What Is Deposit Insurance?

Deposit insurance is a type of insurance that protects depositors against loss in the event of a bank failure. It was first launched in the United States during the 1930s Great Depression to shield bank depositors from loss.

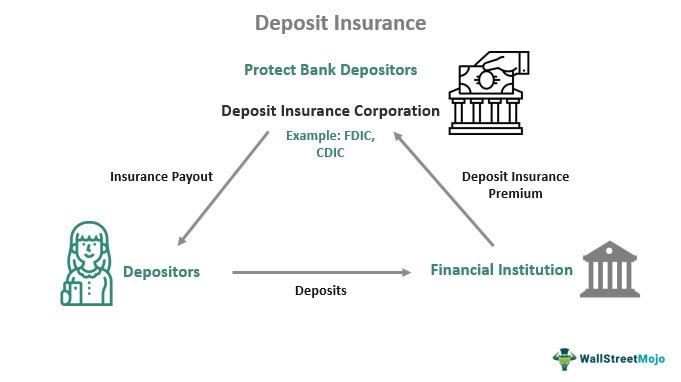

It is an element of the financial safety net since it offers protection against banking crises and funding to lessen their effects. The institutions that offer deposit insurance can be government-run, a part of a nation’s central bank, a private institution, or private institutions with government support.

- Deposit insurance is a type of insurance that protects depositors from loss if a bank fails. In addition, it promotes economic stability by lowering bank depositors’ likelihood of simultaneously withdrawing their funds.

- One example of an institution offering it is the FDIC in the United States. The standard insurance amount they provide is $250,000 per depositor, per FDIC-insured bank, and the ownership category.

- Offering guarantees and security to customer deposits also benefits the banks. If banks take on too many risky investments or overextend themselves and fail, they don’t necessarily go bankrupt. Instead, the FDIC takes control of them and puts them under new management.

How Does Deposit Insurance Work?

The deposit insurance program contributes to the overall well-being of the banking sector and the economy. As a result, depositors can feel confident even during periods of financial turbulence because of solid consumer safety. In addition, it promotes economic stability by lowering the possibility of a significant number of bank depositors withdrawing their funds at once. The member banks’ and institutions’ contributions are placed in a fund and used to fund the deposit insurance program.

Deposit insurance is based on the theory that people will refrain from trying to withdraw their money even if they learn that the bank is insolvent because they are confident that the government-backed entity will reimburse them in the event of a bank failure. It is done to stop bank runs on institutions reported as insolvent or having financial problems. Additionally, bankrupt banks won’t need to sell their assets rapidly to obtain money.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

Example

Let us look at a deposit insurance example to understand the concept better:

An example is the Federal Deposit Insurance Corporation (FDIC). It is an independent agency established by Congress to maintain financial stability and public trust in the United States. The Federal Deposit Insurance Corporation (FDIC) and the Deposit Insurance Fund (DIF) aim to offer deposit insurance to depositors in American depository institutions. However, the FDIC does not cover deposits made at credit unions. Instead, the National Credit Union Administration (NCUA) often provides insurance to credit unions.

A bank failure occurs when a financial institution cannot meet its obligations to its depositors and creditors. When an FDIC-member bank fails, the FDIC intervenes to protect bank deposits. The agency first tries to complete the failed bank’s acquisition by another financial institution. As a result, depositors’ funds are not lost, and their accounts are immediately transferred to the acquiring bank. In addition, depositors are paid directly if the FDIC cannot find a financial institution to acquire the bank.

The insurance amount will be at least $250,000 per depositor, per FDIC-insured bank, and per ownership category. Customers can utilize this coverage without taking any action. For example, if a person has deposited with an FDIC member bank, they are automatically protected. Consumers do not pay anything for this coverage; banks and other financial institutions pay.

FDIC deposit protection provisions cover deposit accounts at member banks. Accounts are held individually, jointly, and for specific specialist purposes. The following is a list of accounts that the FDIC insures: checking, savings, money market, certificate of deposits, prepaid accounts, IRAs, and other self-directed retirement accounts, trust accounts created at a bank that is both revocable and irrevocable, non-self-directed employee benefit plans held by banks, accounts for businesses, partnerships, and unincorporated associations, government-owned institutions’ depositories, etc.

Advantages And Disadvantages

Let’s look into the advantages and disadvantages of deposit insurance.

Some of the advantages are the following:

- The main benefit for individuals is the peace of mind associated with knowing that their deposits won’t become inaccessible if their bank goes bankrupt or is rendered insolvent. In addition, it indicates that individuals are more likely to deposit money into their bank accounts than other investments.

- It contributes to the economic stability of the nation.

- It helps to gain and retain the trust and confidence of people in the banking system.

- Banks can benefit from the protection element of this offering. If banks take on too many questionable investments or overstretch themselves and fail, they don’t always go extinct. Instead, the FDIC will take them up and put them under a new administration. As a result, the bank’s management loses control of it yet does not entirely fail as they could otherwise.

Some of the disadvantages are the following:

- Banks have always been subject to moral hazard because they make money from the deposits of others, money they borrowed, or investors’ money. As a result, banks are encouraged to take more significant risks when their depositors are covered.

- It weakens depositors’ incentives to keep an eye on the risk posed by management’s actions and to take corrective action, such as withdrawing deposits when the danger rises, reducing market discipline.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What is Deposit Insurance and Credit Guarantee Corporation?

The Deposit Insurance and Credit Guarantee Corporation (DICGC)is a wholly-owned subsidiary of the Reserve Bank of India. It provides deposit insurance as a safety net for bank depositors if the banks cannot make payments.

What is Canada Deposit Insurance Corporation?

In order to offer deposit protection to depositors in Canadian commercial banks and savings institutions, the Parliament of Canada established the Canada Deposit Insurance Corporation as a Federal Crown Corporation in 1967. In the event of a banking collapse, the CDIC guarantees Canadians savings of up to $100,000 held at Canadian banks.

What is not covered by deposit insurance?

Mutual funds, annuities, life insurance plans, stocks, and bonds are not considered deposits. Also, they are examples of investment goods. Hence they are not protected by FDIC deposit insurance.

Recommended Articles

This article has been guide to What is Deposit Insurance and its meaning. Here, we explain it with examples and its advantages and disadvantages. You may also find some useful articles here: