Table of Contents

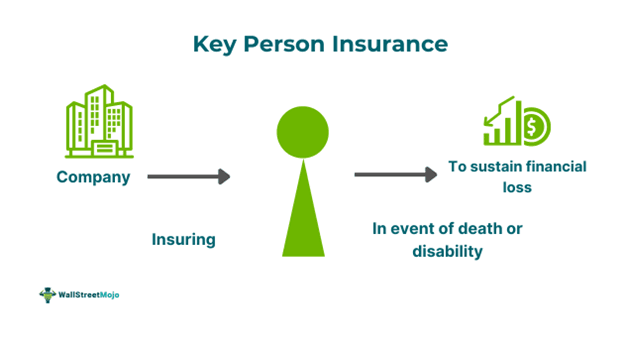

What Is Key Person Insurance?

A key person insurance policy is an arrangement where a company pays for insurance to protect the business from the loss of key individuals. These key persons could be valuable employees, partners, or directors who possess skills and experience critical to the business's success.

The insurance, in essence, pays the business rather than individuals. This helps mitigate and navigate the financial and operational risks that may arise from the sudden loss of a key person. The amount insured can be used for capital or revenue purposes that help the business continue despite its absence.

Key Takeaways

- Key person insurance policies are life insurance policies designated to benefit the business. They are, however, taken in the name of the key persons.

- Key persons are highly skilled, experienced individuals who, on death or disability, are a loss to the business.

- They could be owners, shareholders, or even employees.

- Cost and coverage depend on the age, health, and gender of the key person.

- The purpose of key person insurance is to save the business from financial loss and help them sustain in the period of loss.

How Does Key Person Insurance Work?

A key person insurance policy is a type of insurance arrangement where the policy pays the business rather than the insured or the beneficiaries. These policies are reserved for persons whose absence will be the company's financial burden. They can serve as both life and disability insurance. These key persons possess skills, knowledge, experience, and expertise that are difficult and costly to replace.

Key persons include founders, important executives, and owners who are critical to business survival. Under this arrangement, the business is the beneficiary, and it pays the premiums. In other words, in the event of death, disability, or other reasons, the business benefits the insurance payoff.

The purpose of the key person insurance amount may include paying off debts, supplementing lost revenues, or offsetting operating expenses. It may also be used to hire a replacement, distribute profit, shut the business, or pay severance benefits to employees.

The insurance provides death benefits to the insured businesses as a means to continue operation if the key person dies. They are free to decide the manner in which the death benefit is spent. The benefits of the insurance can also be leveraged when the insured is alive. These policies could be of two types: permanent life insurance policy and term life insurance policy. The term life insurance is for a particular term and extends to 10-30 years. Permanent life insurance does not end as long as the premiums are being paid.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

Cost And Coverage

Cost

The cost of business key person insurance is based on certain factors, including:

- Age of the insured

- Gender of the insured

- The overall health of the insured

- The type of policy

- Riders added, if any.

Coverage

Typically, a good coverage suggested would be 10 times worth the key person's salary. Furthermore, the evaluation of the monetary value they bring shall also be taken into consideration. This can be estimated using the following:

- The contribution made by the person to the company's profits. This shall include the income lost and the impact of fulfilling business objectives.

- The replacement cost required for the key person after taking into consideration their skills and compensation. In addition, the lost sales and replacement or recruitment costs shall also be taken into account.

Furthermore, knowing a company's total key employees and understanding its legacy and contingency plans can help

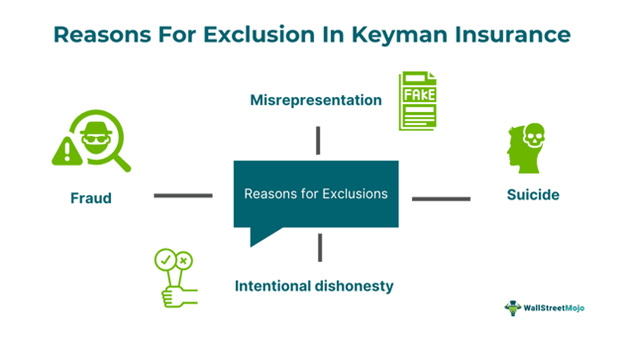

Exclusions

Given below are some of the common key person insurance or key man insurance policies.

- Misrepresentation

- Suicide of a key person

- Fraud

- Intentional dishonesty

It should be noted that the first two years of policy often come with contractual clauses. This is known as the contestability period. Any claims within the period will be investigated, whether due to fraud or deliberate omissions. Suicide of such persons will also not be considered during the period.

Tax Treatment

Businesses pay the policy premiums, which cannot be counted as business expenses and are, therefore, not tax deductible. The life insurance death benefit, however, is given tax-free to the beneficiary.

Suppose the business owners own the insurance policy instead of the business; then, a deduction can be made. The premiums can be deducted as compensation to the actual owner. In permanent life insurance, the cash value growth is tax deferred. The business may borrow against cash value, and this will not create a taxable event.

Examples

Let us look into some examples to understand the concept better:

Example #1

Suppose ABC Ltd., a cloth manufacturing company, recently lost its marketing manager due to health issues. The manager had served the company for over a decade and had excellent knowledge of facing market ups and downs, making him a key personnel. His sudden demise disrupted the product marketing area. Unfortunately, recruiting a new manager would take a few months to finalize. Fortunately, the company had key person insurance. This insurance helped them sustain the business, hire a new person, and train them. The insurance amount comes as a relief for sustaining a business loss.

Example #2

An article published on January 20, 2023, discusses how businesses like Tesla, JPMorgan, and Meta are at risk from relying too much on one person. To reduce these risks, it highlights the necessity of key person insurance and efficient succession planning. The article suggests boards implement succession planning, insurance, and leadership diversification techniques to safeguard operations from the negative consequences of losing a key individual.

Benefits

Given below are some of the benefits of this insurance:

- The sum assured helps the company in coping with the loss of letting go of a key employee.

- It helps the company in continuing the business.

- Such insurance gives them breathing space to think about what to do next.

- This insurance contributes to risk management.

- It is especially useful for small businesses that have very few people working.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.