Retrocession Definition

Retrocession refers to the process by which a reinsurance company purchases an insurance scheme from another reinsurance company to cover its risks. This provision of reinsuring offers additional capacity to the original reinsurer, helping it prepare for future crises better.

The reinsurance companies sign a retrocession agreement to cede risks in case of a financial loss. Under the retrocession arrangement, the primary insurers and reinsurers unite to share the risk arising from huge insurance claims in the future. In finance, retrocession is a form of fees or commission paid by the company to a third party that brings business to it.

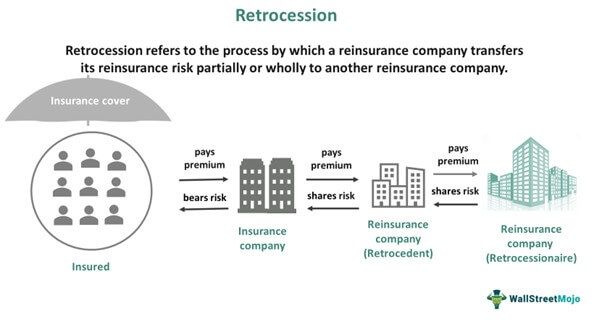

- Retrocession is when a reinsurance company transfers its reinsurance risk partially or wholly to another reinsurance company.

- Insurers and reinsurers sign a formal agreement and agree to share the risk of financial loss in case of a huge insurance claim.

- In finance, it is the commissions or fees paid by financial institutions to wealth managers who bring business to them.

- The types of retrocession agreements are specific and blanket retrocessions, whereas retrocession fees include banking fees, trading fees, and financial product purchase fees.

Retrocession Explained

In insurance, retrocession is the process of purchasing reinsurance by a reinsurance company to share its risk. Under this, the insurers and reinsurers sign an agreement whereby the former agrees to rescue the latter with full-fledged reinsurance coverage. By offering insurance coverage to clients, the entities take significant financial risks, which they need to have a backup in case of crisis.

For example, an insurance company purchases reinsurance coverage from the reinsurance company X, and X buys another reinsurance scheme from company Y. In this scenario, X is retrocedent, and Y becomes a retrocessionaire.

In the context of insurance or reinsurance, original insurers transfer a portion of their risks to another reinsurer. In case of catastrophes, like natural calamities and acts of war, the number of claims filed is huge, making it a blessing for the primary insurers and respective reinsurers.

Suppose five insurance companies out there have become reinsurers of their respective primary insurance companies. Then, when the claims are high in times of natural calamities, the primary insurer can share the portion of the claims with its respective reinsurer. As a result, no one entity experiences all financial burdens. Instead, it gets divided among all current market players involved.

The types of reinsurance that the reinsurers offer include spread loss reinsurance and stop loss reinsurance. While the former is where insurance companies pay reinsurers premiums during low-claim years and build their funds to recover them from losses when required, the latter is a type of reinsurance where reinsurance companies pay the primary insurers an aggregate retained loss as per their policy limits. The overexposure of claims for one insurance company is prevented with this process.

Retrocession in Finance

Besides being recognized as a retrocession agreement in the insurance industry, the term is also characterized as a fee charge or commission differently in various financial sectors. For example, Financial institutions, including banks, pay retrocession commissions or fees to wealth managers who work in partnership to bring businesses to them and achieve common financial goals.

The term also refers to kickbacks or finder fees offered to distributors and advisers, helping asset managers. The fees and commission are normally paid secretly, and no third party knows about it. The fee encourages wealth managers to pitch to more and more clients and make sure the banking institutions do well, and they earn a good commission in return.

However, when critically assessed, these fees are considered a payment model that makes wealth managers mislead clients/customers and recommend products, including mutual funds, that might not be the best for them.

Types of Retrocession

Retrocession, as a document of consent for insurers and reinsurers, can be classified into the following two categories:

- Specific: It covers only a single risk or a defined group of risks and is normally characterized by either pro-rata or excess loss reinsurance.

- Blanket: It offers coverage to the primary reinsurer’s complete portfolio. It is normally characterized as an excess of loss reinsurance.

On the other hand, retrocession as a fee or commission can be classified into the following categories:

- Banking retrocession fees: It is a commission that wealth managers receive from banking institutions for their efforts to bring more and more businesses to them.

- Trading retrocession fees: It is a payment done for various trades brokers and money managers undertake. One of the examples of such fees is the brokerage fee.

- Financial product purchase retrocession fees: It is paid for investment funds, which flow back to those who help with client acquisition.

Example

Example #1 – Retrocession in Insurance

Suppose an insurance company ABC Ltd. insures residents of hurricane-prone areas. In order to mitigate its risk, the company takes a reinsurance coverage with XYZ Ltd. The insurance involves significant risk as the insured are residents of areas known for frequent hurricanes. Therefore XYZ feels that the insurance claims from hurricane damage will be huge.

Hence, XYZ takes insurance from another reinsurance company DEF Ltd. in exchange for part of the premiums received from ABC. This is referred to as retrocession. It helps to spread the risk among different insurance companies. As a result, no one company will have to bear the loss alone if hurricanes occur. Swiss Re, Hannover Re, and Munich Re are some reinsurance companies that undertake retrocession.

Example #2 – Retrocession in Finance

The best example to cite would be JP Morgan’s settlement, which brought the concept of retrocession into the U.S. investment market for the first time. In 2015, the Securities and Exchange Commission (SEC) found that two investment advisory businesses of J.P. Morgan – J.P. Morgan Securities LLC (JPMS) and JPMorgan Chase, the banking subsidiary, chose to invest clients in its investment products but did not disclose to them the information, including conflict of interests, required for making well-informed investment decisions.

As per law, SEC found them at fault, and the subsidiaries had to pay $267 million for the wrongdoings under a record asset management settlement.

Frequently Asked Questions (FAQs)

What is retrocession?

Retrocession refers to the process through which a reinsurer shares its reinsurance risk with another reinsurance company. The companies involved enter into an agreement under which one reinsurance company provides reinsurance coverage to the other in return for premiums. This reduces the risk of overexposure in case of claims and helps as a backup.

What is retrocession in banking?

Financial institutions pay retrocession commissions or fees to money managers who bring clients to them. Also, they receive such fees from other funds to promote certain financial products to clients, which may or may not be in the clients’ best interest. Hence, these payments are quite contentious in the financial world. Usually, they are paid without the knowledge of clients.

Cite an example of retrocession.

Suppose an insurance company obtains reinsurance coverage from reinsurance company X. At the same time, considering the high degree of risk, X buys another reinsurance scheme from company Y. Such reinsurance cover offered to a reinsurer is referred to as retrocession. It acts as a backup in case of crisis. In this case, X is retrocedent, and Y is the retrocessionaire.

Recommended Articles

This has been a Guide to Retrocession & its Definition. Check out the concept of retrocession, retrocessionaire agreement, & fees in insurance & finance. You can learn more from the following articles –