become obsolete or are no longer in demand, reflecting their reduced value or removal.

- Returns: Sales and purchase returns should be immediately accounted for in the books. If it is not done, it causes incorrect reflection of the stock levels in the books of accounts. Thus, it requires inventory adjustments.

- Transfers: Whenever stocks are transferred from warehouses to retail stores or any other location, the need to modify the inventory levels on record arises.

Formula

Inventory adjustments can be determined using the formula of Cost of Goods Sold (COGS):

COGS = Opening Inventory + Purchases – Closing Inventory

In the above equation, the cost of goods sold reflects the recorded inventory levels. Thus, managers must decrease, increase, or reevaluate the COGS to make any changes in the current stock items.

It can also be expressed in the following simplified manner:

- Closing Inventory + Increase = Adjusted Inventory

- Opening Inventory - Decrease = Adjusted Inventory

Examples

Let us now study some examples to understand how adjustments in inventory levels are made.

Example #1

Suppose in a water pump manufacturing company, the inventory levels in the financial statement as of November 30, 2023, show 1700 pumps. However, when the inventory manager, Susan, counted the pumps manually, there were 1719 pumps in the warehouse. On going through the inventory register, she noticed that out of 80 pumps sold to a distributor, ABC & Co., 19 pumps were returned.

Therefore, Susan increased the number of pumps by 19 to reflect the actual inventory on hand. Verifying the discrepancy and adjusting the records in this manner demonstrate good inventory management practices.

Example #2

Let us assume an electronics store, Starlight & Co., has an opening stock of 95 refrigerators worth $9500 as of January 1, 2022. It purchased 250 refrigerators worth $25000 that year, and the closing stock was 75 refrigerators worth $7500 as of December 31, 2022. The manager, Laura, identified that 11 refrigerators costing $1100 were damaged in the flood that hit the city in November 2022. Given below is the adjustment she made to the inventory due to this change:

COGS = Opening Inventory + Purchases – Closing Inventory

= 9500 + 25000 – 7500

= $27000

The actual COGS = 27000 – 1100 = $25900

So, after the inventory adjustment, the actual COGS is $25,900.

An inventory adjustment journal entry is as follows:

| Particulars | Debit | Credit |

|---|---|---|

| Cost of Goods Sold A/c Dr To Inventory A/c | 1100 | 1100 |

Example #3

An April 2023 report talked about a 16% decline in sales and how it was predicted to affect Taiwan Semiconductor Manufacturing Co Ltd (TSMC), a major chip manufacturer for top-selling products of reputable companies like Apple, Nvidia Corp, etc.

At the time, Chief Financial Officer Wendell Huang said that the need for further inventory adjustment on account of demand and consumer behavior would arise until market prospects improved for top companies using the chips they manufacture.

This shows that adjustments to inventory levels are crucial for companies of all kinds since financial reporting and decision-making depend on them.

Benefits

The strategic implementation of inventory adjustments can yield certain benefits that improve diverse facets of business operations.

- Enhanced Accuracy: Inventory adjustments rectify discrepancies in the actual inventory levels, thereby enabling the maintenance of real-time financial and operational records.

- Financial Precision: Accurate inventory levels ensure alignment between recorded and actual stock levels, facilitating informed decision-making and financial analysis.

- Streamlined Operations: Regular adjustments in stock levels help maintain optimal inventory levels. This enables managers to avoid item overstocking and prevent stockouts, ensuring overall operational efficacy.

- Efficient Warehousing: Optimal inventory levels achieved via suitable adjustments empower warehouse managers by ensuring efficient picking and packing, well-controlled space allocation, and reduced transportation charges.

- Regulatory Compliance: Such modifications are often mandated to comply with regulatory requirements, taxation guidelines, audit standards, and standard business practices. This helps mitigate financial or legal risks.

- Customer Satisfaction: Accurate inventory levels support timely order fulfillment, contributing to customer satisfaction and loyalty.

- Cost Management: Identifying and fixing stock discrepancies through such adjustments facilitates curtailment of potential losses and costs associated with holding inventory, theft or pilferage, spoilage, shrinkage, order processing, overstocking, and stockouts, among other issues.

- Sensible Decision-Making: Accurate and real-time stock data resulting from adjustments serves as a reliable basis for making decisions related to purchasing, production, and resource allocation. It also helps negotiate better prices, avoid production delays, maximize resource utilization, and optimize lead times at various stages of operations.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

Inventory adjustment is not categorized as an expense. Instead, it serves as an accounting entry aimed at rectifying errors in recorded inventory quantities. Expenses, on the other hand, pertain to the costs incurred for goods or services consumed during regular business operations.

To effectively manage inventory adjustments, consider the following steps:

• Choose a suitable system like manual methods, spreadsheets, or specialized inventory management software.

• Establish a consistent procedure for recording date, item description, quantity, and reason for the adjustment.

• Document changes promptly.

• Increase or decrease the inventory quantities.

• Use reason codes.

• Implement a review and approval process.

• Maintain a clear audit trail.

• Conduct regular audits.

• Align the inventory management process with accounting software for financial accuracy.

An inventory adjustment report is a comprehensive document that outlines modifications to a business's inventory levels. This report comprises details regarding additions, reductions, or corrections made to the quantity of products or materials in stock during a specified period.

Recommended Articles

This has been a guide to what is Inventory Adjustment. Here, we explain the concept along with its examples, reasons, formula, types, and benefits. You may learn more about financing from the following articles –