What Is Preferred Provider Organization (PPO)?

A Preferred Provider Organization (PPO) is a managed care medical insurance plan covering individuals and families. Under this scheme, the network of contracted medical service providers, such as doctors, hospitals, and medical facilities (preferred providers), offer healthcare services to the policyholders at a lower cost.

The private insurance companies generally provide PPO plans. The PPO provisions can facilitate the policyholders to have affordable medical care across various states and cities. These are well-suited for those who value flexibility and are willing to pay higher premiums; however, it is not cost-effective enough for lower-income groups.

- A preferred provider organization (PPO) is a medical coverage offering managed care, facilitating the members (individuals, couples, and families) to select their healthcare provider and take up medical services at a lower expense.

- PPO plans maintain a network of preferred doctors, hospitals, and healthcare facilities. They also permit the policyholders to consult out-of-network providers at a higher cost.

- Although these expensive health insurance plans require the members to pay higher than the usual monthly premiums, deductibles, and copays.

- It differs from the health maintenance organizations (HMOs), which are low-cost medical insurance requiring referrals and primary care physician involvement.

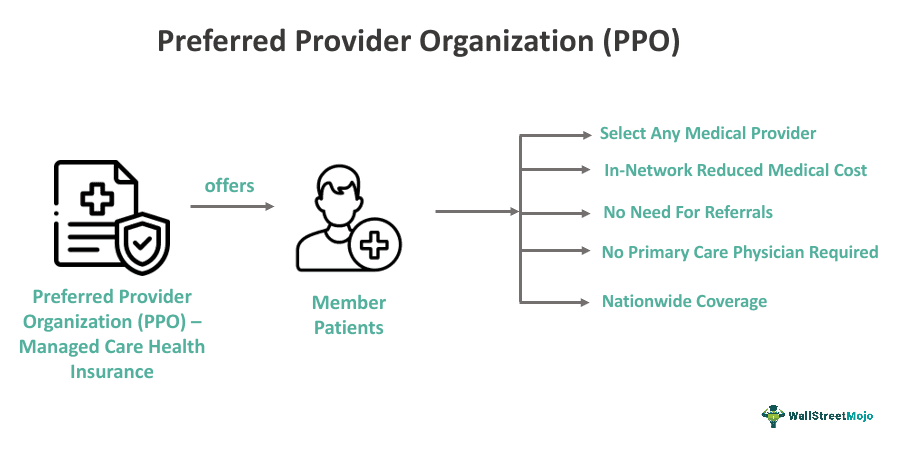

How Does A Preferred Provider Organization Work?

A Preferred Provider Organization (PPO) is a type of health insurance plan known for its flexibility in selecting healthcare providers. Individuals or employers purchase PPO insurance plans, becoming members of the PPO network. Members have the flexibility to select their healthcare providers. They can choose any doctor or specialist within or outside the PPO network. However, using in-network providers typically results in lower out-of-pocket costs. Moreover, these plans comply with state and federal healthcare insurance regulations, ensuring their operations adhere to the law.

The PPOs emerged in the United States in the 1970s in response to the increasing popularity of Health Maintenance Organizations (HMOs). It aimed to offer greater flexibility and choice to patients as an alternative to the restrictive nature of HMOs. Unlike other insurance plans like HMOs, PPOs do not mandate a referral to a specialist. This grants the insured greater autonomy in healthcare choices.

Such plans balance the needs of employers (who sponsor the plans) and employees (who utilize them) by offering a mix of cost-effective options and the freedom to choose healthcare providers. To effectively manage healthcare expenses, PPOs employ various cost control strategies. This includes utilization reviews and pre-authorization requirements for specific medical procedures. However, such plans entail payment of deductibles and coinsurance. They also often come with higher monthly premiums as a trade-off for the flexibility they offer.

Examples

Here are examples of Preferred Provider Organizations (PPOs) in the United States:

Example #1 – Aetna Preferred Provider Organization

Aetna offers PPO plans that offer both in-network and out-of-network coverage options, allowing members to select their preferred healthcare providers from a broad network. It provides discounted network rates and higher flexibility. One of the highlights is the Aetna Dental Preferred Provider Organization plan.

Example #2 – Blue Cross Blue Shield Preferred Provider Organization

Blue Cross Blue Shield (BCBS) is a network of independent health insurance companies in the United States. Many regional Blue Cross Blue Shield organizations provide PPO plans, granting members the flexibility to choose from a network of doctors and hospitals. BCBS PPO plans can differ depending on the state and the specific BCBS company offering the plan.

Example #3 – Cigna Dental Preferred Provider Organization

Cigna provides PPO plans that allow members to consult specialists without needing a referral and access a broad network of healthcare professionals. It is a dental medical insurance plan allowing members to select their dentist, whether they are part of Cigna’s network. However, visiting an in-network dentist often results in lower costs. Cigna Dental PPO covers preventive, basic, and major dental services, with coverage levels and expenses varying depending on the plan chosen.

Pros And Cons

Selecting a preferred provider insurance plan is based on individual healthcare needs, budget considerations, and personal preferences. Given below are its various advantages and disadvantages:

Pros

- Flexibility: Patients with PPO insurance can visit any specialist, doctor, or hospital without a referral, even if they are out of the network.

- No Primary Care Physician Required: Patients don’t need to opt for a primary care physician or make referrals to see specialists, streamlining the healthcare process.

- Out-of-Network Coverage: PPOs provide partial coverage for out-of-network healthcare services, ensuring that patients still receive some benefits when seeking care from providers not within the network.

- No Referrals Needed: Patients can directly consult with specialists without obtaining referrals, making specialized care more accessible.

- Nationwide Coverage: PPOs have extensive provider networks in different states, making them suitable for frequently traveling individuals.

- Preventive Healthcare: PPOs often promote preventive care and wellness initiatives, improving overall health outcomes and reducing long-term healthcare costs.

- Care Coordination: Coordination among healthcare providers is a priority for PPOs to ensure that plan members receive comprehensive and well-coordinated care.

- Transparency: It provides clear and transparent information about costs, coverage, and the network of medical providers to empower members in making informed healthcare decisions.

Cons

- Higher Premiums: PPOs have higher monthly premiums than other health insurance plans like HMOs.

- Deductibles and Co-Payments: Such plans often entail high deductibles and co-payments for various services.

- Limited Cost Control: Due to the flexibility to see out-of-network providers, managing and controlling healthcare costs may be more challenging compared to other plans with stricter cost controls.

- Pre-Authorization Requirements: Some PPO plans may necessitate pre-authorization for specific procedures or treatments, potentially adding administrative complexity.

- Provider Network Changes: Preferred provider organization insurance networks can change over time, potentially resulting in a patient’s preferred doctor or hospital no longer in-network, leading to care disruptions.

Health Maintenance Organization vs Preferred Provider Organization

Health Maintenance Organizations and Preferred Provider Organizations are two popular kinds of medical insurance plans in the United States; they have the following distinct characteristics:

| Basis | Health Maintenance Organizations (HMOs) | Preferred Provider Organizations (PPOs) |

|---|---|---|

| Definition | HMOs are insurance plans that offer cost-effective options with referral requirements and primary care physician (PCP) involvement. However, it has a limited in-network of medical providers, and the members cannot seek healthcare services outside the network except in emergencies. | PPOs are medical insurance plans with managed care that provide low-cost healthcare service to its members, allowing a greater flexibility to choose healthcare providers both in-network and out-of-network. |

| Flexibility | Coverage is primarily limited to in-network healthcare providers; it also requires members to designate a primary care physician (PCP) and obtain referrals from the PCP to consult specialists. | It offers greater flexibility in provider selection, both in-network and out-of-network providers. Moreover, the members can access specialists without referral requirements. |

| Network | A more extended network of preferred providers across various cities and states | Usually, there is a smaller network of medical providers; however, some plans may have an extensive network. |

| Cost Structure | Comparatively lower premiums but elevated out-of-pocket expenses | It involves expensive premiums but lower out-of-pocket expenses; it includes deductible and coinsurance charges |

| Referrals | Obtaining referrals from their designated primary care physician to access specialized care or specific medical procedures is mandatory. | PPO members can directly consult specialists without needing referrals from a primary care physician. |

| Out-of-Network Coverage | They are not covered by HMO plans, except for emergencies, leading to higher expenses if seeking care outside the network. | Includes partial coverage for out-of-network care, but members often bear an elevated cost. |

| Primary Care Physician (PCP) | HMO plans mandate the selection of a primary care physician (PCP) who oversees the member’s healthcare and provides referrals to specialists. | PPO plans do not require a PCP, allowing members to consult with specialists directly. |

Frequently Asked Questions (FAQs)

1. How much does the preferred provider organization cost?

The PPO cost varies as per the insurance company. Also, it is different for individuals of various age groups, couples, and families. For instance, an average PPO cost is $458 monthly for a 30-year-old person.

2. Is a preferred provider organization (PPO) a good option?

The PPO plans are a suitable option if the member can pay higher monthly premiums, deductibles, and copays to avail of a managed-care facility with the flexibility of choosing their medical provider, in-network or outside.

3. What is the difference between a preferred provider organization (PPO) and Point of service (POS)?

A Preferred Provider Organization (PPO) and a Point of Service (POS) plan are managed healthcare plans. However, PPO plans provide more freedom in choosing healthcare providers without requiring referrals but come with higher premiums and increased costs for out-of-network care.

On the other hand, POS plans emphasize using a primary care physician, referrals for specialists, and lower premiums, positioning them as a middle option between PPOs and HMOs in terms of cost and flexibility.

Recommended Articles

This article has been a guide to what is Preferred Provider Organization. We explain its examples, comparison with health maintenance organization, pros and cons. You may also find some useful articles here –