What Is Decreasing Term Life Insurance?

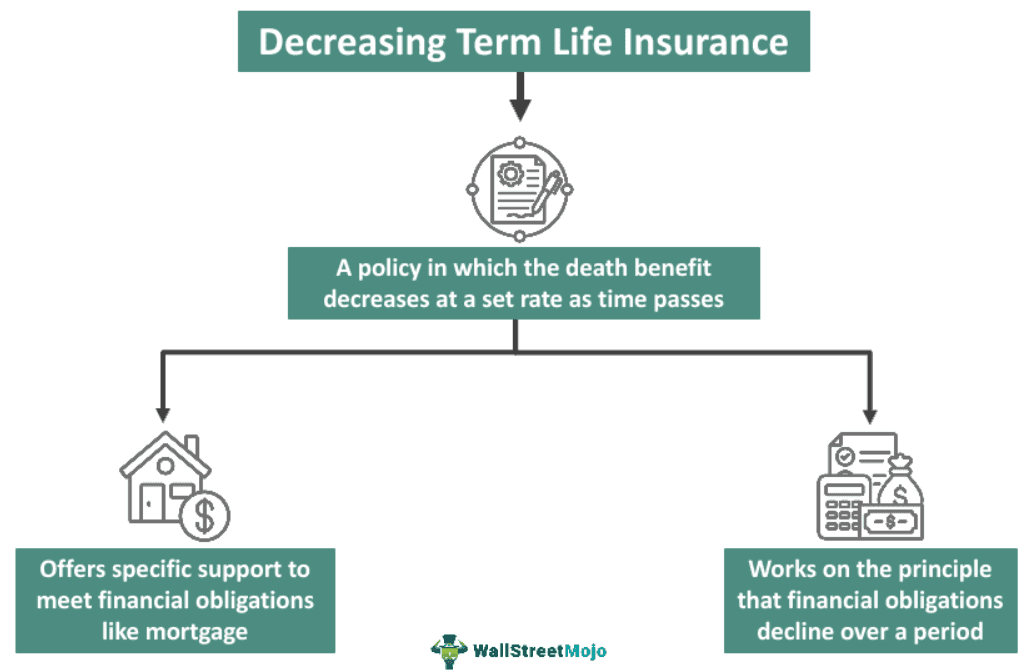

Decreasing term life insurance is a type of life insurance policy where the death benefit decreases over time. Death benefit is the amount paid to the beneficiaries in the event of the death of a policyholder. It is commonly used to ensure that the remaining balance of an amortizing loan, like a mortgage or a business loan, is covered over time.

The premiums are typically constant throughout the contract, while the reduction in the coverage amount occurs monthly or annually. The term length varies, usually ranging from 5 to 30 years, depending on the insurance company and the specific plan a policyholder chooses.

- Decreasing term life insurance is a type of life insurance policy where the coverage amount decreases over the policy’s term.

- This type of policy is cost-effective and serves the purpose of protecting specific debts, making it an attractive option for those who want to ensure their loved ones can handle the relevant financial burdens if they pass away during the policy term.

- Decreasing term life insurance is designed for specific financial obligations expected to decrease or decline over a period, while level term life insurance provides a consistent payout that generally meets a broader range of financial needs.

How Does Decreasing Term Life Insurance Work?

A decreasing term life insurance policy is a specific type of term life insurance designed to provide financial protection to individuals with decreasing financial obligations over time. When someone purchases this policy, they select a term length, typically ranging from 5 to 30 years, and an initial death benefit amount. The term represents the duration during which the policy will remain in effect.

During the term of the policy, the key feature is that the death benefit gradually decreases over time. This progressive decrease, at a predetermined percentage, is systematic. It can occur either monthly or annually, depending on the terms of the policy. The purpose of the decreasing death benefit is to align with a policyholder’s changing financial responsibilities.

If a policyholder were to pass away during the policy’s term, their beneficiaries would be eligible for the death benefit. However, the amount the beneficiaries receive is based on the current reduced value of the death benefit at the time of a policyholder’s death. This payout is intended to help a policyholder’s loved ones cover any outstanding financial obligations, such as a mortgage, loans, or other debts that typically decrease as they are paid off over time.

Conversely, if a policyholder outlives the policy’s term, the death benefit gradually decreases to zero, and the coverage comes to an end. At this point, the policyholder and their beneficiaries no longer have the financial protection provided by the policy.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

Examples

Let us look at some examples to understand the decreasing term life insurance definition better.

Example #1

Assume John, a 30-year-old married individual with two children, wants to ensure his family is financially protected in case of his untimely death. He decides to purchase a decreasing term life insurance policy with a coverage amount of $500,000 for a term of 20 years.

Year 1:

- John’s policy provides a death benefit of $500,000.

- He pays monthly premiums to maintain the coverage.

- Over the years, the outstanding mortgage on his family home gradually decreases.

Year 10:

- The outstanding mortgage on John’s home has decreased significantly.

- John’s coverage has also decreased to match the remaining mortgage balance, which is now $200,000.

- The death benefit for Year 10 is $200,000.

Year 20 (End of Policy Term):

- John’s mortgage is fully paid off, and he no longer has any outstanding debts related to his home.

- His coverage has decreased to $0, as there is no mortgage to protect anymore.

- The policy term ends.

In this hypothetical example, decreasing term life insurance was a cost-effective way for John to ensure his family had sufficient coverage to pay off the mortgage if he passed away during the period when there was still a significant financial obligation. As the mortgage decreased over time, so did the coverage, aligning with the family’s decreasing financial needs.

Example #2

Suppose Stella, a 40-year-old breadwinner with a 20-year mortgage on her home worth $300,000, opts for a policy with a coverage amount that matches her mortgage balance. Over the years, as Stella continues to make mortgage payments, her decreasing term life insurance coverage gradually declines in line with the decreasing mortgage balance. It means if she were to pass away during this period, the policy would provide enough funds to pay off the mortgage and relieve her family of this financial burden, ultimately offering them peace of mind.

Advantages And Disadvantages

The section below discusses the advantages of life insurance in this form.

- Cost-Effective: Decreasing term life insurance typically requires policyholders to pay lower premiums compared to traditional term life insurance policies. This makes it more affordable, especially attracting individuals on a budget.

- Matches Financial Obligations: It is designed to align with specific financial obligations, such as a mortgage or loans. As a policyholder’s financial responsibilities decrease over time, so does the coverage amount, ensuring they pay for only what they need during a given period.

- Simplicity: The concept is straightforward. A policyholder knows exactly what the policy is meant for, and it serves the defined purpose efficiently. Policyholders need not worry about investment components or cash value.

- Mortgage Protection: It is an excellent choice for homeowners as it can be tailored to pay off a mortgage, ensuring a policyholder’s family can keep the family home if the policyholder passes away during the policy term.

This section discusses the disadvantages of this type of life insurance.

- Decreasing Coverage: While it is beneficial for specific needs like mortgage protection, it may not cover other expenses or provide a financial safety net for a policyholder’s family beyond the designated purpose.

- No Cash Value: While some permanent life insurance policies offer cash value after a period, this term life insurance does not generate cash value. Policyholders will not receive payouts if they outlive the policy term.

- Limited Flexibility: Once the coverage amount and term are chosen, there is limited flexibility for adjusting the policy. If a policyholder’s financial circumstances change, they may need to purchase additional coverage. New or additional coverage usually proves more expensive due to advancing age and other health conditions (as applicable).

- Shortcomings for Long-Term Needs: If a policyholder has long-term financial dependents or anticipates other financial responsibilities beyond the policy term, decreasing term life insurance may not provide adequate coverage for those needs.

Decreasing Term Life Insurance vs Level Term Life Insurance

The differences between decreasing and level term life insurance are listed in the table below:

| Basis | Decreasing Term Life Insurance | Level Term Life Insurance |

|---|---|---|

| Purpose | It is designed for specific, short-to-medium-term financial obligations. It is ideal for situations where policyholders want to ascertain debt repayment (e.g., mortgage or loan) in the event of their death before the policy expires. | Level term life insurance offers broader financial protection than decreasing plans. It is suitable for individuals who want to provide their beneficiaries with a consistent, larger payout that can cover various needs, such as income replacement, educational expenses, and debts. |

| Premium | Decreasing term insurance premiums are typically lower than level term insurance premiums, primarily because the coverage amount decreases over time. | Premiums for level term insurance are higher than decreasing term insurance because the coverage amount remains the same, and these policies offer a more substantial payout later. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1.Who sells decreasing term life insurance?

A wide range of insurance companies, independent agents, online marketplaces, and occasionally, financial institutions sell such life insurance. Some employers offer this insurance as part of group benefits. It is important to research well before selecting a policy. Comparing quotes from various service providers to find a policy that suits individual financial needs and budget is recommended.

2.What are the benefits of decreasing term life insurance?

The benefits of decreasing term life insurance include cost-effectiveness, as premiums are lower compared to level term policies. It is tailored to cover specific, diminishing financial obligations like mortgages.

3.Should I get a level term or decreasing life insurance?

The choice between level term and decreasing term life insurance depends on an individual’s financial goals and circumstances. If they want consistent, broader financial protection that remains the same throughout the policy term and covers needs like income replacement, education expenses, and debts, level term life insurance might be more suitable. If an individual has specific, diminishing financial obligations, such as a mortgage, which they want to ensure is paid off if they pass away, decreasing term life insurance is a cost-effective choice.

4.Can I cancel the decreasing term life insurance?

Yes, you can cancel this policy. Most insurance policies, including decreasing term life insurance, come with a “free look” period, in the first 10 to 30 days of purchase. During this period, you can cancel the policy and receive a full refund of the premiums paid. Beyond this period, you can still cancel the policy, but the process and potential financial implications vary depending on the insurance company and the policy terms.

Recommended Articles

This has been a guide to what is Decreasing Term Life Insurance. Here, we explain it with examples, comparison with level term life insurance, and advantages. You can learn more about it from the following articles –