Universal Life Insurance Definition

Universal life insurance is a type of permanent insurance policy, which covers the policyholder for the remainder of its life with flexible benefit options. These policies also include a savings factor often referred to as the cash value or the savings component.

Permanent insurance policies typically feature flexible and low premium payments. Other benefits allow the policyholder to grow its cash value with the appropriate amount of risk involved. For this reason, one may also hear universal life insurance referred to as cash value life insurance.

- Universal life insurance is a type of permanent life insurance wherein the policyholder is covered for life with flexible benefit options.

- Policyholders will have the flexibility to contribute additional capital towards the premium payment. The excess money will then be added to the cash value, where it can accumulate interest.

- The interest rates will typically be tied to the performance of a stock market index. It could be positive while the markets are outperforming and negative when the stock market is underperforming.

Explanation

Universal life insurance policies are distinct from other types of insurance policies in the flexibility they give to the policyholders. The universal life policy is a type of permanent life insurance, meaning the policy will be active for one’s entire life as long as the premium payments are made.

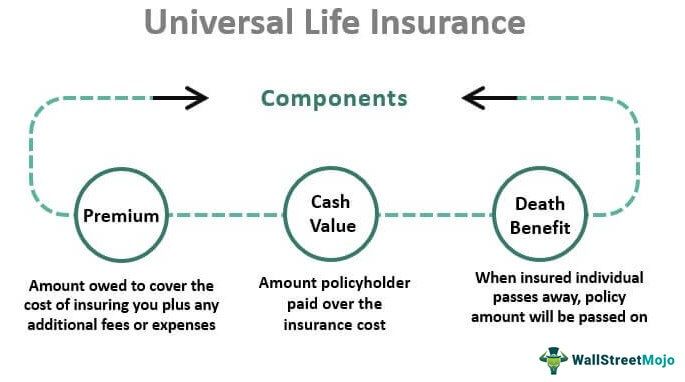

The universal life insurance policy will consist of three components, including:

- Premium (cost of insurance)

- Cash value, and

- Death benefit

Each component plays a crucial role in the policy’s makeup and makes it an attractive option for individuals looking for permanent life insurance.

Premium (Cost of Insurance)

The premium will be the amount owed to cover the cost of insuring one plus any additional fees or expenses. It will be a minimum payment to keep one’s policy active.

Premium payments are unique when it comes to universal life insurance, as one can pay or contribute more money towards the premium if desired. If one decides to contribute toward the universal life policy, the insurance company will put the additional fees towards a savings account or the cash value.

Cash Value

A universal life insurance policy’s cash value is the amount the policyholder paid over the insurance cost or the premium. The type of policy one elects to go with will determine how its money is managed in this account. It will either be tied to a stock index or earning a set amount of interest.

If the minimum premium amount is not met, the universal life insurance company will deduct the payment amount from the cash value. The policyholder can also decide to make withdrawals from this account as it grows in value. However, if one chooses to make withdrawals, they may have to pay taxes on them.

Death Benefit

When the policyholder or the insured individual passes away, the policy amount will be passed on or paid out to the beneficiaries. Depending on how the policy is set up will determine how the cash value and payments get distributed.

In many cases, when the insured individual passes away, the universal life insurance company keeps the cash value amount. However, if the policy is set up that way, the beneficiaries can also receive the cash value amount.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

Pros and Cons

Permanent life insurance policies have specific benefits that make them attractive for certain individuals. However, they are not for everyone, and some people may be better off with a different type of policy, such as a whole life insurance plan.

Pros

- Flexible Premium Payment – The flexibility in payments is a significant advantage for policyholders. One can contribute more towards its premium payment, and the excess amount will be added to the cash value amount. One can also use the cash value amount to pay the premium amount if desired in some cases.

- Earned Interest – With permanent life insurance plans, one can also earn interest on its cash value amount. The rate at which the cash value will earn interest will typically be tied to a stock market index’s performance. Many insurance companies will offer protection from risks associated with the stock market.

- Withdrawals – As time goes on and one’s cash value begins to accumulate, one can withdraw money from the account. Keep in mind one will have to pay taxes on life insurance withdrawals in most cases.

- Flexible Death Benefit – Having the ability to increase or decrease the amount of benefits that get paid out can be a significant factor for some individuals. Making adjustments to the death benefit of an insurance policy can affect the premium payments.

Cons

- Variable Rates – Although many people would consider having the rates dependent on market performance a positive, it can also lead to lower rates in some instances. If the market underperforms, one would be paying more premiums and earning a low amount of interest.

- Active Status – For the policy to remain active, it may require one to maintain a certain balance of cash value, or at the very least, a positive balance.

Universal Life Insurance vs Whole Life Insurance

Both universal and whole life insurance are popular options when it comes to permanent life insurance policies. They both provide benefits upon one’s death to the beneficiaries it has nominated, but they also have key differences between them. These include:

Premium Payments

With universal life insurance, one has the flexibility to increase its payment amount and contribute additional capital towards the cash value. It is different from whole life insurance, where one has a set premium amount that is determined when the policy is purchased. The insurance company will invest a portion of the premium payment on one’s behalf to grow and accumulate over time.

Death Benefits

Permanent life insurance policies allow the policyholder to adjust the death benefit, increasing or decreasing it when needed. On the other hand, whole life insurance offers a fixed death benefit that pays a set amount to the beneficiaries.

Interest Rates

With a universal life insurance policy, the interest rate will typically rely on the financial markets’ performance. It is opposed to whole life insurance, where one would have a guaranteed cash value amount.

Universal Life Insurance vs Term Life Insurance

Term life insurance is another standard option for a life insurance plan. Let us find out how it compares to universal life insurance below.

#1 – Coverage Length

Universal life insurance will cover the insured for their entire life. With a term life insurance policy, the insured will be covered for a predetermined amount of time. The length of coverage will typically be 10, 20, or 30 years.

#2 – Cash Value

As previously mentioned, universal life insurance policies will build cash value that allows the policyholder to make withdrawals if necessary. Term life insurance policies do not offer this feature. However, the premium payment will also typically be lower, allowing the policyholder to build its savings.

#3 – Premium Payments

As opposed to the flexibility allowed with universal life insurance, term life insurance plans will have a set premium amount. The flexibility enables permanent life insurance policyholders to contribute more towards the cash value.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Recommended Articles

This has been a guide to Universal Life Insurance and its definition. Here we provide a detailed explanation, its differences from whole life insurance and term life insurance along with pros and cons. You can learn more from the following articles –