What is the Cash Surrender Value?

Cash surrender value is the money that the life insurance policyholder will receive if they withdraw before the completion of the policy or his death. This value is, at times, lower than the maturity value, depending upon the time passed from the date of initiation of the policy till the date of surrendering it.

Cash Surrender Value Excel Template

Download Excel TemplateExplanation

At times, the policyholder may require the amount he has set aside for the insurance policy for some urgent current need. He may take a loan against the policy, or he may surrender the policy and withdraw the accumulated savings after deducting fees and charges as per the terms and conditions of the policy.

We must understand that the surrender value is after all previous withdrawals and loan payments, if any taken, against this policy, plus the accumulated interest on the same. There may be partial or full surrender variants within the policy and the applicable penalties depending upon the criteria set in the policy.

How Does Cash Surrender Value in Life Insurance Work?

Key Takeaways

- A policy requires periodic premium payments accumulated in the policyholder’s account. The benefit of this policy is that the policyholder gets it at the time of his death or the policy’s maturity. This benefit is known as a death cover.

- As periodic premium payments increase during the policy’s tenure, the amount accumulated under the death or maturity benefit increases. It happens due to accumulated interest in the account’s total amount and bonus terms and conditions. At the end of the policy period or death, the accumulated amount returns to the policyholder or their heirs.

- Suppose the policyholder requires this to use the corpus, then he may surrender the policy. The accumulated amount is very low if he surrenders it early in life. Therefore the surrender charges eat up most of the accumulated amount, and the surrender value is low. Therefore most policies have a surrender period in which the surrender charge applies. Once this period is over and the amount is required, there is no surrender charge as the accumulated interest has covered it up. In such a case, the surrender value is higher.

- Now, let’s look at why this surrender charge is applied. When selling the policy, the insurance company incurs certain charges related to selling and putting the policy in place by completing the required paperwork. These costs form part of the surrender charges. Once the premiums start flowing in, the insurance companies start investing the same at higher return investments after reserving some amount that they may immediately need in case of sudden payment of a policy is required.

- The insurance company keeps some of the interests earned by the investments. Some of it goes to the policyholder depending upon the policy conditions. Through this investment, the insurance company recovers its costs and makes its profits.

- As the policy ages, its initial expenses get recovered. So once they fully recover and the surrender period gets over, there is no surrender charge on the premature surrender.

How is Cash Surrender Value Calculated?

The surrender value calculation can vary from one policy to another and can be specified in the policy document. However, a simple equation can be as follows:

Cash Surrender Value = Enhanced Accumulated Value – Surrender Charges.

- Enhanced value can be the total accumulated invested amount, including periodic interest.

- Surrender charges could be expressed in percentage terms and may vary based on the age of the policy.

Example

Let us understand the below example.

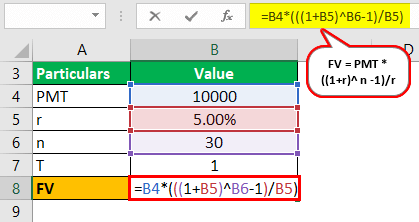

Suppose policyholder Mr. X has a policy for 30 years with annual premiums of $10,000 and a cover of $1 million if he prematurely dies. Otherwise, after 30 years, the total accumulated amount + a 10% bonus on the corpus will be distributed to him. The insurance company has incurred $5,000 in costs to implement this policy. Further surrender period specified by the policy is ten years, during which a surrender charge of 1% on the premiums unpaid will be chargeable, and none will be chargeable if surrendered after ten years. The return to be received on the premium amount is 5%.

Solution:

Now we understand the given numbers:

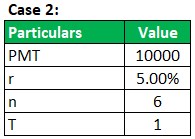

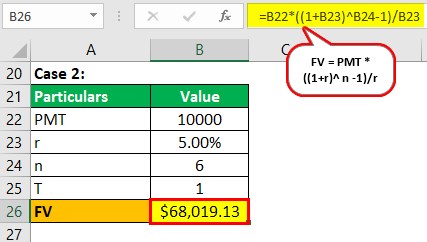

- PMT: 10000

- r: 5.00%

- n: 30

- T: 1

We need to solve the following equation to arrive at the required FV:

FV = PMT * ((1+r)^ n -1)/r

- = 10000 * (1+5%)^30-1)/5%

- = 664388.48

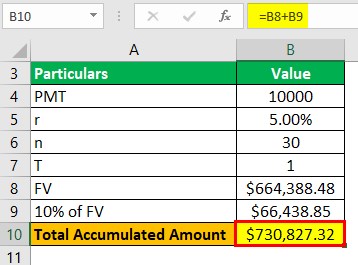

So, if he remains invested, he will get the FV + 10% of FV = $730,827.32

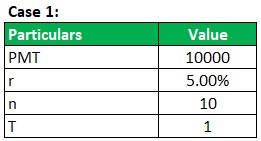

Case 1:

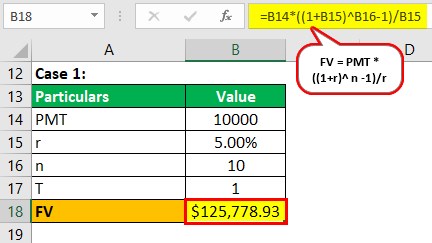

If he withdraws after ten years, he will get:

We need to solve the following equation to arrive at the required FV:

There are no surrender charges, so the cash surrender value is $125,778.93.

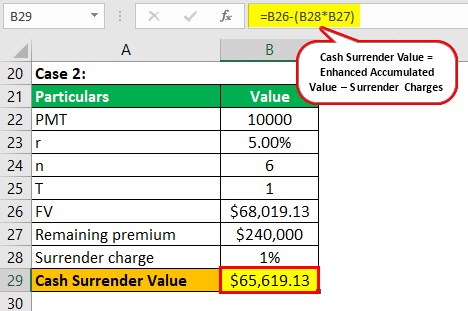

Case 2:

If he withdraws before ten years, let’s say in 6 years:

We need to solve the following equation to arrive at the required FV:

Of this, 1% on unpaid premiums is deducted as a surrender charge.

Premiums unpaid are 24 years x 10000 = 240000

Now, we will calculate the cash surrender value:

- = 68019.13– (0.01 x (240000))

- = $65,619.13

As we can see, the surrender charges are lower than the initial expenses incurred by the insurance company because it adjusts some amount due to the interest it earns on the premium amounts it invested. Therefore, the charge reduces as the number of unpaid premiums falls. After year 10, the insurance company assumes it will recover at least all its costs and therefore charge no surrender.

Cash Surrender Value Taxation

According to the Internal Revenue Service (IRS), the tax authority in the US, the cost basis of an insurance policy is the total of the premiums paid. So, any amount of surrender value that is greater than the total premium paid is considered a gain.

- Amount accumulated in the policy is not taxed.

- Loan payments against the policy are also not taxed.

- Withdrawal up to the amount of the cost basis is not taxable. However, excess of it is taxable at regular income tax rates instead of capital gains tax rate if the policy is “not property described.”

An example can explain the tax calculation:

Suppose policyholder X received the cash surrender value of $80,000 after deducting 5000 surrender charges. The total premium he paid till then was $70,000, so the amount of income to be taxed is cash surrender value – total premium paid, 80000-70000 = $10,000.

Cash Surrender Value vs Cash value

Cash value is the accumulated amount in the policy account, which we have termed enhanced value in the above example. At the same time, cash surrender value is the money the policyholder will receive if he withdraws before the completion of the policy or his death.

In the above example, the surrender charge is the difference between the two. Once the surrender period is over, the cash and cash surrender values are the same.

Conclusion

To sum up, the surrender value calculation varies per the policy terms and conditions, and the policyholder should read the policy documents properly before entering into it to assess whether the given policy is appropriate considering his financial circumstances. The policyholder should also look at the tax consequences of surrendering his policy per his jurisdiction and decide whether it is best to surrender the policy or take a loan against it to meet his immediate need.

Recommended Articles

This article has been a guide to Cash Surrender Value and its meaning. Here, we discuss how cash surrender value in life insurance works along with an example and calculation. You can learn more about it from the following articles: –