Risk Insurance Definition

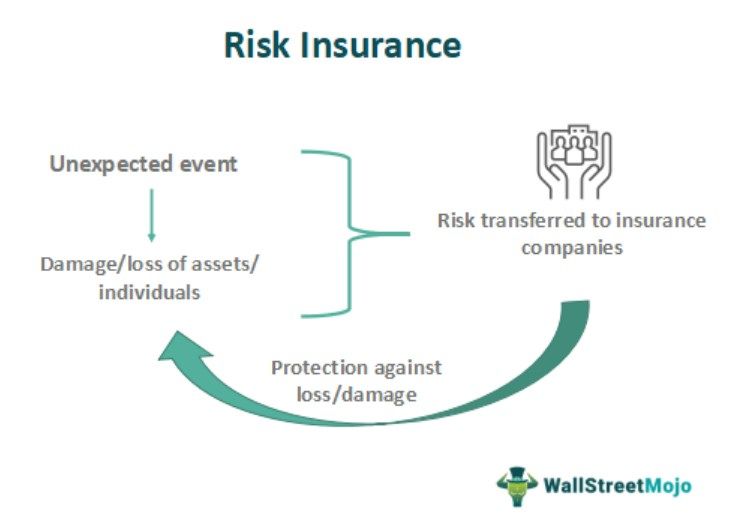

Risk insurance refers to the risk or chance of occurrence of something harmful or unexpected that might include loss or damage of the valuable assets of the person or injury or death of the person where the insurers assess these risks and, based on which, work out the premium that the policyholder needs to pay.

Most of the risks are nowadays insurable by insurance companies. These companies calculate the probability of the events and their impact and then calculate the premium accordingly. It protects the individuals and entities from heavy financial losses by transferring the burden of loss to the insurance company in exchange of the premium.

- Risk insurance, also known as insurance coverage or risk transfer, is a financial product that protects against potential losses or damages resulting from specific risks or events.

- Risk insurance helps individuals, businesses, and organizations manage and mitigate the financial impact of unforeseen events such as accidents, property damage, liability claims, natural disasters, or other covered perils.

- Risk insurance works on the principle of pooling risks, where policyholders pay premiums to the insurance company, which then uses those funds to compensate policyholders for covered losses based on the terms and conditions of the insurance policy.

Risk Insurance Explained

Risk insurance and management shall involve assessing the price to be paid to Insurance policyholders who have suffered from the loss that occurred to them, which is covered by the policy. It involves various types of risks such as theft, loss, property damage, or someone being injured; there is a chance that something unexpected or harmful may happen at any time.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

All risk insurance evolves in calculating the pay of the financial value for the damages that might occur to the insured property or item that might be lost, injured, or destroyed accidentally or often occur to happen. It also states how much it would cost to replace or repair such an insured item to cover the loss suffered by the policyholder in case of such damage. Insurers shall calculate claims and evaluate their risks.

The term of risks in insurance says how the insurers evaluate their chances in issuing insurance policies to the policyholders on the loss that may occur due to loss, theft, or damage to the property or even someone injured. This concept also says the types of risks involved in insurance issuance. It also helps the insurers to evaluate the risk and calculate the claims that can be paid in the future at any point in time if the damage or loss occurs.

Types

The following are the different types of risk in insurance:

#1 – Pure Risk

- Pure risk refers to the situation where it is certain that the outcome will lead to loss of the person only or maximum it could lead to the condition of the break-even to the person, but it can never cause profit to the person. An example of pure risk includes the possibility of damage to the house due to natural calamity.

- In case any natural calamity occurs, it will damage the house of the person and its household items, or it will not affect the person’s home and household items. Still, this natural calamity will not give any profit or gain to the person. So, this will fall under the pure risk, and these risks are insurable.

#2 – Speculative Risk

- Speculative risk refers to the situation where the direction of the outcome is not specific, i.e., it could lead to a condition of loss, profit, or break-even. These risks are generally not insurable. An example of speculative risk includes the purchase of the shares of a company by a person.

- Now, the prices of the shares can go in any direction, and a person can make either loss, profit, or no loss, no profit at the time of the sale of those shares. So, this will fall under the Speculative risk.

#3 – Financial Risk

Financial risk refers to the danger in which the outcome of the event is measurable in terms of the money, i.e., any loss that could occur due to the risk can be measured by the concerned person in monetary value. An example of financial risk includes a loss to the goods in the company’s warehouse due to the fire. These risks are insurable and are generally the main subjects of all risk insurance.

#4 – Non-Financial Risk

Non-Financial risk refers to the risk in which the outcome of the event is not measurable in terms of the money, i.e., any loss that could occur due to the risk cannot be measured by the concerned person in the monetary value. An example of the non-financial risk includes the risk of poor selection of the brand while purchasing mobile phones. These risks are uninsurable since they cannot be measured.

#5 – Particular Risk

Particular risk refers to the risk which arises mainly because of the actions or the interventions of the individual or the group of some individuals. So, the origin of the particular risk by individual-level and impact of the same is felt at a localized level. An example of a specific chance includes an accident on the bus. These risks are insurable and are generally the main subjects of the insurance.

#6 – Fundamental Risk

Fundamental risk refers to the risk which arises due to the causes which are not under the control of any person. So, it can be said that the fundamental risk is impersonal in its origin and the consequences. The impact of these risks is essentially on the group, i.e., it affects the large population. The fundamental risk includes risks on the group by events such as natural calamity, economic slowdown, etc. These risks are insurable.

#7 – Static Risk

Static risk refers to the risk which remains constant over the period and is generally not affected by the business environment. These risks arise from human mistakes or actions of nature. An example of static risk includes the embezzlement of funds in a company by its employees. They are generally easily insurable as they are easy to measure.

#8 – Dynamic Risk

Dynamic risk refers to the risk which arises when there are any changes in the economy. These risks are generally not easy to predict. These changes might bring financial losses to the members of the economy. An example of the dynamic risk includes the changes in the income of the persons in an economy, their tastes, preferences, etc. They are generally not easily insurable.

Example

Here we try to understand the concept of risk insurance and management with the help of an example.

Let us assume a bakery that has a huge outlet in a prominent and busy part of a city. The manufacturing and sale takes place in the same outlet. In this case, the risk insurance will be quite high, considering the operation system. The outlet will have a lot of electric gadgets and ovens which are itself quite risky.

Moreover, in the same outlet, customers will visit for purchase, adding to the risk. It is also located in a busy part of the city, which means that a minor accident may result in significant damage due to a lack of space. Therefore, this bakery will have to take a special risk insurance to insure its outlet to mitigate the loss risk in exchange for a high premium.

Factors For Calculating Premium

This concept explains the protection provided by the insurance company to the individuals or entity against any risk which might be due to a wide range of events. However, the premium calculation is based on certain factors. They are as follows:

- Event occurrence – If the chance of occurrence of the particular event is high, then the premium will be more and vice versa. Thus, the policyholder will have to pay for a the high risk insurance.

- Level of damage – If the level or severity of the resultant damage or loss is assumed to be very high, then the insurance company will charge higher premium because in case of happening of the event, the insurance company will have to disburse a higher claim, which is a loss to them.

- Amount of risks – It is essential to assess the value of the risk that will be covered. If the company covers more perils or events, the insurance policy will become more expensive. This is because of the higher probability of a claim resulting in special risk insurance.

Advantages

Let us understand some advantages of the concept:

- It offers financial protection against the heavy losses due to unforeseen situations. The insurance helps mitigate the risk.

- It provides some peace of mind to the individuals or companies who may face the risk, allowing them to channelise their time and funds to some more productive work.

- It allows the business to continue. The entity does not have to stop its operations due to fund crunch resulting from some unforeseen situations.

- Very often, insurance companies provide some additional services to policyholders in the form of advice or guidance regarding risk mitigation or risk assessment.

- The insurance companies provide covers which are customized to meet the demand and need of the policyholders.

Disadvantages

Some disadvantages of the concept are as follows:

- The premium costs rise with the rise in risk. The policyholders need to bear the high risk insurance.

- The policies may have a number of deductibles, exclusions and out of pocket expenses which the policyholders should be aware of while taking the insurance.

- The process of claim disbursement may be complex and time consuming involving a lot of documentation and investigation.

- Sometimes individuals or companies may end up taking multiple insurance policies for same risk, resulting in payment of extra premium.

Thus, it is necessary to check both the benefits and limitations of risk insurance policies so that it is possible to make informed decisions.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What factors should I consider when choosing a risk insurance policy?

When choosing a risk insurance policy, it’s essential to consider factors such as the type and extent of coverage needed, the reputation and financial stability of the insurance provider, the policy exclusions and limitations, the premium costs, the deductible amounts, and any additional policy features or riders that may be available.

How do insurance companies determine the premiums for risk insurance?

Insurance companies determine premiums based on various factors, including the type and level of risk being insured, the insured party’s claims history, the value of the insured property or assets, the coverage limits, the deductible amounts, and actuarial calculations that take into account the likelihood and potential severity of future losses.

What is the claims process for risk insurance?

In the event of a covered loss or damage, the insured party must promptly notify the insurance company and provide the necessary documentation and evidence to support the claim. The insurance company will then assess the claim, verify coverage, and determine the appropriate amount of compensation based on the policy terms.

Recommended Articles

This has been a guide to Risk Insurance & its definition. We explain its types with examples, factors for premium calculation, advantages & disadvantages. You can learn more about from the following articles –