What Is Professional Liability Insurance?

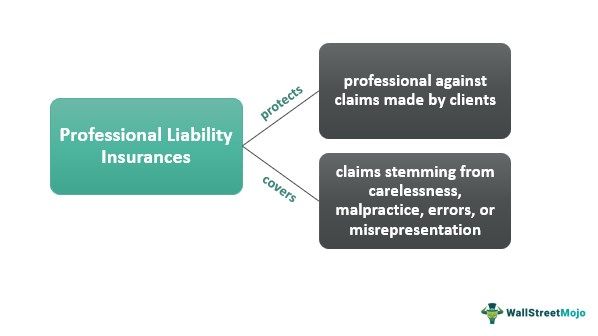

Professional liability insurance, often known as PLI, protects professionals like accountants, attorneys, and doctors against claims of negligence and other types of claims made by their patients or clients. Because general liability insurance plans do not give protection against claims stemming from carelessness, malpractice, errors, or misrepresentation, experts who specialize in a particular field are required to get this form of insurance.

It is also known as errors and omissions insurance by those in the real estate segment. Standard policies for professional liability will indemnify the insured against loss resulting from any claim or claims made during the policy period as a result of any covered error, omission, or negligent act committed in the conduct of the insured’s professional business during the policy period.

- Businesses can defend themselves against allegations of negligent behavior with the help of professional liability insurance.

- This insurance is utilized by experts such as accountants, builders, information technology specialists, physicians, and professionals who contract their services, among other professionals.

- PLI policies cost far less than legal representation, legal costs, and other associated expenditures; the average annual premium is between $500 and $1,000.

Professional Liability Insurance Explained

Professional liability insurance can go by various titles, such as medical malpractice insurance if it is purchased by members of the medical profession or mistakes and omissions insurance if members of the real estate industry purchase it. Insurance for professional liability is a specialized kind of protection that is not included in standard homeowner’s insurance, in-home corporate policies, or firm owner’s policies.

Most plans for professional liability insurance are claims-made, meaning that coverage is only valid for claims that are made and events that take place while the policy is still in effect. However, one may also find occurrence policies, meaning they are protected if an event happens, while they have insurance if the plan lapsed. A customer files a claim against the person after it expires.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

Cost And Coverage

The amount varies depending on the region, the industry, and the number of claims filed in the past. Other aspects that might play a role in determining the cost of insurance include the company’s staff and the years spent in the company.

Coverage limitations and deductibles, just as with other kinds of insurance coverage limitations and deductibles e, affect the policy’s overall cost. According to data compiled by the insurance company Insureon, the typical premium for professional liability insurance is between $500 and $1,000 annually, with most contracts having a monthly premium of $59.

Different kinds of coverage come with such insurance. Although only the types of legal responsibility specified in the policy are covered by insurance, this excludes criminal prosecution and all forms of legal liability under civil law. The following are some examples of liabilities that PLI covers: Inaccuracies, omissions, and mistakes in the services that were supplied, Undelivered services, several missed deadlines, carelessness or a failure to satisfy the requirements, and infringement of the contract.

Examples

Let us look at some examples of professional liability insurance to understand it better:

Example #1

With ever-changing rules in the financial services business, traders must proactively manage their risks. Therefore, traders who serve as brokers must register with the U.S. Securities and Exchange Commission (SEC), join a self-regulatory organization (SRO), and comply with federal securities laws and regulations. If one makes a mistake as a trader, professional liability insurance assists in paying for legal defense. Traders’ insurance can also assist in covering defense expenses. It can be in the case of accusations of carelessness, mistakes in judgment, or misuse of client funds.

Example #2

According to a Business Wire report, At-Bay is an insurance offering various professional liability insurance policies. Through an API channel that provides auto-quotes for companies with revenue of Up to $25 Million. Brokers can acquire bindable quotations when applying a policy with up to $2 million limits. That too in less than two minutes for more than 50 different business classes after the system has been deployed. Within two days, brokers hear from an underwriter regarding customers who require limits of up to five million dollars.

Professional Liability Insurance vs General Liability

- General liability and professional liability protection against distinct types of risk. Only general liability insurance can protect the company from claims if a customer slips and falls on commercial premises. Professional liability insurance can only protect the business against the high expense of claimed professional errors.

- General liability covers material damages, whereas professional liability covers monetary losses. Product liability insurance is sometimes included in general liability coverage for construction professionals, manufacturers, merchants, and other company owners. This coverage protects the insured from claims arising from finished work that causes physical injury to a third party. This may appear to be the area of professional responsibility, but the dividing line is physical injury. Professional liability insurance addresses disputes involving monetary losses caused by a person’s products or services.

Professional Liability Insurance vs Malpractice Insurance

- Malpractice is a type of professional liability. It covers just physical harm as opposed to financial or legal damages.

- A variety of vocations, such as attorneys and engineers, are covered by liability insurance for potential losses. However, malpractice insurance is especially geared to the risks faced by medical professionals. For example, during a difficult surgical process, a surgeon runs a far higher chance of causing injury than an architect.

- However, professional liability insurance is not the same thing as malpractice insurance in and of itself. Malpractice insurance is a subset of professional liability insurance. Malpractice insurance is the name physicians and lawyers give to the professional liability coverage that is particular to their business.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What does professional liability insurance cover?

Any negligence, omissions, or errors made by a professional while providing a service that leads to harm to the property of a third party or damage to the third party themselves can be covered by a professional liability insurance policy, which protects the policyholder from any legal liabilities that may result.

How much does professional liability insurance cost?

Costs depend on the region in which one practice, field, and the number of claims filed against someone. The company’s number of workers and the length of time in the company may also affect the cost of insurance coverage. Similar to other forms of insurance, coverage limitations and deductibles affect the total cost. According to information from insurance company Bizinsure, the average cost of professional liability insurance for most small business owners is $600 or less annually.

Who needs professional liability insurance?

Professionals and service-providing firms such as Consultants, Engineers, Brokers of real estate agencies, and Client-serving accountants should obtain professional liability coverage. This insurance protects a business from claims of professional errors, faults, or failed service delivery.

Recommended Articles

This has been a guide to what is Professional Liability Insurance. Here, we explain its cost, coverage, and comparison with general liability. You can learn more about it from the following articles –