What is Insurable Interest?

Insurable interest refers to the importance placed by an individual for certain things, events, or another person in their life. The presence of such resources is essential for the individual’s life and contentment. Its absence, on the other hand, produces pain or financial trouble.

The concept central to insurance policies was first applied in the Marine Insurance Act of 1745. It was aimed to put an end to the practice in which a person with no business stake in a marine cargo would purchase marine cargo insurance, basically speculating on whether or not the vessel would reach securely at its location.

- The principle of insurable interest meaning explains that it is essential for a policyholder to have an insurable interest in the subject matter of insurance.

- The application of the concept was first seen in the Marine Insurance Act of 1745 to halt the practice of people with no financial stake in maritime cargo purchasing marine cargo insurance to gain from unfortunate events destroying the cargo.

- Usually, it is valid if a person purchases life insurance for close relations like parents, spouses, children, business, and key business employees.

Explanation

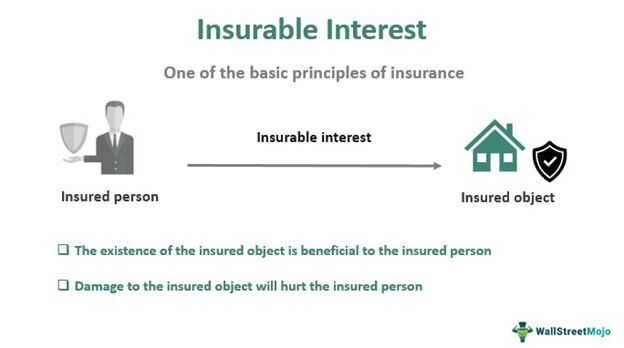

Insurable interest forms the core principle of insurance. It is attributed to the insured object since the object’s healthy existence yields benefit to policyholders. It is the motivating factor that makes people take protective measures against unforeseen events damaging the beneficial thing. Thus, it acts as a qualifying criterion for granting insurances, and its identification is often based on ownership rights, possession, or close relationships.

In various circumstances, it determines whether to issue an insurance policy or not. The issuance based on reasonable interest gives the policyholder protection against financial consequences of unanticipated catastrophic events and saves insurance companies from entering into void contracts. Also, the concept prevents someone from getting insurance for the assets owned by others. For instance, an insurance company can grant a retailer shop insurance and reject if the application is for his friend’s shop.

People can get insurance for anything valuable that they own, such as cars, expensive art, real estate, or similar possessions. According to insurable interest in life insurance, generally, a person can’t get insurance for another unrelated person. It prevents people from betting on someone’s death by determining who is eligible to take out an insurance policy on someone else’s life. If people could get life insurance policies in anyone’s name, they could quickly look for people with higher risks of dying and profiting from their deaths. It is unethical, and it would also bring losses to insurance companies.

Any contracts lacking reasonable interest are legally invalid, even if the contract is already signed. Because of this, it’s essential to know whether you’re eligible to rely on one or not. It’s also vital to note that most legislations do not allow someone to take an insurance policy on someone else’s life or property without that person’s consent. So, one needs to prove that the person is aware of the arrangement before doing it. In the case of life insurance, the following is a usual list of people for whom a person can buy life insurance:

- Spouse

- Children

- Parents

- Siblings

- Business partners

- Key employees in the business

Insurable Interest Example

Jack has several people who depend on him to survive, so he decides to get life insurance for himself. After he chooses a package, the insurance company will naturally determine whether the nominees listed on the documents are deserving or not from a legal perspective. In most cases, life insurers prefer close family members as dependent or nominees. They believe that making a nomination for someone who is not an immediate family makes the likelihood of fraud significant.

The insurance company officials find out that he is married with two kids, has a father that is getting very old, and a niece who is also financially dependent on Jack. He can list directly related people like his kid, spouse, or father as a nominee since they are a clear case of insurable interest. However, to list niece, a distant relative, as a nominee, he should prove the insurable interest with documentation or proof like a guardian certificate. It is to confirm that the nominated distant relative depends on the insured person’s life for a living.

Insurance Interest Principle

Insurance policies are not a way to accumulate wealth but to attain protection from the consequences of unanticipated losses. Therefore, the policyholder should have a vested interest, especially a financial tie with the covered item. The insurable interest principle states that getting insurance should be prompted by reasonable interest, ownership right, or a close relationship to the insured object. A legitimate rationale or relationship explaining the relevance of the subject matter of insurance in their life must exist for a person to avail of insurance. Fundamentally, the principle states that the presence of insurable interest is vital in gaining an insurance policy.

Frequently Asked Questions (FAQs)

What is the principle of insurable interest?

The principle explains that the statutory right to protect or insure stems from a financial connection between the policyholder and the subject matter of insurance. Thus, precisely, the policyholder should have an insurable interest in the subject matter of insurance.

What is insurable interest definition in life insurance?

An essential requirement for a life insurance contract is that the individual acquiring the policy should have a reasonable interest in the covered person. An individual cannot seek insurance for an unrelated person unless proper documents reveal the insurable concern.

How do you determine insurable interest?

It is customary for an insurance company to investigate before granting an insurance policy. The investigation unit professionals communicate with the applicant and beneficiary to confirm the legitimacy. They will study the putative insured’s relationship and determine whether it is valid or not. It will help the insurance company in identifying fraudulent applicants and claims.

Recommended Articles

This has been a guide to Insurable Interest and its Meaning. Here we discuss insurable interest principles and detailed explanations along with examples. You can learn more from the following articles –