Differences Between FIFO and LIFO

FIFO (First In, First Out) and LIFO (Last In, First Out) are two accounting methods for the value of inventory held by the company. By accounting for the value of the inventory, it becomes practicable to report the cost of goods sold or any inventory-related expenses on the profit and loss statement and to report the value of the inventory of any kind on the balance sheet.

In this article, we look at what is LIFO and FIFO, examples, advantages and its key differences –

Definitions of FIFO and LIFO methods

What is FIFO (first in first out)?

FIFO stands for ‘First In First Out, ‘which implies that the inventory added to the stock will be removed from stock first. So the inventory will leave the stock in order the same way it was added to the stock.

It means that whenever the inventory is reported as sold (either after conversion to finished goods or as it is), its cost will be equal to the cost of the oldest inventory present in the stock.

It, in turn, means the cost of inventory sold as reported on the profit and loss statement will be taken as that of the oldest inventory present in the stock. On the other hand, on the Balance Sheet, the cost of the inventory still in stock will be taken equal to the cost of the latest inventory added to the stock.

FIFO vs. LIFO Video

What is LIFO (last in first out)?

LIFO stands for Last In, First Out, which implies that the inventory added last to the stock will be removed from the stock first. So the inventory will leave the stock in an order reverse of that in which it was added to the stock.

It means that whenever the inventory is reported as sold (either after conversion to finished goods or as it is), its cost will equal the cost of the latest inventory added to the stock.

This, in turn, means that the cost of inventory sold as reported on the Profit and Loss Statement will be taken as that of the latest inventory added to the stock. On the other hand, on the Balance Sheet, the inventory cost still in stock will equal the cost of the oldest inventory present in the stock.

Both these methods are pure methods of accounting for and reporting inventory value. Whichever method is adopted, it does not govern the addition or removal of inventory from the stock for further processing or selling.

Another inventory cost accounting method that is also widely used by both public vs. private companies is the Average Cost method. This method takes the middle path between FIFO and LIFO by taking the weighted average of all units available in the stock during the accounting period and then uses that average cost to determine the value of COGS and ending inventory.

But in this article, our focus is only on the FIFO and LIFO methods of inventory cost accounting and the comparison between the two.

LIFO vs. FIFO Example

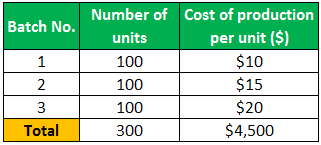

Suppose that a company produces and sells its product in batches of 100 units. If inflation is positive, the cost of production will increase with time. So assume that 1 batch of 100 units is produced within each period, and the cost of production increases after each successive period.

So if the cost of production for producing 1 unit is $ 10 in the first period, it could be $ 15 in the second period, $ 20 in the second period, and so on. Refer to the table below for the summary:

Consider the details about the three batches of production given in the above table. Suppose the batch numbers are in order of date of production of the batches.

The company won’t be able to sell exactly 100 units of products during each period. It will have to sell them as per the orders it receives and the availability of the products in its stock of finished goods. So suppose that the company gets orders of 150 units after producing the 3rd batch of 100 units.

Inventory Valuation using the FIFO method

If a company chooses to use the FIFO method of inventory accounting, the cost of goods sold will be equal to the cost of the first 150 units produced (remember “first in, first out”?) out of all the 300 units available in the stock. The first 150 units produced now include the 100 units of Batch No. 1 plus any 50 Batch No. 2. Hence, the Cost of Goods Sold (COGS) will be equal to (100 * $ 10) + (50 * $ 15) = $ 1750.

Also, the value of the remaining inventory of the finished products will be equal to the cost of the remaining 150 units in the stock, i.e., the remaining 50 units of Batch No. 2 and the 100 units of Batch No. 3. Hence, the value of the inventory of finished goods reported on the company’s Balance Sheet would be equal to (50 * $ 15) + (100 * $ 20) = $ 2750.

Inventory Valuation using the LIFO method

If a company chooses to use the LIFO method of inventory accounting, the cost of goods sold will be equal to the cost of the last 150 units produced (remember “last in first out”?) out of all the 300 units available in the stock. The last 150 units produced now include the 100 units of Batch No. 3 plus any 50 Batch No. 2. Hence, the Cost of Goods Sold (COGS) will be equal to (100 * $ 20) + (50 * $ 15) = $ 2750.

Also, the value of the remaining inventory of the finished products will be equal to the cost of the remaining 150 units in the stock, i.e., the remaining 50 units of Batch No. 2 and the 100 units of Batch No. 1. Hence, the value of the inventory of finished goods reported on the company’s Balance Sheet would be equal to (50 * $ 15) + (100 * $ 10) = $ 1750.

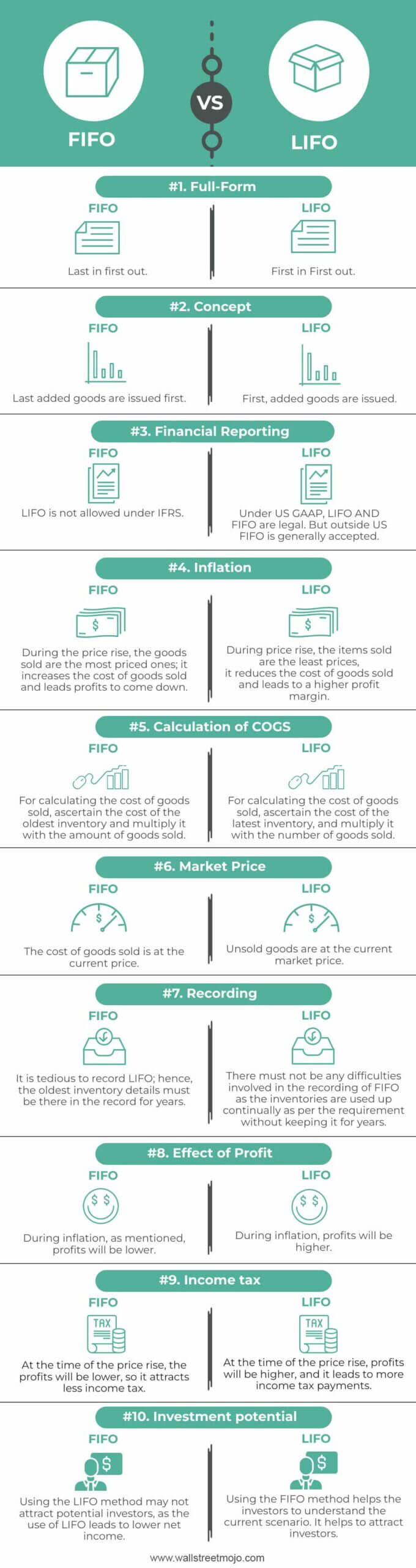

FLFO vs. LIFO Infographics

Why is there more than one method for inventory cost accounting?

The root cause why there is more than one method to account for the cost of inventory is inflation. If inflation ceases to exist, we won’t require different methods to determine the value of inventory company expenses or keep them in its warehouses.

If inflation is not there, the cost of material purchased today would be exactly equal to that purchased last year. So the material cost going into the production of finished goods will also be the same for a particular type of product. So the cost of the inventory added to the stock today will be exactly equal to the cost of the inventory added to the stock one year ago. Hence, whether you use the LIFO method or FIFO method, the value of the inventory expensed or even that in stock will also come out to be the same.

But since inflation is a reality, the inventory value comes out to be something when we use FIFO, and it comes out to be something else when we use LIFO.

Still, why do some companies use FIFO while some use LIFO to calculate inventory value? The answer to this is this: Companies use different methods of inventory accounting for the benefits and convenience offered by both methods in different situations.

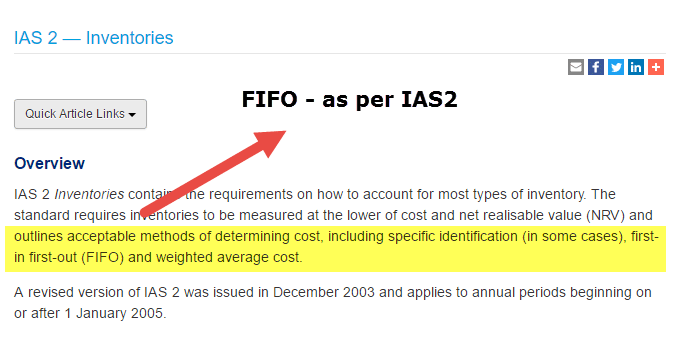

While the above is true, in most countries, the IFRS accounting standards are followed, which do not allow the usage of the LIFO method. So there the companies do not have that choice.

source: iasplus.com

But in the US, it is allowed that publicly traded entities that use LIFO for taxation purposes must also use LIFO for financial reporting also.

Also, look at IFRS vs. US GAAP.

LIFO vs. FIFO – Which is preferred?

The inventory value appears on the Income Statement as Cost of Goods Sold (COGS) and on the Balance Sheet as Inventory under Current Assets. Thus the method used for inventory valuation will indirectly affect the value of Gross Income, Net Income, Income Tax on the Income Statement, Current Assets, and Total Assets on the Balance Sheet.

To understand this, let’s take the values of Cost of Goods Sold (COGS) and that of the inventory calculated using both the FIFO and the LIFO methods from the illustrative example discussed above.

Key Differences

- In LIFO, the goods purchased or produced last are distributed first, and in FIFO, the goods purchased or produced first are distributed first.

- FIFO is the globally and widely used method for inventory valuation. While US GAAP allows adopting LIFO and FIFO, in international scenarios, FIFO is widely used, and IFRS restricts the use of LIFO for inventory valuation.

- Under LIFO, stock in hand represents the oldest stock, while in FIFO, stock in hand represents the latest stock.

- In an inflationary economy, using LIFO leads to lower profit figures and helps in tax savings, while using FIFO leads to higher profit and a huge tax burden.

- FIFO gives the potential investors the exact figure of an organization’s financials and assists in decision making. While LIFO won’t give the exact picture of the financials, this leads to inaccurate investment decisions.

- In FIFO, the closing stock consist of the most recent items, thus closing stock is valued at market price. In LIFO, the closing stock is valued at a historic price.

- FIFO is a more realistic and logical approach to inventory valuation compared to LIFO

- There is a risk of stocks getting obsolete in the case of LIFO, as goods are used from old stock; this risk can be reduced if FIFO is used.

- Unlike LIFO, record maintenance is easier in FIFO, as several layers are less.

- The cost of goods sold is in the current market price in LIFO, and the cost of unsold goods is in the market price in FIFO.

- FIFO is not a suitable method if there is a high fluctuation in material prices. In this case, LIFO is the appropriate option.

Advantages of LIFO

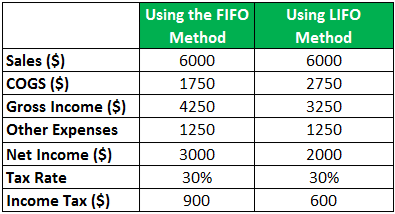

First, take the values of COGS calculated using both the methods and prepare an Income Statement assuming all other values like Sales, Other Expenses, and Tax Rate to be the same for both methods. For assumption, let the selling price of 1 unit be $ 40. Since 150 units were sold, the total sales will be (150 * $ 40) = $ 6000. Also, suppose that the Other Expenses for the period under consideration totaled $ 1250, and the Tax Rate applicable to the Net Income was 30 %. And let these assumed values to be the same for both methods.

The Income Statement prepared when both FIFO and LIFO are used will look like the following:

The value of COGS calculated using the FIFO method was $ 1750, while that calculated using the LIFO method was $ 2750. Now, look at the differences between Gross Income, Net Income, and Income tax values. All of that is due to the difference in the values of COGS, which in turn is due to the use of two different methods of inventory valuation.

So ultimately, the benefit of using the LIFO method for a company is that it can report a lower Net Income and hence defer its tax liabilities during times of high inflation. But at the same time, it might end up disappointing the investors by reporting lower earnings per share. On the other hand, a company that uses the FIFO method will be reporting a higher net income and hence will have a greater amount of tax liability in the near term.

In addition to tax deferment, LIFO is beneficial in lowering the instances of inventory write-downs. Inventory write-downs happen if the inventory has decreased in price below its carrying value. If LIFO is used, only old inventory will remain in stock, and its purchase price will have a lesser chance of going below its carrying value.

Advantages of FIFO

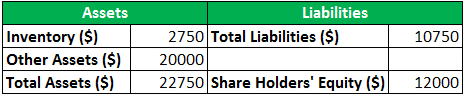

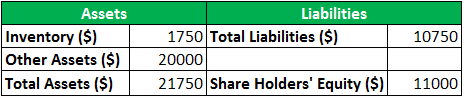

Now, to understand the impact of both the methods on the Balance Sheet, take the values of inventory calculated using both the methods and prepare the Balance Sheet in its simplest form, assuming the values of Other Assets (all assets other than the inventory) and Total Liabilities to be the same for both the methods. For assumption, let the value of Other Assets be $ 20000, and the value of Total Liabilities be $ 10750. And let these assumed values be the same for both methods.

The Balance Sheet prepared when both inventory valuation methods are used will look like the following:

Using the FIFO Method

Using LIFO Method

The value of inventory calculated using the FIFO method was $ 2750, while that calculated using the LIFO method was $ 1750. Now, look at the differences between the values of total assets and shareholders’ equity (=total assets-total liabilities). All of that is due to the difference in inventory values, which in turn is due to the use of two different methods of inventory valuation.

So ultimately, the benefit of using the FIFO method for a company is that it can report a higher value of shareholders’ equity or net worth and hence appear more attractive to the investors. On the other hand, a company that uses the LIFO method will be reporting a lower value of net worth and hence will appear comparatively less attractive to the investors.

It should be obvious to the reader, but it is also noteworthy that the impact on the COGS in the income statement and inventory in the balance sheet will be as described above only if the inflation is positive, i.e., the prices of raw materials are increasing with time. Conversely, if inflation is negative, the impact of LIFO and FIFO will be reversed as described above.

Comparative Table

The crux of the above explanation is summarized in the following table:

| Criteria | LIFO | FIFO |

|---|---|---|

| Full-Form | Last in first out | First in First out |

| Concept | Last added goods are issued first. | First, added goods are issued. |

| Financial Reporting | LIFO is not allowed under IFRS | Under US GAAP, LIFO AND FIFO are legal. But outside US FIFO is generally accepted. |

| Inflation | During the price rise, the goods sold are the most priced ones; it increases the cost of goods sold and leads profits to come down. | During price rise, the items sold are the least prices; it reduces the cost of goods sold and leads to a higher profit margin. |

| Calculation of COGS | For calculating the cost of goods sold, ascertain the cost of the oldest inventory and multiply it with the amount of goods sold. | For calculating the cost of goods sold, ascertain the cost of the latest inventory, and multiply it with the number of goods sold. |

| Market Price | The cost of goods sold is at the current price. | Unsold goods are at the current market price. |

| Recording | It is tedious to record LIFO; hence, the oldest inventory details must be there in the record for years. | There must not be any difficulties involved in the recording of FIFO as the inventories are used up continually as per the requirement without keeping it for years. |

| Effect of Profit | During inflation, as mentioned, profits will be lower. | During inflation, profits will be higher. |

| Income tax | At the time of the price rise, the profits will be lower, so it attracts less income tax. | At the time of the price rise, profits will be higher, and it leads to more income tax payments. |

| Investment potential | Using the LIFO method may not attract potential investors, as the use of LIFO leads to lower net income. | Using the FIFO method helps the investors to understand the current scenario. It helps to attract investors. |

Conclusion

FIFO and LIFO are two methods of accounting and reporting inventory value. FIFO takes the cost of materials purchased first as the cost of goods sold and the cost of materials purchased last as the items still present in the inventory. LIFO takes the cost of materials purchased most recently as the cost of goods sold and the cost of materials purchased first as the items still present in the inventory.

The benefits of using the LIFO method are that it helps defer tax and lower inventory write-downs during periods of high inflation. In addition, the benefit of using FIFO is that it results in a higher value of reported earnings and the company’s Net Worth attracting more investors. However, these effects are the opposite when there is deflation.

But in most countries, the IFRS standard is enforced under which using LIFO is not allowed. Only a few countries, including the US, allow the usage of LIFO for taxation purposes but also require its usage while reporting the results to the investors. However, FIFO is a much more popular method out of the two because of being more logical for most industries.

Recommended Articles

This article has been a guide to FIFO vs. LIFO. Here we discuss the top differences between FIFO and LIFO and the examples, advantages, and disadvantages. You may also have a look at the following articles –