Part of our Financial Statement Analysis guide

What Are Ratio Analysis Limitations?

Ratio Analysis Limitations refer to the restrictions taken into consideration while computing the ratio analysis. It only considers quantitative aspects and fully ignores the qualitative aspects, it does not take into consideration the reasons for fluctuation of amounts due to which results may not be appropriate, and it only shows the comparison or trend, actions have to be taken afterward by management based on an analysis of ratios.

Ratio Analysis is one of the most commonly used tools for the analysis of Financial Statements. It helps depict the most critical financial parameters of the business at a glance. However, despite being such a popular and useful technique for the interpretation of Financial Statements, Ratio Analysis has its own set of limitations.

- Ratio analysis has limitations as it solely focuses on quantitative factors and overlooks qualitative aspects. Management must carefully scrutinize ratios and investigate reasons for fluctuations before making decisions.

- While ratio analysis is crucial for assessing a company’s financial statements, it’s equally important to consider qualitative factors that impact the company’s performance.

- The accuracy of ratio analysis relies on the quality of financial statements. If the financial statements are manipulated, it can lead to inaccurate business analysis, highlighting the significance of reliable and transparent financial reporting.

Ratio Analysis Limitations Explained

Ratio analysis limitations, when listed, refer to the lists of factors that restrict the ratio analysis computations in some way. These restrictions tell one about how and where the ratio analysis calculations can go wrong.

Ratio Analysis is based on the Financial Statements prepared by the company. They consider only the quantitative side of the business and completely ignore the qualitative factors of the business, which are equally important. Furthermore, the quality of Financial Statements determines the accuracy of Ratio Analysis. Suppose the financial statements are manipulated by the business or presented to show a better position than the actual (also Known as ‘Window Dressing‘). Any ratios computed on such Business Financials will also result in an incorrect analysis of the business.

Ratio analysis is one of the most significant metrics that help evaluate the financial state of a business. It helps businesses compare themselves with their competitors. As a result, they learn about the loopholes and work on them to improve their market position.

The ratio analysis is a vital valuation parameter for both the management of the businesses and their investors. Based on the analysis of different ratios that a firm calculates and presents in its financial statements, the investors decide whether to invest in a firm’s asset or not. In addition, it guides the management of the companies to assess their strategies and check if they are good to go in the current business scenario. If required, the management transforms startegies for betterment and improvement.

The role that ratio analysis plays in helping the businesses assess their current position and make comparisons with peers, it is important to ensure that the computations are correct with respect to the limitations that calculations involve.

Ratio Analysis Explained in Video

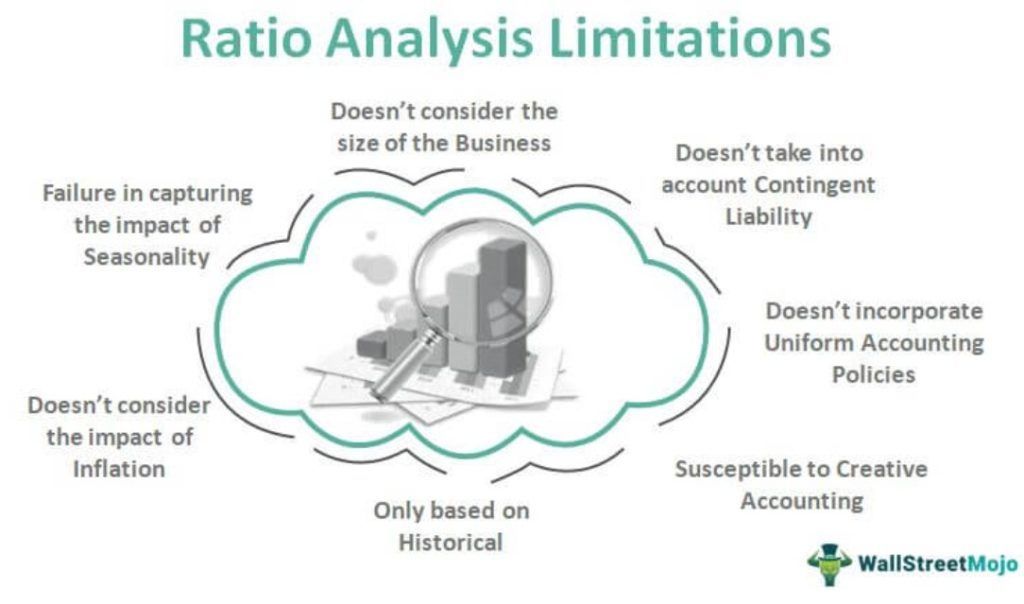

Top 10 Ratio Analysis Limitations

Understanding the restriction of ratio analysis can help companies know the factors that influence the ratio analyses that they conduct. Hence, the firms remain prepared to face unexpected outcome, given the ignorance of certain factors.

The top 10 limitations that one must know of are as follows:

#1 – Doesn’t consider the size of the Business

- Ratio Analysis diverts the attention of the intended user from the figures and financial statements of the business as they don’t consider the size of the business and the resultant bargaining power and economies of scale that a large business enjoys compared to a Small business. It doesn’t consider such factors that have an impact on the Company’s performance.

#2 – Doesn’t take into account Contingent Liability

- Another limitation of Ratio Analysis is that it doesn’t consider any contingent liability. A contingent liability depends on some external factors that may or may not happen, such as Litigation matters, etc.

- If they result in an adverse outcome for the business, such events will have serious repercussions on the company’s financials. Still, Ratio Analysis doesn’t consider this, although such Contingent Liabilities may have a material impact on the company’s Financial Position.

#3 – Doesn’t incorporate Uniform Accounting Policies

- Ratio Analysis doesn’t incorporate the impact of Accounting policies adopted by the business in recognizing Income and Expenses. The resultant comparison between the companies based on Ratio Analysis will be biased and will not exhibit the true comparison between the companies.

- For instance, Companies reporting depreciation based on the Straight Line Method will report different Net Profits, and Companies reporting depreciation based on the Declining Balance Method will report a different Net profit. Similarly, Companies exposed to currency movements will be impacted differently, but Ratio Analysis will not be able to capture the same in Financial Statements.

# 4 – Susceptible to Creative Accounting

- Financial Statements can be distorted by the companies using Creative Accounting. Accounting Policies adopted by the companies have a material impact on Ratio Analysis. A company may opt for an Exceptional Income (Non-Recurring Income) as a part of its Revenue. It may declassify a Business Expenditure into a Non-recurring Expenditure, which can materially impact its Financial Statements and the resultant Ratio Analysis. By choosing such accounting policies, businesses deliberately abuse the subjectivity inherent in Accounting, which tends to bias the figures in the direction opted by the management.

- Ratio Analysis becomes incomparable if there is a significant change in the accounting procedures and policies adopted by the business. For instance, a company shifting from the LIFO Inventory method of Valuation to the FIFO method of Inventory Valuation will observe a significant variation in its profitability and Liquidity ratios during Inflationary periods and vice versa, which will make the trend analysis exercise futile.

#5 – Cannot use to compare different industries

- Another limitation is that it is not standardized for all industries. Different businesses operating in different Industries are difficult to interpret based on the standard Ratio Analysis. For instance, companies operating in Real Estate will have a very low Return on Capital Employed (ROCE) as the assets held by such companies are updated regularly, which increases the amount of capital employed; however, there are certain Industries where assets are not required to be revalued at such frequency which makes it very difficult to compare based on Ratio Analysis.

- Ratio Analysis standards are not the same across industries, and it isn’t easy to compare companies based purely on their Standard Financial Ratios. For instance, a company in the Trading business may have a Current Ratio of 3:1 might appear to be excellent compared to a company in Real Estate with a Current Ratio of maybe 1:1 as ratio Analysis doesn’t take into consideration the particular dynamics of the business and Industry to which the companies relate to.

#6 – Only based on Historicals

- Another limitation is that it is based on historical figures reported by the business and, as such, predicts that the history will repeat itself, which may or may not be the case. Also, such figures are irrelevant when a business has changed its business model or entered into a different line of business.

#7 – Doesn’t consider the impact of Inflation

- Ratio Analysis doesn’t incorporate the impact of Price rise, i.e., Inflation. If an increase in Sales is purely on account of Inflation, Revenues of the business would appear to have increased over the previous year when, in fact, the Revenues would have remained constant in real terms.

#8 – Doesn’t Consider Impact of Market Conditions

- Ratio Analysis doesn’t incorporate the impact of the market conditions on business performance. For instance, an increase in the Company’s Outstanding Debt Receivables during an economic boom cycle when sales increase will be considered bad compared to a recessionary period.

#9 – Failure in capturing the impact of Seasonality

- Another limitation is its failure to capture seasonality. Seasonality factors impact many businesses, and Ratio Analysis fails to factor the same resulting in a false interpretation of such a Ratio Analysis.

- For instance, a company operating in Woollen garments will observe sudden Inventory levels before the Winter Season as large production is done in advance to meet the supply of Woollen garments in peak season. Compared with other months, such Inventory levels will show an unlikely spike in Inventory levels if seasonal factors are not taken into consideration, which Ratio Analysis fails to undertake on its own.

#10 – Considers the position of the business on a particular date

- Ratio Analysis uses Balance Sheet values, which are the position of the business on a particular date, and most of the values are shown at the Historical Cost and Income Statement, which shows the performance for the whole year at the current cost.

- Analyzing such ratios can create a lot of disparity among the intended users.

Frequently Asked Questions (FAQs)

1. What are the main limitations of ratio analysis as a tool for financial evaluation?

Ratio analysis has limitations as it relies solely on historical financial data, may not capture qualitative factors, and does not account for external economic factors. Additionally, differences in accounting policies and practices between companies can affect the comparability of ratios.

2. Can ratio analysis alone provide a complete picture of a company’s financial health?

While ratio analysis is a valuable tool, it cannot provide a complete picture of a company’s financial health on its own. It should be complemented with other financial metrics, qualitative analysis, and a thorough understanding of the industry and economic conditions for a more comprehensive evaluation.

3. Can ratio analysis provide insights into a company’s long-term sustainability?

Ratio analysis can offer some insights into a company’s long-term sustainability by assessing profitability, solvency, and efficiency. However, it may not account for factors like innovation, market trends, and management’s strategic decisions that significantly affect a company’s long-term success. A broader analysis is necessary to evaluate long-term sustainability.

Recommended Articles

This article has been a guide to what are Ratio Analysis Limitations. Here, we explain the concept along with discussing the list of top 10 limitations. You may learn more about Ratio Analysis from the following articles –