Written byAshish Kumar SrivastavAshish Kumar SrivastavEditorial HeadAshish, a seasoned finance professional, content editor, and blogger, brings over a decade of expertise. As Editorial Head at WallStreetMojo, he mentors writers and ensures quality. A self-published author and with a passion for financial literacy, Ashish's extensive knowledge covers investment banking,12+ years of experienceM.Sc.Investment bankingView Full Profile

Reviewed byDheeraj Vaidya, CFA, FRMDheeraj Vaidya, CFA, FRMContent Reviewer & Course DirectorDheeraj is a former J.P. Morgan and CLSA Equity Analyst with nearly two decades of experience in financial modeling, valuation, equity research, and corporate finance. He specializes in helping students and professionals develop practical and in-demand finance skills through structured and AI-powered,20+ Years of experienceCFA, FRM, IIT Delhi, IIM LucknowFinancial ModelingView Full Profile

Stock Accounting refers to recording the transaction entered into by the business enterprise from the point of investments made by anyone, i.e., whether a body corporate or individual in the company, in exchange for an issue of something in return that could be easily traded in the open market.

It is an important practice from the point of view of any business, but it depends on the rules and laws of the country as well as the accounting standards followed there. Professionals are often engaged in such types of work because they have specialized knowledge and latest accounting software to ensure that the process is done properly.

Stock Accounting Explained

Stock accounting refers to the methods of accounting and tracking the stocks in an organization. Stock Accounting is simply a grouped or compiled form of all the transactions which were transacted over a set period, whether they are economical or not of the stock of the company, which we can easily compare with the records to analyze the funds raised and their utilization for the sake of earning maximum possible benefits thereupon.

The common stock accounting can be related to the shares issued by the company to the general public for the purpose of raising capital to meet business needs. However the investors who subscribe to such stock get an ownership right in the company and have a say in various management decisions.

Every business needs funds to operate its business effectively. So to manage such funds, some businesses choose the option of issuing stocks in the open market. They raise funds by allotment of stock against the money received from the investors.

After that, the process of stock accounting entries for receiving the money from the public and issuing them the stock certificate is known as Stock Accounting.

Types

Now let us look at the various types of common stock accounting in the financial market that needs to be accounted for in the books of the company.

The first type includes share certificates issues to the general investors. The company issues stocks against cash. I.e., the company will receive cash, and the investor will receive a stock certificate. The company does this in order to raise funds to meet its operational requirements, make investments to earn return or plan for growth and expansion. The investors purchase shares with the expectation of getting returns in the form of dividends or trade them in the secondary market to earn profit.

In this option, stocks were issued for consideration other than cash. i.e., issuing stock for taking some services, etc. . This is also for the company’s benefit but in return the benefit provider gets a part of the company’s ownership in the form of stocks.

The last type is issuing stock for purchasing some existing stock issued in the market. In other words, to repurchase the stock issued earlier, new stock is going to be an issue.

Accounting Entries

As discussed above, there are three types of stock accounting entries for which we have to pass the recording entries, which are as follows:

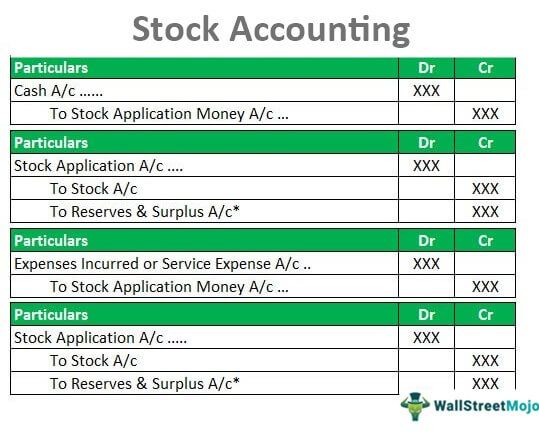

#1 – Where Stocks are Issued for Cash

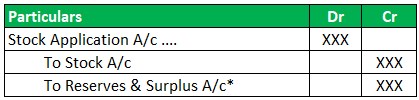

In the case where the common or preferred stock accounting are for stocks that are issued for cash, then to record the transaction following two entries need to be journalized in the books of accounts:

#2 – Where Stocks are Issued for Consideration Other than Cash

In a case where stocks are issued for consideration other than cash, then to record the transaction following two entries need to be journalized in the books of accounts:

#3 – Where Stocks are Issued for Purchasing Our Stock

In a case where stocks are issued for purchasing our stock issued earlier, then the trading stock accounting is done with the help of the following entry that needs to be journalized in the books of accounts:

Example

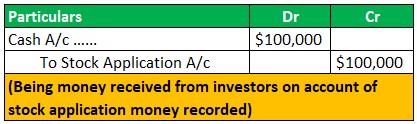

Let us understand the recording of stock with an example, company A wants to issue stock amounting to $100,000 comprising of 10,000 stocks of $10 each on 01.04.2020 and to issue stock certificates to the applicants on 10.04.2020, then record such transaction in the books of accounts following entries are to be passed:

On date 01.04.2020:

Then on date 10.04.2020, to allow the stock applied entry would be:

Benefits

Just as every activity at various levels of the organization has its own benefits and limitations, the different methods of common or preferred stock accounting also have them. Let us first try to understand the benefits of the same.

#1 – Helps in decision making of Management

From the information compiled in the stock account, the register management or decision-making team could easily gather the data without making such efforts.

#2 – Helps Management to reconcile and provide data to the lenders as and when required

The Lenders and the management as well need to analyze the financial position of an entity before taking any decision; the proper accounting of stock helps in analyzing the amount which the company has raised by way of stock issuance.

#3 – All Compliances Decisions

The entity earns and declares a dividend to the stockholders; then, they must pay some taxes levied thereupon. To analyze such an amount and promptly comply with the regulatory guidelines, one must observe stock records.

#4 – Goodwill/ Capital Reserve

When someone wants to take over the business, then for the valuation of goodwill or capital reserve, one needs to analyze the stock accounts as the permission of stockholders is required.

Limitations

Now let us try to understand the limitations of the trading stock accounting.

#1-Subjective

The share valuations may be subjective, especially for companies whose shares are not actively traded in the stock exchange. It is difficult to determine the fair value of the shares which depends on financial performance, market conditions, Again, different valuation methods can give different results.

#2 – Market volatility

Due to market fluctuations resulting from economic and political unrest, natural disasters, investor sentiments, etc, the market value of shares keep on changing, and recording them may lead to fluctuations in the net income and the shareholder’s equity.

#3 – Difference in time

There may be difference of time gap between when the financial transactions are occurring and when they are being recoded, leading to complications in the accuracy and comparability.

#4- Types of shares

The company may issue different types of stocks, like common share, preferred shares, convertible shares, etc, which have different methods of accounting.

#5- Reporting requirements

The organization must follow the requirements set down by the Securities and Exchange Commission(SEC) in the US or the International Financial Reporting Standarrds(IFRC) which invove complex rules, and diaclosur requirements.

#6- Difference across borders

Different jurisdiction may follow different methods of accounting standards and regulations. This reduces the comparability and consistency.

Thus the above are some of the limitations of the system

Recommended Articles

This article has guide to what is Stock Accounting. We explain the accounting entries, types along with examples, benefits & limitations. You may learn more about financing from the following articles –