What Is Fire Insurance?

Fire insurance protects an individual or a business against property loss or damage caused by an unintentional fire. It may, however, require the policyholder to meet specific fire safety standards to become eligible for the coverage. The coverage limit typically depends on the fire origin, the type of asset, and the insurance provider.

Obtaining insurance coverage entitles the insured to reimbursement from the insurance company in the event of fire damage. A fire insurance policy covers buildings, machinery, merchandise, furniture, and other personal possessions. Most insurance policies cover fires caused by natural disasters, gas explosions, and electrical faults. Although the policyholder needs to pay a premium for it, they can use the compensation to replace, repair, or rebuild the property.

- Fire insurance protects a person or a business from property loss or damage caused by accidental fire from natural disasters, gas explosions, and electrical faults.

- The insurance company reimburses the market value of lost buildings, machinery, products, furniture, and other personal belongings. However, it sets a coverage limit based on the cause of the fire and the asset type and value.

- Making a fire insurance claim necessitates notifying the insurance company, understanding and adhering to policy terms, and completing paperwork.

- These insurance policies come in various forms, including basic, valued, comprehensive, average, floating, consequential loss, replacement, etc.

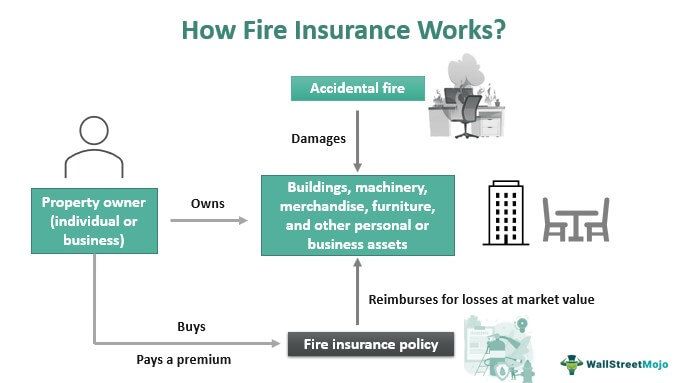

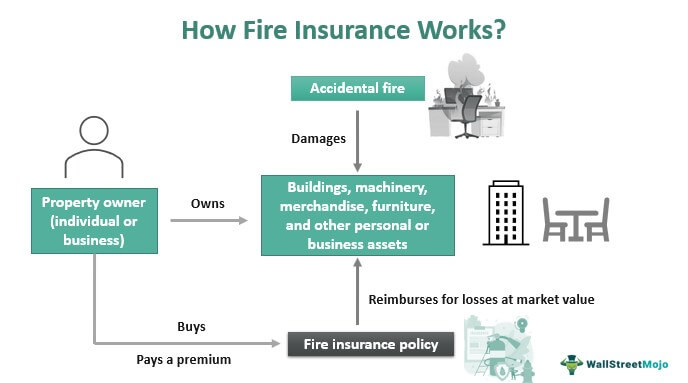

How Does Fire Insurance Work?

Fire insurance provides coverage to damaged personal or business assets and property due to fire, regardless of its origin. Property and homeowners insurance are other names for it. In some cases, it covers living expenses until the suffering party receives the reimbursement. The compensation helps the policyholder recover from the loss by repairing, replacing, or reconstructing the property. The insurance company reimburses for lost property at its market value. But it sets a coverage limit, such as for rare and luxury items.

The homeowner insurance often includes this insurance, though one can buy it as a separate policy if required. A standard fire insurance company informs potential policyholders about the many types of coverage available, ranging from basic to comprehensive. The insurance policy and coverage depend on many factors like the nature and value of the personal or commercial property, cause of the fire, location, etc. It is a legal prerogative for public property to have this insurance.

Fire Insurance Coverage

| Includes | Does not include |

|---|---|

| Accidental fires due to natural disasters, electricity faults, gas explosions, lightning, smoke, and water tank or pipe damage. | Fires caused by arson, nuclear radiation, war, theft, invasion, human negligence or on purpose, and insurrection. |

The standard fire insurance company sends surveyors or claims adjusters to assess the extent of the damage to the facility upon receiving a claim. It is to classify various furniture and accessories damaged or are likely to create a fire. They also record the presence of fire prevention, fire fighting, and fire suppression systems. It then decides the amount of compensation based on that and the type of fire insurance policy. The policyholder has the option of receiving reimbursement as a replacement cost or actual cash settlement.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

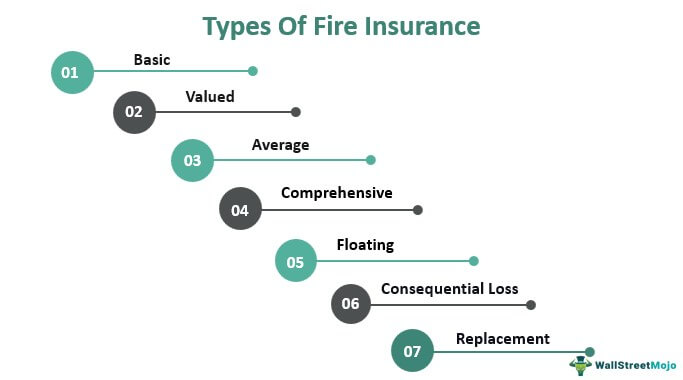

Types Of Fire Insurance

Before selecting a fire insurance policy, one must consider several factors, such as the property type and associated items. Let us look at different types of insurance protecting against fire damage based on one’s requirements:

#1- Basic Insurance

The definition of basic fire insurance coverage depends on the insurance firm involved. It usually covers residential and commercial properties.

#2 – Valued Insurance

It entails the insurer compensating a property for a fixed amount of money. If the sum is less than the amount specified in the insurance policy, reimbursement occurs. The indemnity will be held until the amount insured is reached. It also disregards the property’s actual value, and it does not penalize the insured for insuring for less.

#3 – Average Insurance

Under this insurance type, the policyholder is penalized for getting an insurance policy at a lesser sum than the property’s actual value. The sum is calculated based on the degree of the value difference.

#4 – Comprehensive Insurance

The insurance provider providing this type of policy pays the overall value of the property and associated items damaged in the fire rather than the partial reimbursement typical of basic insurance. This type of insurance is for everyone who owns a building that houses valuable items. They need to ensure that the insurer assumes as much liability as possible.

#5- Floating Insurance

This policy intends for import and export businesses that have merchandise spread across multiple warehouses. The insurance premium charged is frequently the average of specific policy charges for each item.

#6 – Consequential Loss Insurance

A fire might halt output at a corporation or manufacturing unit, resulting in a loss of revenue. This insurance policy covers the aftermath of a fire and determines compensation based on the severity of the damage.

#7 – Replacement Insurance

In this policy, the insured receives compensation, i.e., replacement cost, based on the market value of the property calculated using the depreciation rate.

In addition to the above, there can be other custom insurance types depending on the insurer. Companies with a global presence tend to provide more comprehensive insurance policies, though they might be a tad more expensive. But the extra payment almost always turns out to be worth it after a fire.

Examples

Fire insurance offers many advantages to property owners in different scenarios, such as:

#1 – Civil Structures

Some structures must get this insurance as part of their civil rules. The state or country can deny a permit to build or occupy a building without insurance. It does not, however, suggest purchasing the cheapest property insurance.

#2 – Residential Properties

Before getting this insurance for the home, the owner should keep a few things in mind to avert the risk of fire and reduce the premium, such as installing fire suppression systems. They should consider covering rare and expensive items in their homes in the home fire insurance policy. The insured must also increase their coverage amount if the house value rises at some point. A standard fire insurance company reimburses for repair, replacement, and additional expenses incurred due to the fire.

#3 – Commercial Facilities

A business that warehouses expensive items in a fire-prone place should get this insurance. An example of this is a high-end restaurant, which may have expensive furniture, rugs, lightings, and many other things that could catch fire. Even if a small fire breaks out in the kitchen, the process of putting it out may cause harm to valuable items that are not even in the fire’s path.

Claims

One must file a fire insurance claim with the insurer to get coverage for damages caused to the property by fire. Filling an insurance claim requires informing the insurance provider, following specific rules, and filling out documents. Some companies even make the claim forms available online, eliminating the need for the party to visit the office.

While some insurers restrict the insured from filing any claims for two or three months after signing the policy, others set several days after the fire, after which the insured can file a claim. Waiting too long to file a claim after a fire can turn it invalid.

It is critical to record losses caused by a fire without replacing or disposing of anything on the premises. The owner should have sufficient evidence as photographs, videos, and documents depicting the property and its contents to support their claim and simplify the damage assessment. The surveyor or claims adjuster sent by the insurance company makes a detailed report of the incident. The insurer then calculates the compensation based on this.

The policyholder should review the reimbursement estimate and compare it to the insurance provisions. They must also ensure if the compensation is on a replacement cost basis or actual cash settlement for the fire-damaged property. The latter does not allow the owner to recoup the loss at current market value, but adding a rider to the policy and paying higher premiums will.

The most crucial element to ensure that a claim is paid in full is that the claimant understands the policy terms and adheres to them.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What does fire insurance cover?

Fire insurance covers property losses caused by accidental fire from electrical faults, bursting of a water tank, gas explosions, natural disasters, etc. Some policies also compensate damages to associated objects caused due to the fire. The insurer, however, may set a coverage limit for rare and luxury items.

Does fire insurance cover negligence?

No, fire insurance does not cover fire accidents that happen out of negligence, i.e., a fire started on purpose or for entirely artificial reasons. Similarly, the coverage excludes fire damage from arson, nuclear radiation, war, theft, invasion, and insurrection.

How much does fire insurance cost?

Fire insurance coverage cost depends on the type of the policy, the nature and value of properties damaged, the insurer, and the location. The homeowner insurance often includes this policy, though one can buy it as a separate policy based on the requirements.

Recommended Articles

This has been a guide to Fire insurance and its meaning. Here we discuss how does fire insurance work along with types, examples, and claims. You may also learn more about financing from the following articles –