What Is a Mortality Table?

A mortality table is a tabular presentation of the rate of death for a specific population over a chosen period. It is also known as a life table or an actuarial table. Since World War II, mathematical formulas have been employed to calculate assured life mortality, pensioner and annuitant mortality, and graduated parts of the English Life Tables.

John Grant and Edmund Halley created the first life tables in 1662. Since then, there has been considerable interest in constructing the “law of mortality,” a mathematical explanation for the gradation of the age pattern of death (1693). French mathematician Abraham De Moivre first presented a reasonably specific law in 1725, and the best-known contribution is from British self-educated mathematician and actuary Benjamin Gompertz (1825).

- The mortality table is the basis for calculating the average life expectancy in a society that provides a view of death mortality rates in a nation. It describes the likelihood that a person will pass away at a specific age or live to a specific age.

- There are two types of mortality tables: The generation life table, also known as the cohort life table, “summarizes the specific mortality rate of a set of people sharing the same age. In contrast, the period life table calculates death rates for a certain population over a specified period.

- Life insurance companies use tables to calculate the average lifespan of individuals, separately for males and females. It is useful in calculating the premium that a person in a specific age group should pay and designing insurance products accordingly.

Mortality Table Explained

Mortality tables represent data derived from the mortality experience of a population during a specific timespan. The spreadsheet-based data effectively shows the possibility of death for each age group within a population.

Since both males and females have different mortality rates, life tables are usually made differently for them. However, life tables can also be combined with other data, such as health records and life expectancy ratios. In addition, various segments are added to differentiate between different types of risks, socio-economic background, kind of employment, health issues, smoking habits, etc.

Insurance companies and asset or liability management companies commonly use it. Insurance companies use it to calculate the cost of individual insurance plans and policies. The statistical tools assist insurance providers with a quick way to calculate at which age a person will pass away. In other words, it essentially states the likelihood that a person of a certain age would pass away in the following year. Furthermore, it helps the insurance industry innovate its products according to data and preferences.

Types

There are two types of mortality tables:

- Period life table: The period life table calculates mortality rates for a particular population over a specified period, such as only one year or a selection of the number of years. It also presupposes that fatality rates will remain the same for the rest of life, so it completely ignores any potential changes or improvements in mortality rates.

- Cohort life table: The cohort life table derives the death rate of individuals who share the same birth year. It displays the likelihood that a member of the specified batch or cohort will pass away at each age. Furthermore, the cohort life table is preferred because it allows examining trends in mortality rates over the years. In the cohort life table, data is produced using data collected up to the current point and predictions of fatalities in the future. It is assumed to be a more adequate and precise indicator of the lifespan of a person of a particular age.

Examples

Let us look at mortality table examples to understand the concept better:

Example 1

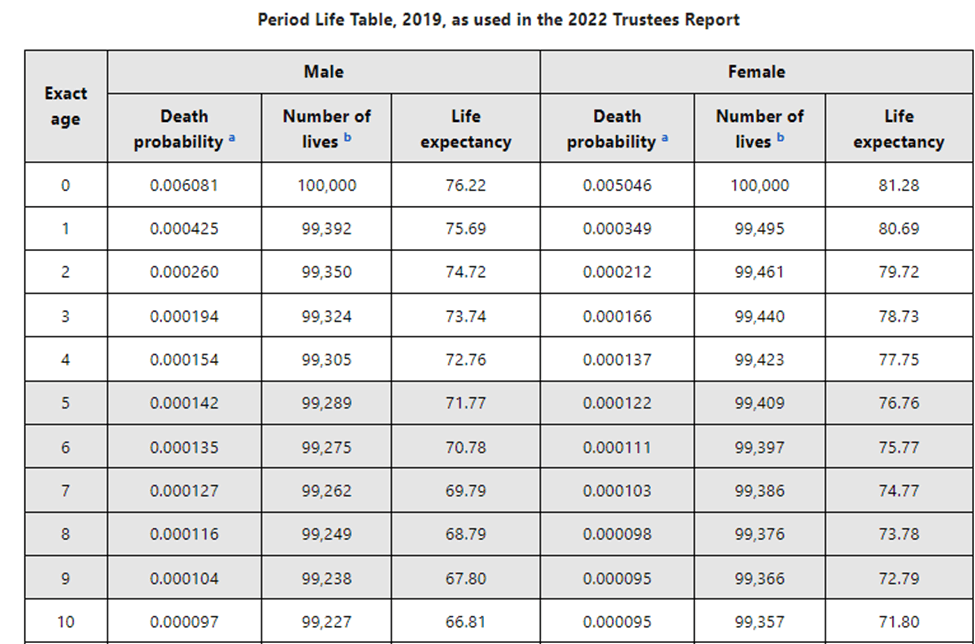

The image listed below is a small section of the 2019 period life table for the Social Security area population (composed of residents of the 50 States and the District of Columbia (adjusted for net census undercount), civilian residents of Puerto Rico, the Virgin Islands, Guam, American Samoa, and the Northern Mariana Islands, Federal civilian employees and persons in the U.S. Armed Forces abroad and their dependents, non-citizens living abroad who are insured for Social Security benefits; and all other U.S. citizens abroad), as used in the 2022 Trustees Report (TR).

Example 2

For life insurance valuations, it is crucial to employ mortality tables that incorporate a prediction of future death patterns. Additionally, it is essential to be aware of the systematic risk associated with using a table that might not accurately predict future mortality and to establish strategies for dealing with it.

Life insurance providers adjust their mortality tables to consider particular risk factors, such as a person’s diabetes, being underweight or overweight, and other health conditions. Consider patients with diabetes as an example. When a person applies for life insurance due to diabetes, the insurance company can estimate how long the applicant might survive by using a mortality table for diabetic patients. Even though it’s not exact data, the mortality table gives them the information they need to decide whether to offer individual coverage, depending on the situation and the amount of insurance coverage.

Importance

For a variety of reasons, mortality tables are essential:

- First, a mortality table generated at the national level by national organizations can be used to compare local or regional mortality rates to national rates, thus contributing to the determination of a standardized mortality ratio and statistical significance.

- Grant, Reed and Merrell, Keyfitz, Greville, and other demographers have created life tables to estimate demographic trends relating to death rates, life expectancy, migration and immigration rates, occupation, etc.

- It is used to calculate the average life expectancy of individuals and create family planning programs that address infant and maternal mortality rates, etc.

Frequently Asked Questions ( FAQs)

What are the components of a mortality table?

It lists the exact age, death probability (probability of dying within one year), number of lives (number of survivors out of 100,000 born alive), and life expectancy of both males and females.

What are the uses of a mortality table?

Primarily it is used to calculate the probability that a person will pass away at a certain age. Furthermore, they offer an overview of current health issues, suggest enduring risk patterns in particular communities, and display trends in particular causes of death over the coming years.

Why do insurers use mortality tables?

A mortality table is a quantitative graph that displays the average life expectancy for each age group and the mortality rate for a specific position. For example, the average amount of time that a group of people of a given age is yet to live is calculated by insurers using a mortality table.

Recommended Articles

This article has been a guide to what is Mortality Table. We explain its types, examples, importance, and application in the insurance industry. You may also find some useful articles here –