What Is Telematics In Insurance?

Telematics in insurance refers to deploying technology and devices to collect and analyze driver behavior, driving patterns, and vehicle usage data. It creates a more accurate and personalized insurance system by assessing risk and setting individualized insurance premiums.

Telematics encourages safe driving practices, as it can lead to lower auto insurance premiums. Insurers can identify high-risk and low-risk drivers and adjust their premiums accordingly. It also enables real-time vehicle tracking, aiding stolen vehicle recovery, roadside assistance, accident investigation, and overall road safety enhancement.

- Telematics in insurance is a data-driven system that utilizes technology to assess risk and establish personalized premiums.

- It offers policyholders tailored insurance premiums, Pay-As-You-Drive (PAYD), Usage-Based Insurance (UBI), fleet management, and advantages for new or young drivers.

- Telematics improves road safety, enhances customer satisfaction, and reduces costs for insurers by providing real-time data on drivers’ efficiency, mileage, and behavior. This data helps insurers create new products and refine underwriting processes.

- While it helps prevent fraud or false insurance claims, it also raises potential privacy concerns among customers due to the constant monitoring of drivers.

Telematics in Insurance Explained

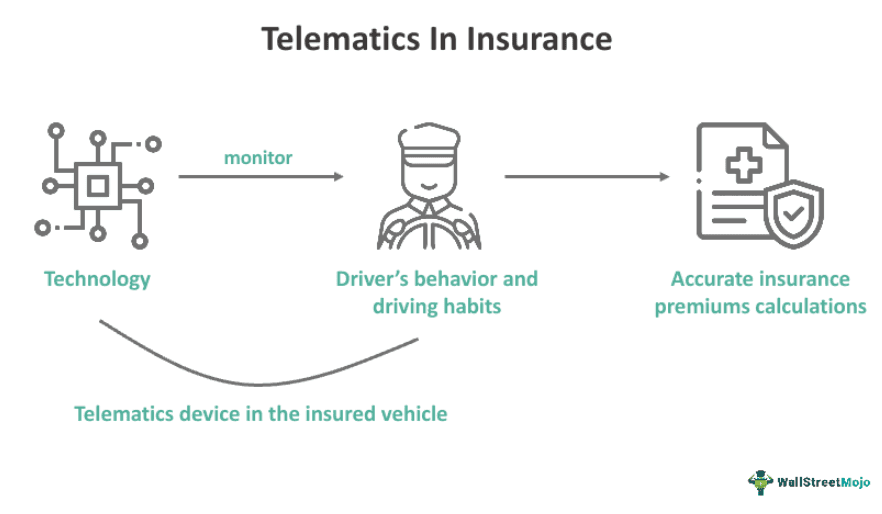

Telematics in insurance can be defined as utilizing the latest technologies, such as GPS(Global Positioning System), sensors, and data analytics, to assess and monitor auto insurance policyholders‘ driving behavior and performance. To implement this, policyholders’ vehicles are equipped with telematics devices, which typically include a combination of accelerometers, onboard diagnostics, and GPS. These devices are attached to the vehicle to collect information about the driver’s behavior.

The collected data includes driving patterns, braking habits, mileage, driving speed, and the time of day for vehicle operation. Telematics data is transmitted to the insurance company using wireless communication, where it is meticulously examined according to predetermined parameters. These parameters help create an accurate driving profile for each policyholder.

Based on the driver profiles, customized insurance premiums are offered. Insurers may also provide feedback and rewards to drivers to encourage safe driving habits. This approach has several implications, such as more accurate risk assessment by insurers, lower premiums for safe drivers, and higher premiums for riskier drivers. Additionally, telematics aids in fraud detection for insurance claims.

Drivers have the opportunity to learn and improve their driving habits, leading to the development of user-based insurance and pay-as-you-drive insurance policies. Usage-based insurance calculates premiums based on individual driver behavior, while pay-as-you-drive calculates premiums in proportion to safe driving habits. This shift from traditional generalized risk factors in insurance to individualized driving risk behavior has led to premiums based on actual driving data, increased competition among insurers, and reduced premium amounts. Ultimately, telematics has contributed to lower road accidents and decreased fraudulent insurance payouts, benefiting insurers and policyholders alike.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

Examples

Let us use a few examples to understand the topic.

Example #1

Imagine John has a small device installed in his car that tracks his driving habits, such as how fast he drives, how smoothly he brakes, and how often he uses his seatbelt. This device sends this data to his insurance company. If it shows that John is a safe driver, he might get a discount on his auto insurance premiums. This is a basic example of how telematics is used in insurance to offer personalized pricing based on his driving behavior.

Example #2

In 2022, General Motors (GM) announced its intention to introduce an algorithm-based auto insurance plan in select U.S. states by the end of the first quarter. Based on telematics in insurance, this plan assessed policyholders’ premiums according to their past driving performance. In partnership with the American Family, GM’s OnStar subsidiary sought regulatory approval for this data-based insurance plan in Arizona, Illinois, and Michigan to receive approval. The company aimed to expand to more states in the future.

GM’s policy didn’t consider driver-assistance systems, but there were plans to incorporate sensor data from systems like “Super Cruise” in future versions. GM had set a goal of generating $6 billion in insurance revenue by 2030. The company collected driving data directly from the vehicle for a more reliable rate setting, offering upfront discounts to safe drivers who opted into data collection.

Uses

Telematics has multiple applications for insurers and policyholders. Let’s discuss these here:

- Tailored Insured Premium: Telematics allows for a customized insurance premium based on the level of risk associated with a driver. Low-risk drivers can secure lower premiums, while high-risk drivers may face higher rates.

- Pay-As-You-Drive (PAYD): This system calculates premiums based on the distance driven by drivers. Those who drive fewer miles can enjoy reduced premium costs.

- Usage-Based Insurance (UBI): Telematics aids in evaluating how a vehicle is used, particularly benefiting commercial vehicles by determining drivers’ risk profiles.

- Fleet Management: Telematics finds application in commercial fleet management by operators. It provides insights into maintenance needs, vehicle performance, and driver behavior, enhancing safety, efficiency, and operational cost management.

- Benefits for New or Young Drivers: New or young drivers can demonstrate their safe driving skills to secure lower premiums on their auto insurance.

Impact

Technology has the potential to influence various aspects of driving and insurance claims. Let’s explore some of the impacts on the insurance sector:

- Road Safety Improvement: By rewarding good driving, telematics has contributed to enhanced road safety. This encourages individuals to drive more cautiously, reducing accident rates and fatalities.

- Satisfaction for Customers and Insurers: Telematics provides real-time data on drivers’ efficiency, mileage, and behavior to insurers, along with offering feedback and rewards to customers. Consequently, this elevates customer satisfaction and benefits insurers.

- Cost Savings: In telematics-based insurance claims, insurers can reduce fraudulent or false claims costs. Additionally, it allows drivers to claim lower premiums based on their driving behavior and mileage.

- Data-Driven Insights: Insurance companies leverage telematics insights to develop new products, reduce operational expenses, and refine the underwriting process.

Advantages And Disadvantages

Here’s a point-by-point assessment of the advantages and disadvantages of telematics:

Advantages

- Helps ensure thwarting fraud or false insurance claims.

- Encourages policyholders to drive safely.

- Helps drivers secure lower premiums from insurers.

- Has the potential to decrease accidents.

- Utilizes a data-driven approach to improve customer satisfaction, product development, and risk assessment.

- Provides insurers with immediate notifications of emergencies or accidents, potentially saving lives.

- Facilitates the creation of customized premiums.

Disadvantages

- Leads to a breach of privacy due to the constant monitoring of drivers.

- Signal interference or device malfunction can affect the accuracy of data recording and transmission.

- Adds to the extra cost of operation for insurers due to the expense of GPS devices.

- Gets limited since real-time GPS data is not available everywhere.

- Many drivers are unfamiliar with technology handling, creating a technological barrier to adoption.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. Why is telematic insurance not gaining popularity among car owners?

Telematic insurance faces resistance from some car owners due to privacy and data collection concerns. Additionally, there’s a perception that it may lead to higher premiums for riskier drivers, deterring adoption among those who fear increased costs.

2. Is telematics in insurance a privacy concern?

Yes, telematics in insurance raises privacy concerns for some individuals. The constant monitoring of driving behavior and data collection can be considered invasive. Striking a balance between improving road safety and respecting privacy rights is challenging for the industry.

3. Is telematics in insurance the future of the industry?

Telematics holds great promise in the insurance industry, as it offers data-driven insights that can improve risk assessment, customer satisfaction, and cost savings. While it may not completely replace traditional insurance models, it will likely play an increasingly significant role in shaping the industry’s future.

Recommended Articles

This article has been a guide to what is Telematics In Insurance. Here, we explain its uses, examples, impact, advantages and disadvantages. You may also find some useful articles here –