What is Errors and Omission Insurance?

Errors and Omission insurance is a kind of insurance wherein a professional and the company are insured from the liability that may arise due to the claims made against them about inadequate or incorrect work or negligence in work done. Thus, it is an insurance that provides indemnity against claims arising because of professional misconduct or negligence.

It is of great importance for the professionals and the companies to avail errors and omission insurance coverage claims as the same can protect them against huge liabilities that may build up due to lawsuits by the clients on account of neglect done by professionals in their work towards the client.

Errors And Omission Insurance Explained

Errors and omission insurance protects the professionals and the companies from client claims against the professionals independent or associated with companies providing advice or consultancy in the capacity of a lawyer, financial advisor, etc., to the clients.

If the client, owing to errors or omissions on the part of the professional, incurs a financial loss, may file a claim against such professional or the company who engaged such professional. Having such insurance will protect the professional or the company against the full liability of the claim.

Incurring the errors and omission insurance price is particularly crucial for individuals and companies that provide services or advice to clients, such as consultants, lawyers, accountants, real estate agents, and insurance agents.

E&O insurance provides financial protection in situations where a client alleges that the professional’s services or advice resulted in financial loss, damage, or harm. This could include claims of negligence, errors in judgment, failure to perform services as promised, or other professional mistakes. Without E&O insurance, professionals may be personally liable for legal defense costs, settlement payments, or court-ordered damages, which could have significant financial consequences and reputational damage.

The coverage provided by E&O insurance typically includes legal defense costs, settlements, and judgments associated with covered claims up to the policy limits. Policies may also include coverage for defense costs incurred during regulatory investigations or disciplinary proceedings. Additionally, E&O insurance can offer peace of mind to professionals and businesses by helping to safeguard their assets and reputation in the event of a lawsuit or claim.

It is essential for professionals to carefully review their E&O insurance policies to understand the scope of coverage, exclusions, deductibles, and policy limits. Coverage requirements may vary depending on the industry, the nature of services provided, and regulatory requirements.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

Features

Let us understand the features of errors and omission insurance coverage through the points below.

- It is a kind of liability insurance.

- It protects the professionals and companies who have engaged them against the damages awarded in a lawsuit against such professionals in respect of the lawsuit filed by the client due to the professional’s negligence in carrying out the assignment.

- The insurance does not cover criminal liabilities or other certain liabilities kept out of the scope of the insurance agreement.

- Insurance coverage includes costs concerning courts and any settlement amount as may be provided in the insurance agreement.

Examples

Let us now touch upon the practicality of the concept of errors and omission price through the examples below.

Example #1

A mortgage broker agreed with his client to undertake certain mortgages on account of his client, the lender. However, the mortgages undertaken by the mortgage broker went into default, as a result of which the lender suffered losses when one sold the said properties. The client, being aggrieved, filed suit against the mortgage broker (professional) on account of the incapability of the mortgage broker to correctly evaluate the ability of the borrower in repayment of mortgage loans and also for incorrectly evaluating the value of underlying properties.

Example #2

Travelers Casualty Insurance Co. was not obligated to defend or indemnify CBIZ Borden-Perlman Insurance Agency, Inc. (B-P), in a tort action, as Republic bore the litigation and settlement costs. The U.S. Court of Appeals for the Third Circuit upheld a New Jersey district court’s summary judgment in favor of Travelers.

The ruling aligned with the expectations of insureds possessing both commercial general liability and errors and omissions policies. Errors and omissions policies cover professional service risks, distinct from general business risks covered by general liability policies. B-P, a CBIZ insurance agency in New Jersey, held insurance with Travelers, providing commercial general liability coverage with a financial professional services exclusion, and with Republic, which provided an errors and omissions policy with specific coverage for professional services up to $5,000,000 for every loss and $6,000,000 in aggregate limits.

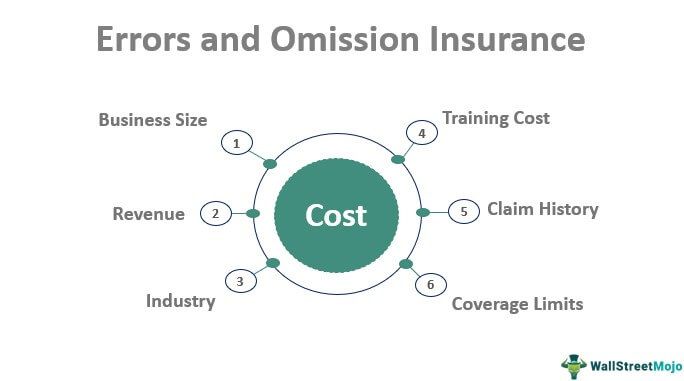

Cost

The errors and omission insurance price depends on many factors discussed in detail hereafter.

- Business Size: A company with many professional employees may be subject to higher risk, and thus, higher costs will be involved.

- Revenue: When a large amount of revenue is involved, it calls for greater investment in insurance as the risk is also high.

- Industry: It can not be denied that insurance needs will be different for different industries. Some professions may have higher chances of error and omission than others.

- Training Cost: The higher the amount is spent on the training of the employees, the less the cost is required for insurance.

- Claim History: A company with a history of suits must pay higher proceeds to the insurance company.

- Coverage Limits: Those insurance arrangements with high coverage limits will be accompanied by higher insurance costs.

Who Can Buy?

Normally, errors and omission insurance coverage is opted for by the following professionals:

- Medical professionals

- Legal professionals

- Finance professionals

- Insurance agents and brokers

- Construction professionals

Needs

Let us understand why professionals and businesses of a certain nature need to invest and understand their errors and omissions in insurance coverage through the discussion below.

It arises because any claim against your business can lead to the risk of heavy losses in your business because of huge liabilities that may arise due to client claims. The losses will be incurred on legal expenses even if the professional persuades the client to withdraw the lawsuit against him later. The claim awarded may be hefty and may cost millions. Having errors and omission insurance will keep the professionals protected from such losses.

Benefits

Incurring errors and omission insurance price ultimately is beneficial since it covers the following costs:

- Lawyer fees

- Court fees

- Administrative expenses such as documentation costs

- Settlement or the judgment claim awarded against professional

Errors and Omissions Insurance vs Professional Liability

Let us understand the distinctions between the errors and omissions insurance coverage and professional liability through the comparison below.

- Professional liability is insurance coverage that protects traditional professionals only, such as physicians, lawyers, etc. However, the term used for quasi-professionals, such as real estate brokers, is errors and omissions insurance.

- Nowadays, insurance companies have started using both terms interchangeably.

Errors and Omissions Insurance Vs Malpractice Insurance

Let us understand the differences between the two concepts through the comparative points below.

E&O Insurance

- E&O insurance provides coverage for professionals and businesses against claims of negligence, errors, omissions, or failure to perform professional services adequately.

- It is commonly purchased by professionals such as consultants, lawyers, accountants, and insurance agents.

- E&O insurance is relevant across various industries and professions where the quality of advice or services provided can result in financial loss or damage to clients.

- Claims covered under E&O insurance may include allegations of professional negligence, mistakes in advice or recommendations, failure to meet contractual obligations or inadequate performance of professional duties.

Malpractice Insurance

- Malpractice insurance is specifically designed for healthcare professionals, including doctors, nurses, dentists, and other medical practitioners.

- It protects against claims of medical negligence, errors, or omissions in diagnosis, treatment, or patient care that result in harm or injury to patients.

- Malpractice insurance may be mandated by law or required for licensure in many healthcare professions to ensure patients have recourse in the event of medical errors or negligence.

- Claims covered by malpractice insurance may include medical errors, misdiagnoses, surgical mistakes, medication errors, or failure to obtain informed consent from patients.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Recommended Articles

This article is a guide to What is Errors and Omission Insurance. Here we discuss the examples features, cost, needs, and compare it with malpractice insurance. You can learn more about it from the following articles: –