What Is Incontestability Clause?

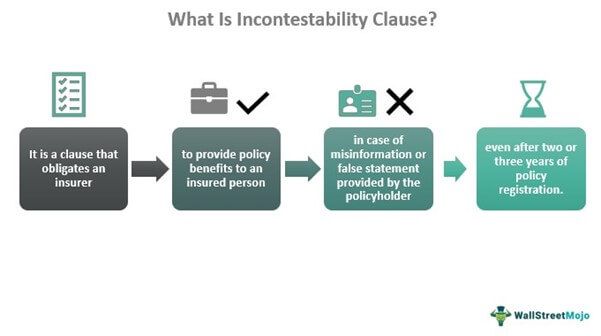

An incontestability clause in insurance policy forbids the insurer to withdraw or turn away from policy terms and conditions in case of misinformation or false statement provided by the insured person in their application. This provision allows the insured person to avail of policy benefits even after two or three years of the finalized contract.

The incontestability clause defines situational discretion between the policyholder and the insurer (insurance provider). The life insurance incontestability clause aims to protect the interests of the policy buyer from an unjustified denial by the insurer. At the same time, this clause gives the insurance company time to verify and identify any misinformation about the applicant.

- The incontestability clause in insurance is one of the most vital provisions in an insurance policy, protecting the interest of the policy buyers.

- According to the incontestability clause, an insurer (insurance company) cannot void a policy’s coverage due to misinformation provided by the applicant.

- The contestability period, which is two or three years from the date of effect of the policy, allows the insurance company to verify and identify any misinformation or fraudulent statements made by the insured.

- Thus, the insurer cannot invalidate the policy based on misinformation after the contestability period. However, this clause is subject to some exceptions.

Incontestability Clause In Insurance Explained

The incontestability clause definition explains its purpose in an insurance policy. For instance, in a life or disability insurance policy, this clause protects policyholders’ interests against unjustified denial of policy coverage by the insurer because of misinformation.

In addition, this clause elaborates that the policy will not stand void due to some misinformation after the contestability period is over. Under the contestability period, the insurance company shall thoroughly review the buyer’s application, medical data, and history to correct any misinformation or false statement.

Thus, an insurance provider or company may challenge the policyholder’s claims in court if they detect that the applicant made fraudulent statements intended to deceive the company. For instance, an applicant can ask someone else to take a medical examination for them and provide it to the insurance company to seek an early claim.

However, if the insurance company detects that the applicant intentionally provided false information, they cannot directly cancel the contract. Similarly, the insurer cannot rescind the policy coverage using a notice only. Instead, the insurer shall file a suit to challenge the claims of the insured person and invalidate the insurance contract. Legal proceedings shall decide the outcome for the policyholder and the insurance company.

Thus, the incontestability clause is included to protect the interest of the insured individual. It saves them additional cost and time invested in case of a legal proceeding. In addition, the clause specifically mentions that the contract or policy is not voidable after two or three from its date of effect due to any misinformation from the claimant.

The incontestability clause also mentions the failure of insurance coverage in case the insured person attempts outright fraud. Albeit, Nonetheless, it is the most vital and most guaranteed provision in an insurance policy in favor of the policyholder.

Examples

Let us now look at some examples to understand the meaning and uses of the incontestability clause comprehensively,

Example #1

Suppose John is an equity analyst at S&P Global, and his friend Ray is a diving coach at Boston University. Both have recently renewed their life insurance with Sun Life, and their applications remain within the contestability period.

According to the contract, the contestability period is two years. This period allows the insurance company to review their applications and cross-check their medical data and history. In addition, this review period gives the insurance company the time to look into any false statements or misinformation provided by the applicants.

Thus, as John and Ray renew their insurance after some time, the changes in their physical health and attributes or any other medical information shall be updated by conducting a medical examination. This examination will provide updates about the current state of their health and well-being. In addition, it reduces the scope of any fraudulent statement or misinformation about the beneficiaries.

Albeit, if the insurance company invokes the incontestability clause due to fraudulent information provided by John and Ray, they are liable to reimburse the premiums paid.

Example #2

Claire works as an insurance agent for Healthy Life Insurance Limited (HLIL) and has recently sold two life insurance policies to an elderly couple in their late 50s or 60s. The insurance policy’s incontestability period is three years, allowing the insurer to verify the applicant’s information and approve the insurance.

However, after one year into the insurance contract, during a data entry, the officials recognized that the couple had filled in their age incorrectly. As this can be a genuine mistake, according to state regulation, the insurer corrected the information and altered the policy benefits accordingly. Consequently, the insurance company will not cancel or invalidate the insurance policy.

Thus, if any significant medical illness or life-threatening disease was discovered in the aged couple, the insurer could invalidate the policy as the contestability period was ongoing. However, in case of minor misinformation, the insurer usually only validates the policy.

Exceptions

The incontestability clause balances the interests of the policyholders against that of the insurer. At the same time, the contestability period provides a leeway for the insurance company. In addition, it assists the insurer in verifying and identifying any mistranslations or misstatements in the application.

However, the insurer cannot tamper with the flow of policy benefits and its coverage to the buyer post the contestability period. Nonetheless, some limitations or exceptions to this incontestability clause exist that allow the insurer to pull back the policy. These include,

- Lack of insurable interest of the policy owner wherein they might not be regular with premium payments. It indicates a need for proof that an individual will face financial difficulty due to the loss or damage of a person or an item.

- Suppose an applicant asks another individual to take the medical exam for them. It indicates the applicant’s intentions in hiding or concealing the true information from the insurer. Thereby leading to the insurer invalidating the contract.

- If the insurer discovers that the policyholder never consented to the coverage or its benefits, they may nullify the policy.

- Any other reason indicates that the insured has intentionally provided misinformation or false statements to deceive or harm the insurer.

- An insurance company can also cancel a life insurance policy when the insured passes before the contestability period are over. The insurer’s invalidation of the policy restricts the benefits from being passed to the deceased’s family.

Thereby, an insurance company ensures that the entire medical history of the insured person is documented and verified before it approves the insurance policy. Albeit making errors while filling out applications and completing other formalities may be usual, the advantages of the incontestability clause shield both the buyer and the insurer.

Frequently Asked Questions (FAQs)

1. Who is protected under incontestability clause?

Insurance companies introduced the incontestability clause in the late 1800s as an ethical practice to vividly protect policy buyers’ interests. Majorly the clause restricts the insurer from canceling policy coverage due to misinformation by the policyholder, which may be discovered after two or three years. Over time, the clause has proven beneficial for the insured and the insurer. Thus, in case of proven or intentional fraud by the insured, the insurer can outright invalidate the contract.

2. What is the purpose of the incontestability clause?

The incontestability clause obligates the insurance companies to thoroughly verify and review the policy buyers’ application to check that the applicant has not concealed any critical information. Thus, after two to three years of implementing the policy, the insurer must refrain from canceling policy coverage due to misinformation. However, this clause is subject to some exceptions.

3. What is the incontestability clause in life insurance?

Such a clause in a life insurance policy benefits the policyholder or buyer. It protects the interests of the beneficiaries against unjustified or unreasonable claims of the insurance company to void or nullify the insurance policy coverage or contract in case of death or undetected health conditions of the life insurance policyholder.

Recommended Articles

This article has been a guide to what is Incontestability Clause. Here, we explain its significance in insurance, along with examples and exceptions. You may also find some useful articles here –